Answered step by step

Verified Expert Solution

Question

1 Approved Answer

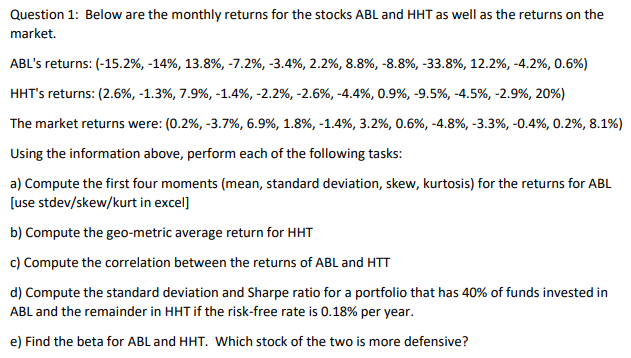

Question 1: Below are the monthly returns for the stocks ABL and HHT as well as the returns on the market. ABL's returns: (-15.2%, -14%,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Legal Environment Today Summarized Case Edition

Authors: Roger LeRoy Miller

8th Edition

130526276X, 978-1305279407, 1305279409, 978-1305704930, 1305704932, 978-1305262768