Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Question 1 Easing Pte Ltd (EPL) is a company based in Singapore that specialises in providing consulting services. EPL adopts the Singapore Financial Reporting Standards

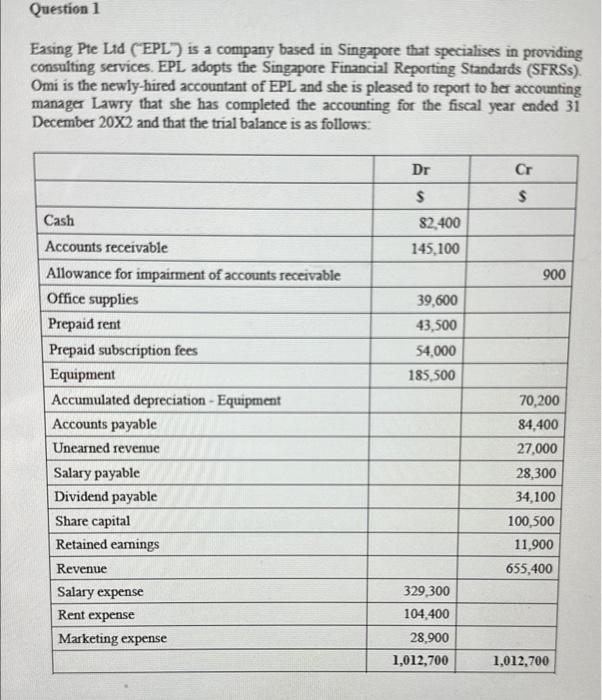

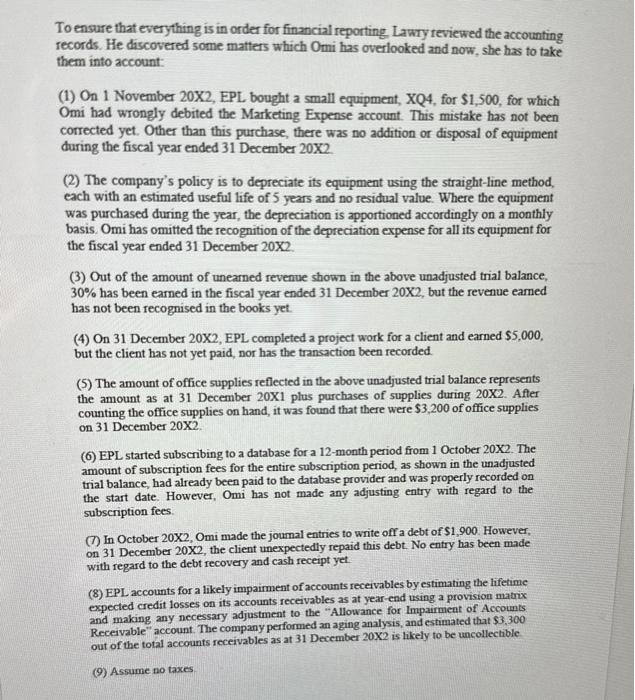

Question 1 Easing Pte Ltd (EPL) is a company based in Singapore that specialises in providing consulting services. EPL adopts the Singapore Financial Reporting Standards (SFRSs). Omi is the newly-hired accountant of EPL and she is pleased to report to her accounting manager Lawry that she has completed the accounting for the fiscal year ended 31 December 20X2 and that the trial balance is as follows: Cash Accounts receivable Allowance for impairment of accounts receivable Office supplies Prepaid rent Prepaid subscription fees Equipment Accumulated depreciation - Equipment Accounts payable Unearned revenue Salary payable Dividend payable Share capital Retained earnings Revenue Salary expense Rent expense Marketing expense Dr $ $2,400 145,100 39,600 43,500 54,000 185,500 329,300 104,400 28,900 1,012,700 Cr $ 900 70,200 84,400 27,000 28,300 34,100 100,500 11,900 655,400 1,012,700

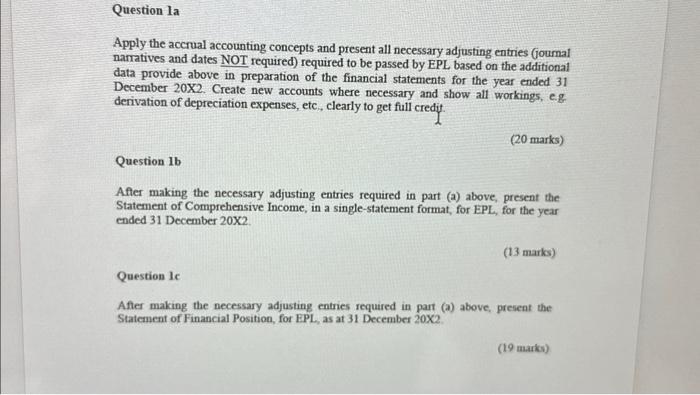

please answer the full question

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Fraud Examination

Authors: Joseph T. Wells

4th edition

1118922344, 9781118803264, 1118582888, 9781118922347, 1118803264, 978-1118582886