Question

Question 1. Explain the terms in your own word Poor Quality Of Reported Earning i. Accounting for Acquisition ii. High Capital Expenditure iii. Revenue Recognition

Question

1. Explain the terms in your own word

Poor Quality Of Reported Earning

i. Accounting for Acquisition ii. High Capital Expenditure iii. Revenue Recognition Issues iv. Weak Financial Control v. Expired Inventory

2. Write the Crux of the above article Note : ( Take time No issue But Answer is related to the article)

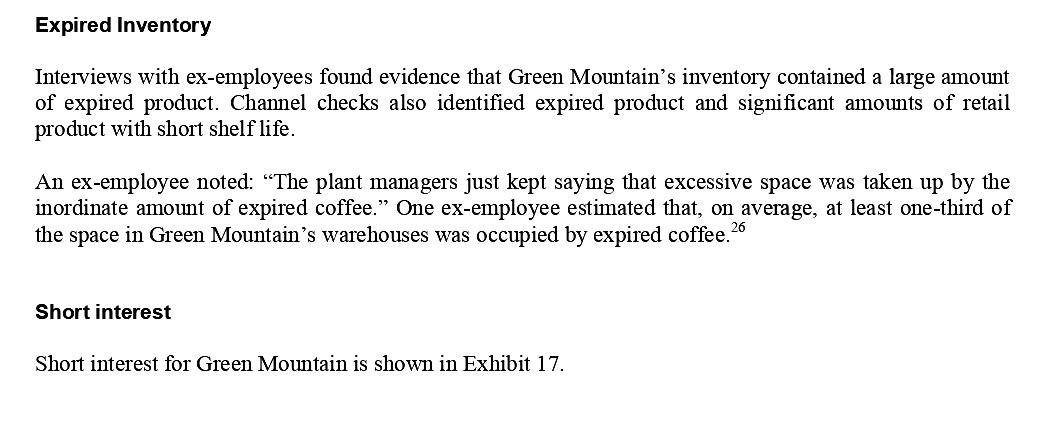

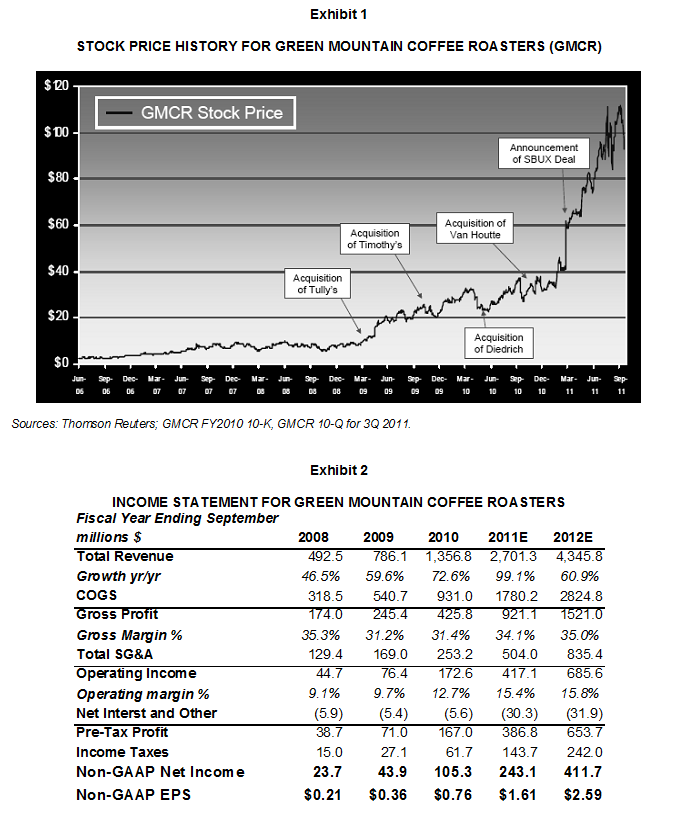

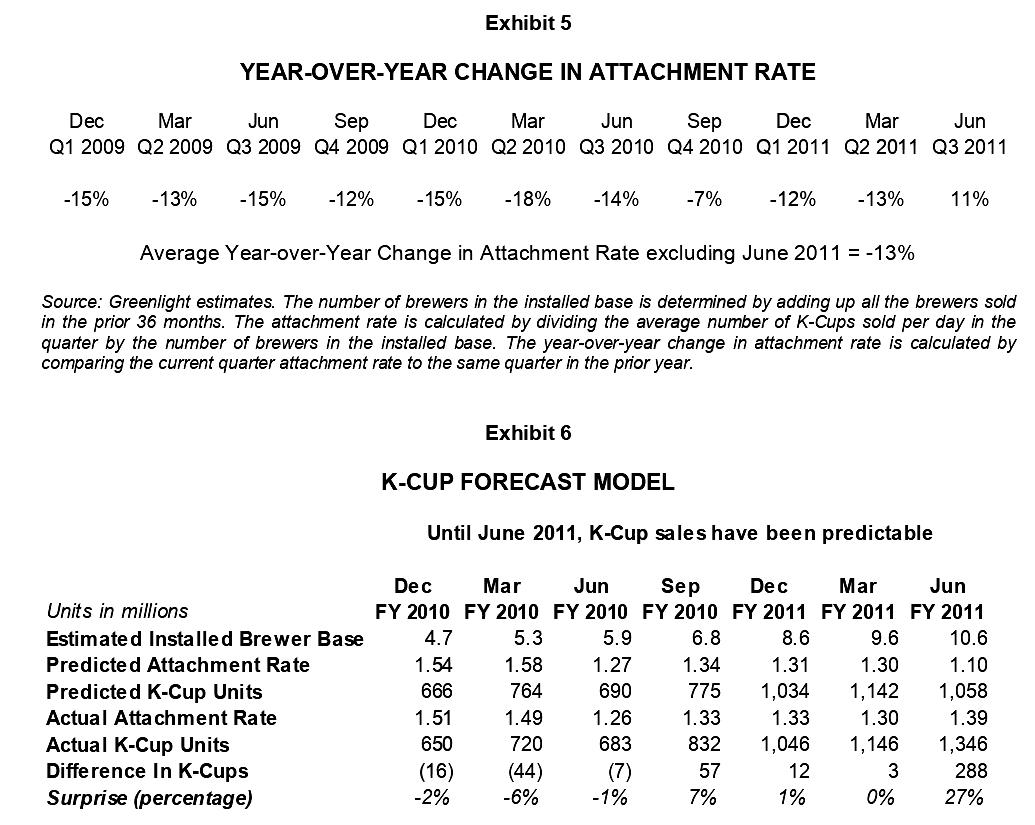

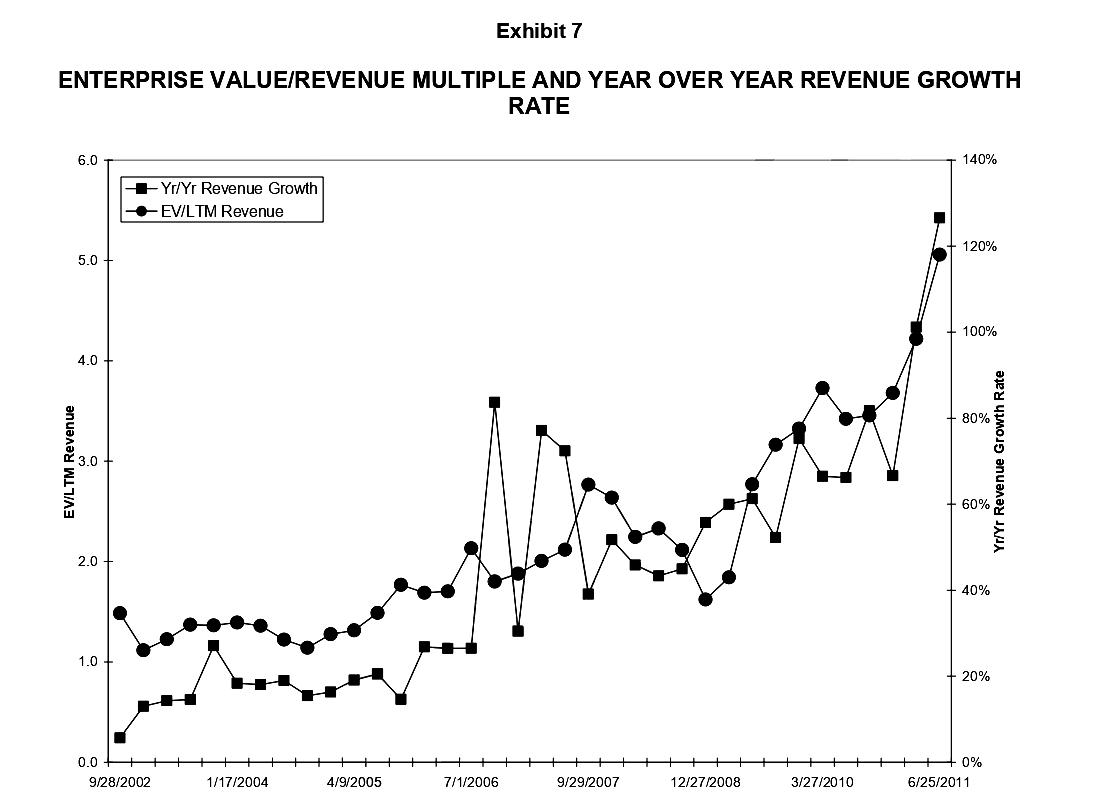

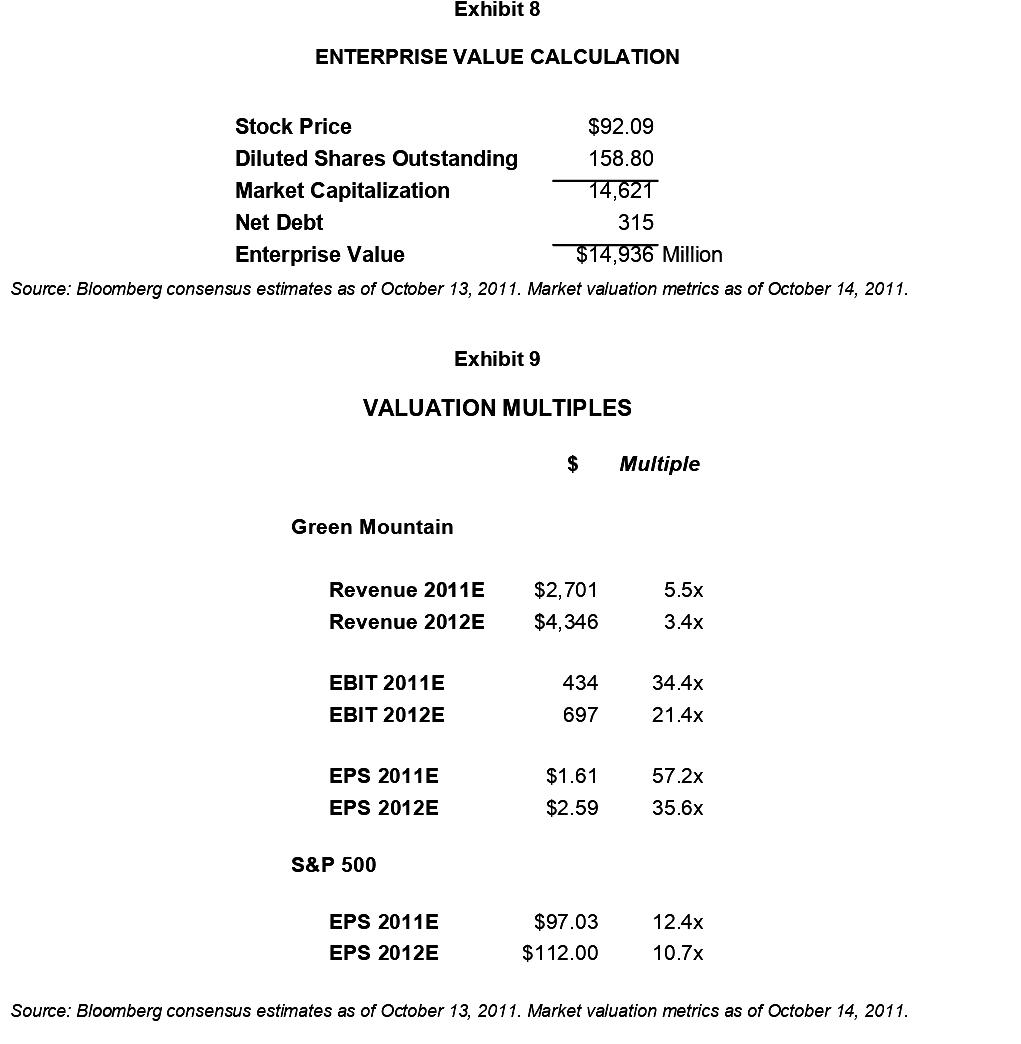

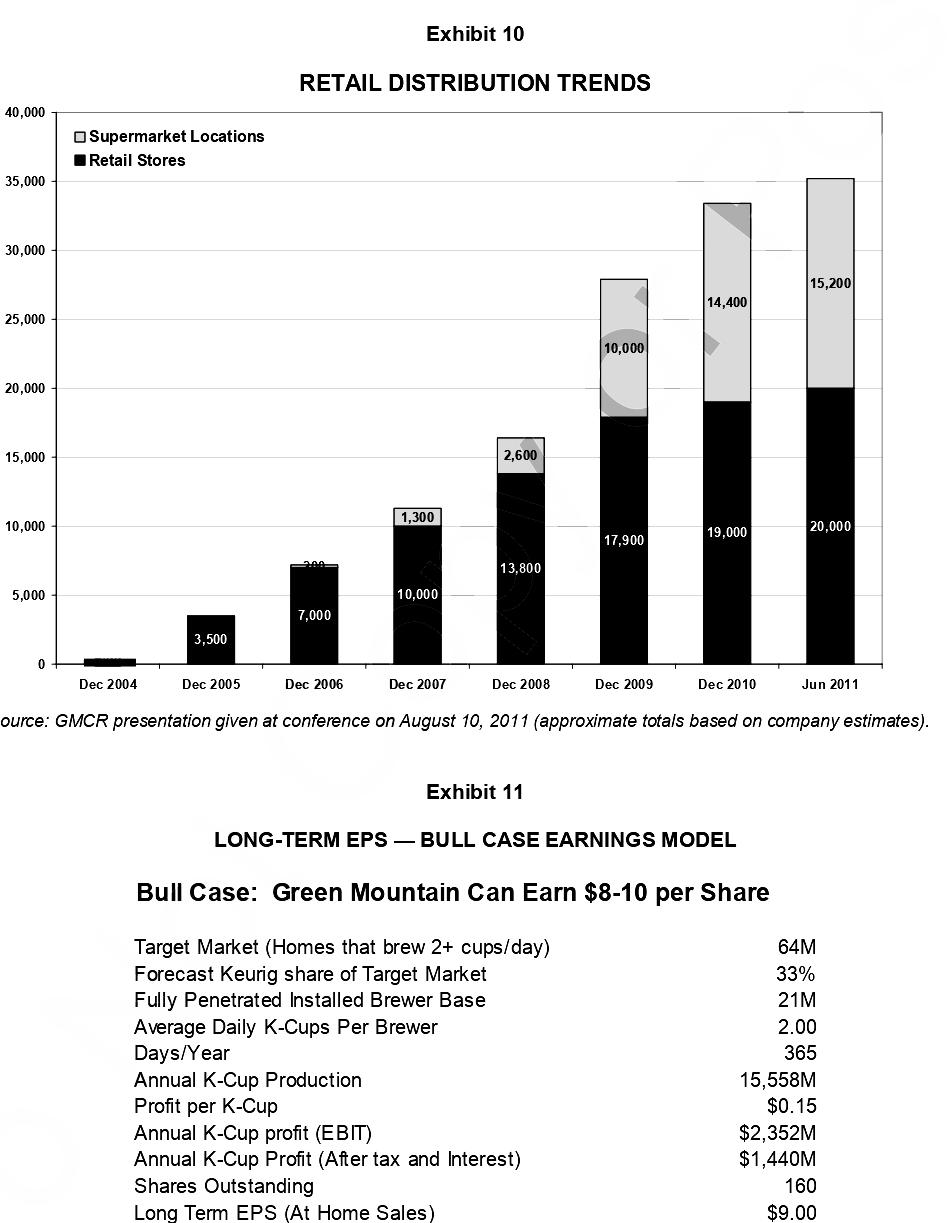

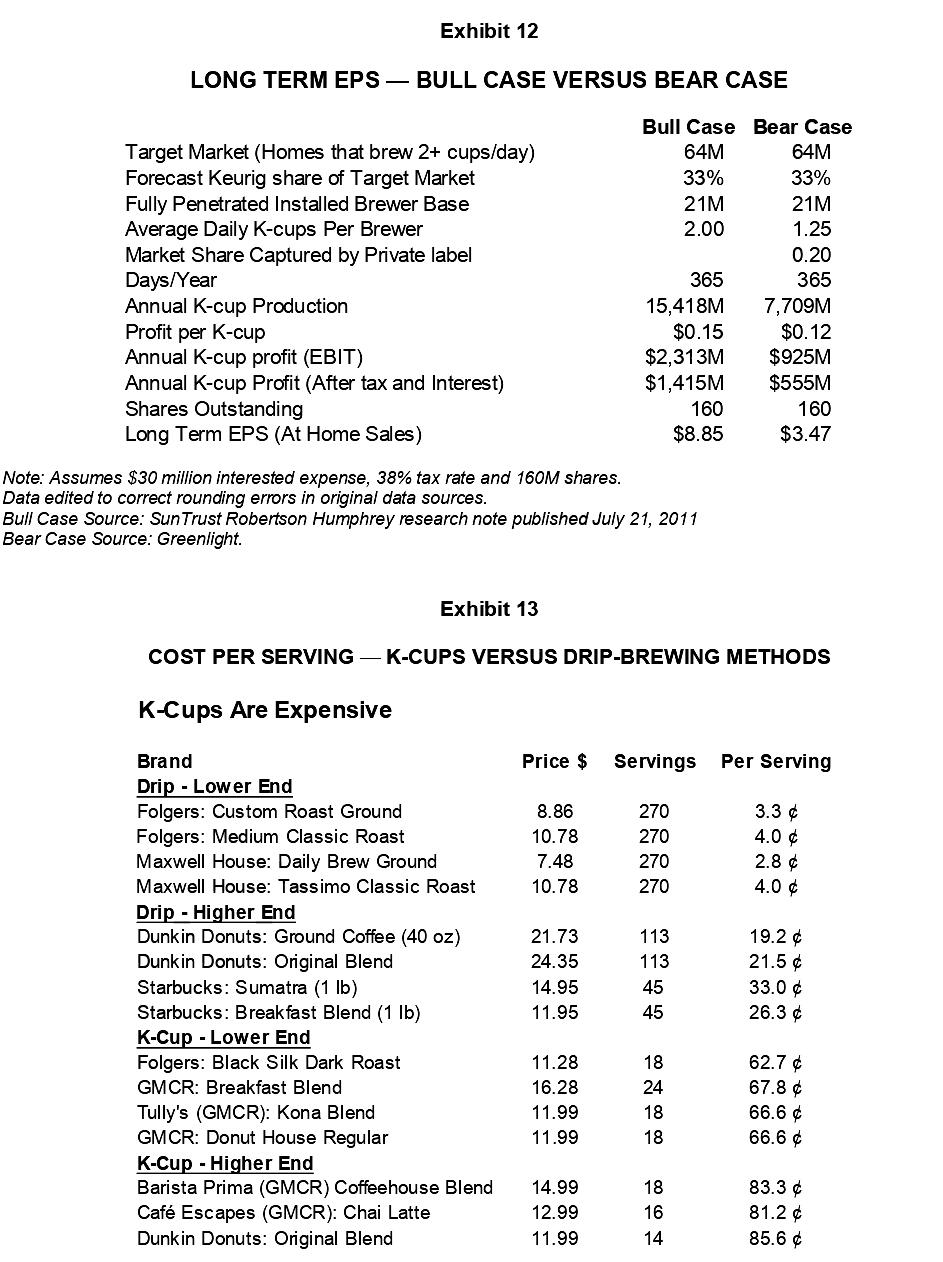

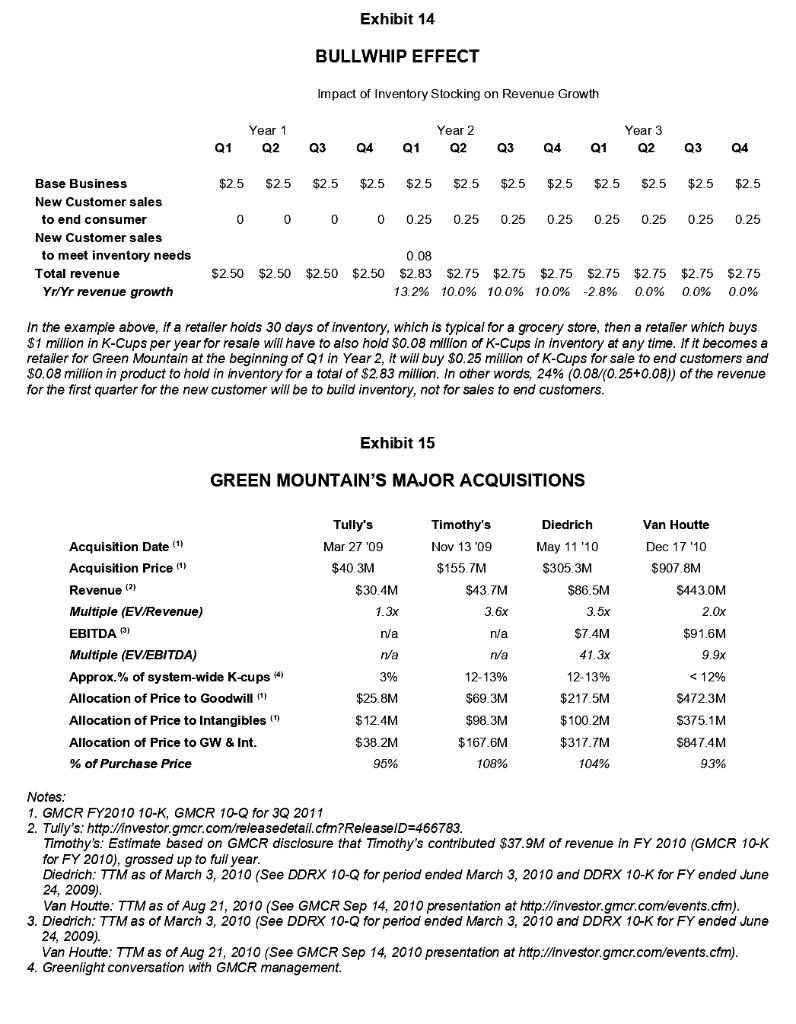

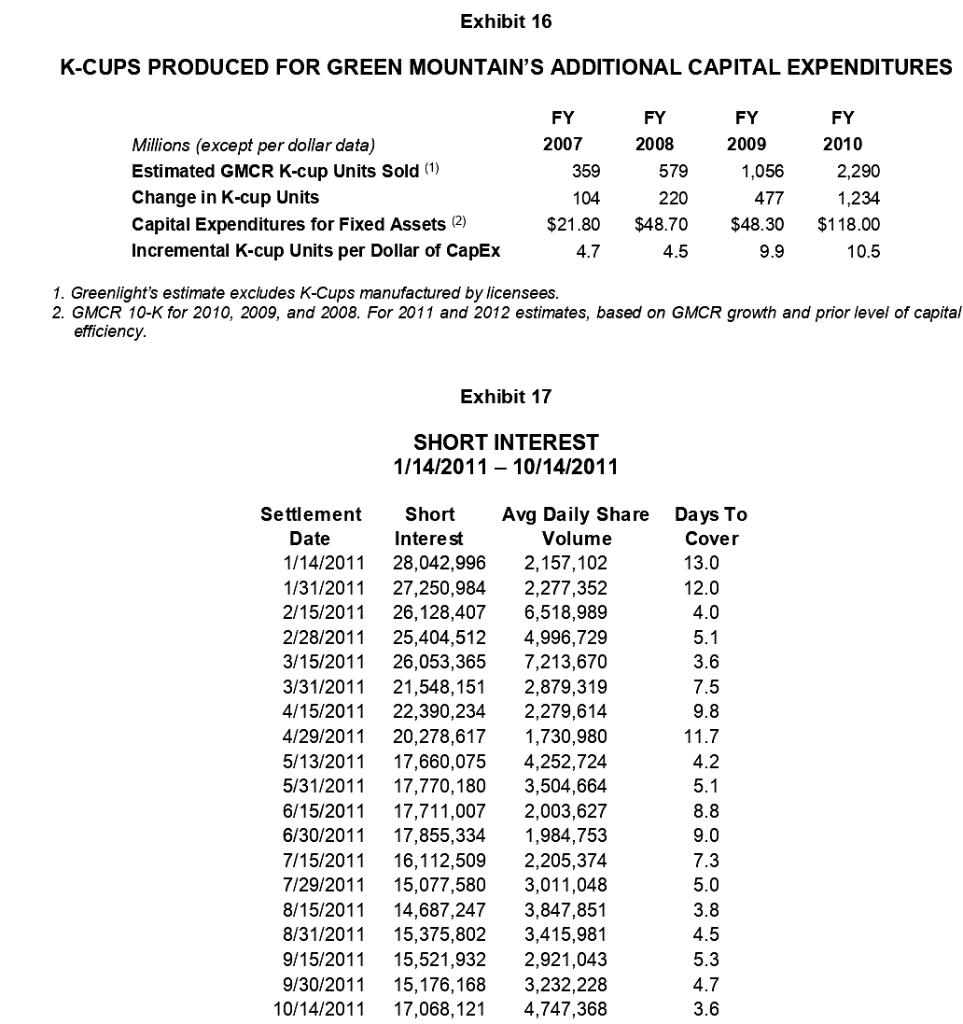

SELLING SHORT: GREEN MOUNTAIN COFFEE ROASTERS It was a cool day on October 18, 2011, as institutional investor Marty Dirks looked out his office window at the Bay Bridge that led from San Francisco to Oakland. He wondered, Do I feel lucky?" The day before Greenlight Capital (Greenlight), a highly-regarded long/short equity hedge fund had presented a bear case (the analysis supporting a short position) for Green Mountain Coffee Roasters (NASDAQ: GMCR) at the Value Investing Congress in New York. It was an intriguing investment idea, but held huge risk. Green Mountain Coffee Roasters (Green Mountain) was a volatile stock; in the past year its price had ranged from a 52-week low on December 16, 2010 of $31.21 per share to a 52-week high on September 20, 2011 of $115.98 per share (see Exhibit 1). If Dirks had sold Green Mountain's shares short on December 16, by September 20 he would have had a loss of 270 per cent in the position in a market in which the Standard & Poor 500 had declined 2 per cent over the same period of time. Could Dirks ever obtain enough conviction from his analysis to take on the investment risk inherent in Green Mountain? COMPANY HISTORY Green Mountain Coffee Roasters was founded in 1981 in rural Vermont, where it was still headquartered. Initially, it roasted and distributed coffee to restaurants and supermarkets throughout the region. For most of Green Mountain's history, sales of wholesale coffee represented the majority of the business. In 1998, Green Mountain started selling single-serve coffee in K-Cups for Keurig Brewing System machines, primarily for the office market. In 2002, Keurig introduced K-Cup brewing machines designed for the home market. At that time, Green Mountain invested $15 million in exchange for a 42 per cent ownership interest in Keurig. Four years later, Green Mountain bought the remaining ownership interest in Keurig for $104 million. This acquisition made single-serve coffee sales the majority of Green Mountain's business. With full ownership of Keurig, Green Mountain had evolved its business model to selling the K-Cup brewing machine for at (or near) cost and locking in a long-term sales annuity of single-use consumables at attractive profit margins. Green Mountain grew Keurig through direct sales and by licensing the K-Cup manufacturing technology to other coffee retailers such as Tully's, Timothy's, Diedrich and Van Houtte. Green Mountain also struck agreements to manufacture K-Cups for well-known coffee companies, such as Starbucks Corporation and Dunkin' Donuts, providing the K-Cup with an even stronger market presence. Patents Green Mountain's K-Cup design was patented; however, the patents were due to expire in September 2012. Accordingly, Green Mountain had stated it would roll out a new brewing technology to provide new patent protection in the future. Green Mountain's fiscal year 2009 Form 10-K filing stated: The two principal patents associated with our current generation K-Cup portion packs will expire in 2012, and we have pending patent applications associated with this technology which, if ultimately issued as patents, would have expiration dates extending to 2023. Furthermore, during a conference call with investors in July 2011,4 Green Mountain's chief executive officer (CEO) explained: With respect to our patents and intellectual property, we have a broad portfolio of patents on portion packs, on brewing machines and on the system of both portion packs and brewing machines, and certainly to the extent that any other product might infringe on our intellectual property, we take that very seriously and we would, in fact, rigorously defend our intellectual property . Financials From 1991 to 2000, revenues grew at a 25 per cent compound annual growth rate (see Exhibit 2). From 2000 to 2005, revenue growth slowed to 14 per cent per year. From 2006 to 2010, revenues grew 57 per cent per year (see Exhibit 3). Approximately 96 per cent of Keurig brewing machines shipped in fiscal year 2010 were sold to a television-based shopping outlet, the At Home channel. In total, Green Mountain had sold over 13 million single-serve brewing machines and over 9 billion K-Cups. According to the Wall Street consensus assumptions, Green Mountain's return on invested capital was approximately 16 per cent (see Exhibit 4). Consumable Attachment Rate Analysts following Green Mountain developed a methodology for tracking and forecasting sales of K- Cups. They calculated a metric referred to as the attachment rate the average number of K-Cups sold per day for the quarter, divided by the number of brewing machines in the installed base. Analysts assumed the installed base consisted of all brewing machines sold in the prior 36 months. Until the June 2011 quarter, the attachment rate had declined an average of 13 per cent from the same quarter in the prior year (see Exhibit 5). Using the assumption that the attachment rate was therefore declining at a rate of 13 per cent from the same quarter in the prior year, a reasonably predictive model was developed to forecast the next quarter's attachment rate (see Exhibit 6). However, in the June quarter the attachment rate was unusually high. Management did not offer any clear explanations for this increase, attributing the surprisingly strong June quarter sales to the cumulative effects of multiple factors. Valuation Metrics As revenue growth increased, valuation multiples had increased substantially over the past five years (see Exhibit 7). Enterprise Value was $14.9 billion (see Exhibit 8). Based on Green Mountain's current stock prices, up-to-date Wall Street estimates were calculated for Green Mountain's revenues, earnings before interest and taxes (EBIT) and eamings per share (EPS); retail distribution trends were similarly assessed (see Exhibits 9 and 10). THE BULL CASE Bullish investors viewed Green Mountain as a high-growth business in its early stages. In an investor conference presentation on August 10, 2011, Green Mountain pointed to the 90 million households that owned a coffee-brewing machine as the company's potential market and, with an installed base of 7 to 9 million brewing machines, noted that Green Mountain had only penetrated eight to 10 per cent of the market. Most analysts were more conservative and focused on the 64 million households that drank more than two cups of coffee each day. The bullish investors believed Green Mountain could capture one-third of that market, attaining an installed base of 21 million brewing machines. As of May 2011, Green Mountain's installed base was 7.5 million machines, suggesting that the installed base could triple from that level. Bullish investors cited a number of arguments to support their ownership decision. Firstly, Green Mountain was capacity-constrained and had been unable to meet demand. On the first-quarter 2011 earnings call held on February 2, 2011, Larry Blanford, Green Mountain's CEO, stated: We are definitely being stretched . . . demand is definitely stretching our ability to supply. And we have not quite caught up with that demand curve yet.9 The company had stated that its sales were constrained by inadequate production capacity; therefore, as additional capacity was added, sales should grow quickly and Green Mountain's profit margins would expand as additional infrastructure investments were made in 2012. Similarly, distribution was likely to expand substantially from its current level. Retailers would commit additional shelf space to brewing machines and K-Cups going forward. Additional sales would also result from adding recognized brands like Starbucks and Dunkin' Donuts to the Keurig system. Availability of these brands in the Keurig system would reduce the risk of competition. Growth of the Keurig installed base should continue as well. The K-Cup had become the standard format for single-seive coffee and the only prominent coffee brands that Green Mountain did not have in its portfolio were Maxwell House and Peet's. Furthermore, while coffee made with K-Cups was more expensive than coffee made with traditional brewing methods, it was still far less expensive than coffee purchased at certain retailers, such as Starbucks: the cost of coffee brewed from K-Cups was approximately one-third of the cost of coffee purchased at Starbucks. The K-Cup brewing system was a premium-priced, high-end system. Private- label coffee sales represented approximately 10 per cent of all coffee sold at retail and, since private-label coffee was a low-end, unbranded product, it was expected to penetrate only a small part of the K-Cup market. 11 Finally, Green Mountain was well protected against competition. In March 2011, Green Mountain's chief financial officer (CFO) stated: We are a technology company with a host of patents."12 In August 2011, Green Mountain's CEO said, I would define our company today as really a single-serve beverage company that is sitting on top of this magnificent technology call it disruptive technology platform."13 Management had further described Green Mountain's position in the marketplace as "the iPod of coffee."14 Even after Green Mountain's patents expired in 2012, there would be substantial barriers to entry by competitors. The capital investment required to produce K-Cups on a large scale was significant and new entrants would likely have a difficult time obtaining retail shelf space. Some prominent investors had great faith in Green Mountain's business model. In June 2011, referring to Green Mountain's many relationships with branded coffee manufacturers, prominent investor, Jim Cramer, described Green Mountain as an exchange-traded fund (ETF) on the rapid-growing single-serve market. "15 An optimistic estimate for long-term earnings per share (EPS) potential was calculated to be $8.00 to $10.00 per share (see Exhibit 11). THE BEAR CASE Greenlight's estimate for Green Mountain's long-term earnings power differed substantially from the bull case. Greenlight estimated long-term EPS potential at $3.47 per share (see Exhibit 12), in contrast to the bull's estimate of $8.85 per share, based on several factors, as summarized below. The High Cost of the K-Cup Brewing System Limits the Market Opportunity Coffee prepared using a K-Cup system cost three to 10 times as much as coffee made with a conventional drip brewer (see Exhibit 13). The Keurig brewing machines were also highly priced (three times the price of similar coffee-brewing machines) and the ongoing cost of coffee in a K-Cup format was at least three times the cost of regular coffee. K-Cups were a luxury item, which limited the market for the product to the high end of the market, as opposed to the entire market of coffee drinkers. While Greenlight had some qualitative arguments that might have led to a lower addressable market estimate, the company chose to be conservative in its assessment of the overall market. Like the bullish analysts, Greenlight estimated that only one-third of the households that drank more than two cups of coffee per day were candidates for the Keurig brewing system and that the total addressable market was 21 million units. As of June 2011, the installed base of Keurig brewers was more than 10 million, as per Greenlight's calculations. With a total addressable market of 21 million units, at the end of the June quarter the Keurig system had penetrated nearly 50 per cent of the total addressable market. Greenlight argued that with 50 per cent of the market penetrated, revenue growth was likely to soon slow significantly. Greenlight's lower earnings estimate was based on several different assumptions: Average Daily K-Cups per Installed Brewing Machine The bull model used a consumption forecast of two average daily K-Cups per brewing machine. Greenlight assumed 1.2 average daily K-Cups per machine in its forecast based on the trend of the calculated actual K-Cup attachment rate (see Exhibit 6). Private Label Market Share Because of the high cost of preparing coffee in the K-Cup format, Greenlight estimated that 20 per cent of the K-Cup market would eventually be private-label coffee as opposed to coffee produced by major brands like Starbucks or Dunkin' Donuts. This assumption reduced Green Mountain's addressable market opportunity by 20 per cent. Sturm Foods, Incorporated (Sturm), a major manufacturer, was already producing filterless K-Cups and planned to enter the market to compete with a filtered K-Cup as soon as Green Mountain's patents expired. Sturm could modify its current production facility with minimal capital investment and believed they could gain substantial penetration into the private label segment of the K-Cup market because the K- Cups were so highly priced relative to their cost to manufacture. An industry expert noted that "Sturm feels that the potential penetration level of single-serve coffee is so much greater than it is for the standard business because the price differentials are going to be huge. I would say that a 20 per cent penetration level would not be a bad number.:16 Major retailers, including The Kroger Co., Safeway Inc., H-E-B, Wegmans Food Markets, Inc. and Costco Wholesale Corporation, told Greenlight that they would be interested in buying a private-label product as soon as a private-label manufacturer could produce a K-Cup-compatible product with a filter. Profit per K-Cup Greenlight estimated that Green Mountain's profit per K-Cup was $0.12. This estimate was based on the bull's estimate of profit per K-Cup (S0.15 for each K-Cups made by Green Mountain - assumed to be 70 per cent of long-term sales) and Greenlight's estimate of $0.06 of profit per K-Cup for non-Green Mountain K-Cups (30 per cent of sales). Revenue for production of non-Green Mountain K-Cups was essentially a manufacturing fee paid by Starbucks and other coffee retailers to Green Mountain to package their coffee into K-Cups. Greenlight presented a compelling, detailed analysis outlining their calculation of the $0.06 of profit per K-Cup for non-Green Mountain K-Cups. Non-Green Mountain K-Cups were growing faster than Green Mountain's K-Cups, resulting in a declining trend in profit per K-Cup. Patent Expirations With Green Mountain's patents set to expire in September 2012, competitors would soon be able to make and sell K-Cups for use in the 10-million-unit installed base of Keurig's machines. The company's business model of selling a brewing machine at cost to create a high margin stream of future K-Cup revenue would therefore be broken and monopoly profits no longer available. Competitors would be able to advertise their K-Cups as compatible with the Keurig brewing system; most of Green Mountain's contracts to produce K-Cups for other coffee brands were non-exclusive. Bullwhip Effect As new retail outlets were added, the sales of products to fill retailers' shelves and distribution centres were included in Green Mountain's revenue. In other words, because new sales outlets had been added, revenue recognized by Green Mountain was higher than end-consumer purchases a phenomenon known the "bullwhip effect. Sales recognized by Green Mountain would continue to be greater than end-customer purchases as more and more new retail and distribution sites were added. As fewer retail sites were added, Green Mountain's growth in recognized revenue would eventually fall below the end- customer growth rate. For example, if Green Mountain had steady sales of $10 million per year and added an additional $1 million-per-year customer at the beginning of the first quarter in the second year, its revenue growth profile would change differently than one may expect (see Exhibit 14). While one might expect revenue growth to be 10 per cent for four consecutive quarters, it must be noted that revenue growth would be inflated by inventory stocking in the first quarter when the new customer is added. Similarly, revenue growth in the first quarter of the following year would be understated because of the comparison to the inflated revenue in the prior year. Many investors would sell Green Mountain stock if it missed revenue growth expectations, even by a small amount. POOR QUALITY OF REPORTED EARNINGS Accounting for Acquisitions Green Mountain has made several acquisitions in recent years. The valuation multiples and allocation of the purchase price to goodwill and intangibles is shown in Exhibit 15. Note that the allocation of the purchase price to goodwill and intangibles is high. High Capital Expenditures Capital expenditures were growing faster than the business at a time when Green Mountain should be achieving greater economies of scale and capital should be deployed more efficiently (see Exhibit 16). Insider Sales A 7,503,883-share offering was completed in May 2011, at $71 per share, with 403,883 shares being sold by directors and officers. Sales by insiders in this offering totaled $29 million. On August 4, 2011, 144 filings were made with the U.S. Securities and Exchange Commission (SEC) for stock sales, as shown below: Robert P. Stiller, Green Mountain's Chairman - $221,920,000 Stiller Family Foundation - $665,760 Green Mountain Coffee Roasters Foundation - $4,161,000 In 2011, there was $172 million in insider sales through September. Shares initially valued at $1.3 billion had been sold by Green Mountain insiders since August 2009. Reports of Possible Financial Misconduct from Ex-employee Interviews18 It was difficult to understand how Green Mountain sold the extra $ 100 million of K-Cups in the June 2011 quarter, but Greenlight's research provided some possible insight. Greenlight interviewed ex- employees of Green Mountain, yielding some troubling information: Revenue Recognition Issues In the June quarter of 2011, Green Mountain sold 1.3 million brewing machines, which exceeded market expectations by about 300,000 units. There are signs that business was not as strong as the report would indicate. During a class action lawsuit filed earlier in 2011, a confidential witness alleged that: Green Mountain improperly recognized revenue on 150 truckloads of product shipped to the company's primary distributor, MBlock, during the quarter that ended December 26, 2009. Green Mountain employees, including the company's global transportation manager, were unable to locate the requisite paperwork, including purchase orders and product shipment authorizations, traditionally used by Green Mountain to validate the sale. . . . Because there was no order for these products, no payment was ever made on the shipment. In addition, the order was not listed on the company's production forecast schedule; however, employees ... not only saw the trucks go out, but visited MBlock and saw its warehouses filled to the rafters with K-Cups. ... The estimated value of the revenue recognized on the improperly recorded transaction was between $7.5 and $15 million.19 Weak Financial Controls Both Green Mountain and MBlock used sub-standard information technology (IT) systems. Important functions, including inventory management, were performed in Excel spreadsheets, which were easy to change, provided non-standardized analysis and were prone to material error. Suggestions to improve operations through the use of new technologies were allegedly met with resistance in both organizations. 20 In addition, Green Mountain's accounting department supposedly used many temporary workers and made extensive use of college intems instead of hiring full-time accountants. Some former Green Mountain workers believed that they were fired for asking too many questions about the company's practices.21 Unusual Inventory Handling and Accounting One ex-employee stated, "We would do more transferring of inventory than actual shipping. ... Keurig would ship stuff to themselves I mean truckloads of stuff... to themselves. A truck driver for Kenco coffee, one of Green Mountain's two U.S. distributors reported delivering merchandise to Kenco only to retrieve it later on and deliver it to a location just 10 bay doors down at the same warehouse.23 There were irregularities during external inventory audits at MBlock: A former MBlock employee noted prior to the inventory audit, We would remove product and pre-load trailer trucks to ship to retailers because we did not have room on the floor. Then we would load more product on trailer trucks to nowhere to move it off the floor. "24 The warehouse was partially cleared prior to an audit, leaving a skeleton inventory of approximately 50 per cent. Inventory was loaded onto trucks where it sat in the docks and was never counted. Sometimes, after the audit, the product would simply be moved back into a warehouse. Immediately prior to an audit, 500,000 brewing machines were inventoried and processed as an order for QVC. The machines were never shipped and after the audit the inventory was restocked. 25 Expired Inventory Interviews with ex-employees found evidence that Green Mountain's inventory contained a large amount of expired product. Channel checks also identified expired product and significant amounts of retail product with short shelf life. An ex-employee noted: "The plant managers just kept saying that excessive space was taken up by the inordinate amount of expired coffee. One ex-employee estimated that, on average, at least one-third of the space in Green Mountain's warehouses was occupied by expired coffee.26 Short interest Short interest for Green Mountain is shown in Exhibit 17. Exhibit 1 STOCK PRICE HISTORY FOR GREEN MOUNTAIN COFFEE ROASTERS (GMCR) $20 GMCR Stock Price $ DO Announcement of SBUX Deal $80 - $60 - Acquisition of Timothy's Acquisition of Van Houtte $40 Acquisition of Tully's Minh $20 - Acquisition of Diedrich $0 Mar Sep Dec Mar Jun Sep OL Dec- DS Mar. Jun 08 Sep DU Dec- 08 Sap 09 Dec- Mar Jun 09 10 10 Sep 10 Dec- 10 Mar. Jun 11 Sep 11 DS 07 07 09 09 Sources: Thomson Reuters; GMCR FY2010 10-K, GMCR 10-Q for 3Q 2011. Exhibit 2 INCOME STATEMENT FOR GREEN MOUNTAIN COFFEE ROASTERS Fiscal Year Ending September millions $ 2008 2009 2010 2011E 2012E Total Revenue 492.5 786.1 1,356.8 2,701.3 4,345.8 Growth yr/yr 46.5% 59.6% 72.6% 99.1% 60.9% COGS 318.5 540.7 931.0 1780.2 2824.8 Gross Profit 174.0 245.4 425.8 921.1 1521.0 Gross Margin % 35.3% 31.2% 31.4% 34.1% 35.0% Total SG&A 129.4 169.0 253.2 504.0 835.4 Operating Income 44.7 76.4 172.6 417.1 685.6 Operating margin % 9.1% 9.7% 12.7% 15.4% 15.8% Net Interst and Other (5.9) (5.4) (5.6) (30.3) (31.9) Pre-Tax Profit 38.7 71.0 167.0 386.8 653.7 Income Taxes 15.0 27.1 61.7 143.7 242.0 Non-GAAP Net Income 23.7 43.9 105.3 243.1 411.7 Non-GAAP EPS $0.21 $0.36 $0.76 $1.61 $2.59 Exhibit 3 CASH FLOW FOR GREEN MOUNTAIN COFFEE ROASTERS FY 2006 millions $ Revenue Non-GAAP Net Income FY 2007 $492.5 $23.7 FY 2008 $786.1 $43.9 FY 2009 $1,256.8 $105.3 FY 2010 YTD 2011 $2,701.3 $243.1 Cash Flow from Operations Capital Expenditures Acquisitions Free Cash Flow Cumulative Free Cash Flow $12.8 - 13.6 -101.1 ($101.9) ($101.9) $29.8 -21.8 0 $8.0 ($93.9) $1.9 -48.7 $0.0 ($46.8) ($140.7) $38.5 -48.3 -41.4 ($51.2) ($191.9) -$10.5 $174.7 -118 - 175.5 -459.5 -907.8 ($588.0) ($908.6) ($779.9) ($1,688.5) Note: YTD 2011 represents 39 weeks ended June 25, 2011. Source: GMCR 10-K's for 2010, 2009, 2008. GMCR 10-Q for Q3 2011. Exhibit 4 RETURN ON INVESTED CAPITAL 2013 Bull Case EPS (1) Shares Outstanding Implied Net Income $4.00 160 640 Estimated net Working capital (2) Acquisitions (3) Net Fixed Assets as of Q3 2011 CapEx in Q4 2011 (4) CapEx in FY 2012 (4) Total Invested Capital 1,120.0 1,409.1 499.1 162.0 740.0 3,930.2 Return on Invested Capital 16.3% Exhibit 5 YEAR-OVER-YEAR CHANGE IN ATTACHMENT RATE Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 -15% - 13% -15% -12% -15% -18% -14% -7% -12% - 13% 11% Average Year-over-Year Change in Attachment Rate excluding June 2011 = -13% Source: Greenlight estimates. The number of brewers in the installed base is determined by adding up all the brewers sold in the prior 36 months. The attachment rate is calculated by dividing the average number of K-Cups sold per day in the quarter by the number of brewers in the installed base. The year-over-year change in attachment rate is calculated by comparing the current quarter attachment rate to the same quarter in the prior year. Exhibit 6 K-CUP FORECAST MODEL Until June 2011, K-Cup sales have been predictable Units in millions Estimated Installed Brewer Base Predicted Attachment Rate Predicted K-Cup Units Actual Attachment Rate Actual K-Cup Units Difference In K-Cups Surprise (percentage) Dec Mar Jun Sep Dec Mar Jun FY 2010 FY 2010 FY 2010 FY 2010 FY 2011 FY 2011 FY 2011 4.7 5.3 5.9 6.8 8.6 9.6 10.6 1.54 1.58 1.27 1.34 1.31 1.30 1.10 666 764 690 775 1,034 1,142 1,058 1.51 1.49 1.26 1.33 1.33 1.30 1.39 650 720 683 832 1,046 1,146 1,346 (16) (44) (7) 57 12 3 288 -2% -6% -1% 7% 0% 27% 1% Exhibit 7 ENTERPRISE VALUE/REVENUE MULTIPLE AND YEAR OVER YEAR REVENUE GROWTH RATE 6.0 140% Yr/Yr Revenue Growth -EV/LTM Revenue 120% 5.0 100% 4.0 80% EV/LTM Revenue 3.0 YrYr Revenue Growth Rate 60% 2.0 40% 1.0 20% 0.0 9/28/2002 0% 6/25/2011 1/17/2004 4/9/2005 7/1/2006 9/29/2007 12/27/2008 3/27/2010 Exhibit 8 ENTERPRISE VALUE CALCULATION Stock Price $92.09 Diluted Shares Outstanding 158.80 Market Capitalization 14,62T Net Debt 315 Enterprise Value $14,936 Million Source: Bloomberg consensus estimates as of October 13, 2011. Market valuation metrics as of October 14, 2011. Exhibit 9 VALUATION MULTIPLES $ Multiple Green Mountain 5.5x Revenue 2011E Revenue 2012E $2,701 $4,346 3.4x 434 EBIT 2011E EBIT 2012E 34.4x 21.4x 697 EPS 2011E $1.61 57.2x 35.6x EPS 2012E $2.59 S&P 500 EPS 2011E EPS 2012E $97.03 $112.00 12.4x 10.7x Source: Bloomberg consensus estimates as of October 13, 2011. Market valuation metrics as of October 14, 2011. Exhibit 10 RETAIL DISTRIBUTION TRENDS 40,000 Supermarket Locations Retail Stores 35,000 30,000 15,2001 14,400 25,000 10,000 20,000 15,000 2,600 1,300 10,000 19,000 20,000 17,900 13,800 5,000 10,000 7,000 3,500 0 Dec 2004 Dec 2005 Dec 2006 Dec 2007 Dec 2008 Dec 2009 Dec 2010 Jun 2011 ource: GMCR presentation given at conference on August 10, 2011 (approximate totals based on company estimates). Exhibit 11 LONG-TERM EPS - BULL CASE EARNINGS MODEL Bull Case: Green Mountain Can Earn $8-10 per Share Target Market (Homes that brew 2+ cups/day) Forecast Keurig share of Target Market Fully Penetrated Installed Brewer Base Average Daily K-Cups Per Brewer Days/Year Annual K-Cup Production Profit per K-Cup Annual K-Cup profit (EBIT) Annual K-Cup Profit (After tax and Interest) Shares Outstanding Long Term EPS (At Home Sales) 64M 33% 21M 2.00 365 15,558M $0.15 $2,352M $1,440M 160 $9.00 Exhibit 12 LONG TERM EPS BULL CASE VERSUS BEAR CASE Target Market (Homes that brew 2+ cups/day) Forecast Keurig share of Target Market Fully Penetrated Installed Brewer Base Average Daily K-cups Per Brewer Market Share Captured by Private label Days/Year Annual K-cup Production Profit per K-cup Annual K-cup profit (EBIT) Annual K-cup Profit (After tax and Interest) Shares Outstanding Long Term EPS (At Home Sales) Bull Case Bear Case 64M 64M 33% 33% 21M 21M 2.00 1.25 0.20 365 365 15,418M 7,709M $0.15 $0.12 $2.313M $925M $1,415M $555M 160 160 $8.85 $3.47 Note: Assumes $30 million interested expense, 38% tax rate and 160M shares. Data edited to correct rounding errors in original data sources. Bull Case Source: Sun Trust Robertson Humphrey research note published July 21, 2011 Bear Case Source: Greenlight. Exhibit 13 COST PER SERVING - K-CUPS VERSUS DRIP-BREWING METHODS K-Cups Are Expensive Price $ Servings Per Serving 270 8.86 10.78 270 3.3 4.0 2.8 4.0 7.48 270 270 10.78 Brand Drip - Lower End Folgers: Custom Roast Ground Folgers: Medium Classic Roast Maxwell House: Daily Brew Ground Maxwell House: Tassimo Classic Roast Drip - Higher End Dunkin Donuts: Ground Coffee (40 oz) Dunkin Donuts: Original Blend Starbucks: Sumatra (1 lb) Starbucks: Breakfast Blend (1 lb) K-Cup - Lower End Folgers: Black Silk Dark Roast GMCR: Breakfast Blend Tully's (GMCR): Kona Blend GMCR: Donut House Regular K-Cup - Higher End Barista Prima (GMCR) Coffeehouse Blend Caf Escapes (GMCR): Chai Latte Dunkin Donuts: Original Blend 21.73 24.35 14.95 11.95 113 113 45 45 19.2 21.5 33.0 26.3 11.28 16.28 11.99 11.99 18 24 18 18 62.7 67.8 66.6 66.6 14.99 12.99 11.99 18 16 14 83.3 81.24 85.6 Exhibit 14 BULLWHIP EFFECT Impact of Inventory Stocking on Revenue Growth Year 1 Q2 Year 2 Q2 Year 3 Q2 ar Q1 Q3 04 Q1 Q3 Q4 Q1 Q3 Q4 $2.5 $2.5 $2.5 $2.5 $2.5 $2.5 $2.5 $2.5 $2.5 $2.5 $2.5 $2.5 0 0 0 0 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 Base Business New Customer sales to end consumer New Customer sales to meet inventory needs Total revenue Yr/Yr revenue growth 0.08 $2.50 $2.50 $2.50 $2.50 $2.83 $2.75 $2.75 $2.75 $2.75 $2.75 $2.75 $2.75 13.2% 10.0% 10.0% 10.0% 2.8% 0.0% 0.0% 0.0% In the example above, if a retaller holds 30 days of inventory, which is typical for a grocery store, then a retaler which buys $1 million in K-Cups per year for resale will have to also hold $0.08 million of K-Cups in inventory at any time. If it becomes a retailer for Green Mountain at the beginning of Q1 in Year 2, it will buy $0.25 million of K-Cups for sale to end customers and $0.08 million in product to hold in inventory for a total of $2.83 million. In other words, 24% (0.08/(0.25+0.08)) of the revenue for the first quarter for the new customer will be to build inventory, not for sales to end customers. Exhibit 15 GREEN MOUNTAIN'S MAJOR ACQUISITIONS Van Houtte Acquisition Date (1) Acquisition Price (1) Revenue (7) Tully's Mar 27 '09 $40.3M $30.4M Timothy's Nov 13 '09 $155.7M $43.7M 3.6x Diedrich May 11 '10 $305.3M $86.5M 3.5x Dec 17 '10 $907.8M $443.0M 1.3x 2.Ox na n/a $7.4M $91.6M 9.9x 41.3x Multiple (EV/Revenue) EBITDA) Multiple (EV/EBITDA) Approx.% of system-wide K-cups) Allocation of Price to Goodwill ) Allocation of Price to Intangibles (" Allocation of Price to GW & Int. . % of Purchase Price n/a 3% $25.8M $12.4M n/a 12-13% $69.3M 12-13% $217.5M $100.2M $317.7M 104% $98.3M $167.6M 108%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting An Introduction

Authors: Eddie McLaney, Dr Peter Atrill, Eddie J. Mclan

5th Edition

0273733206, 978-0273733201