Answered step by step

Verified Expert Solution

Question

1 Approved Answer

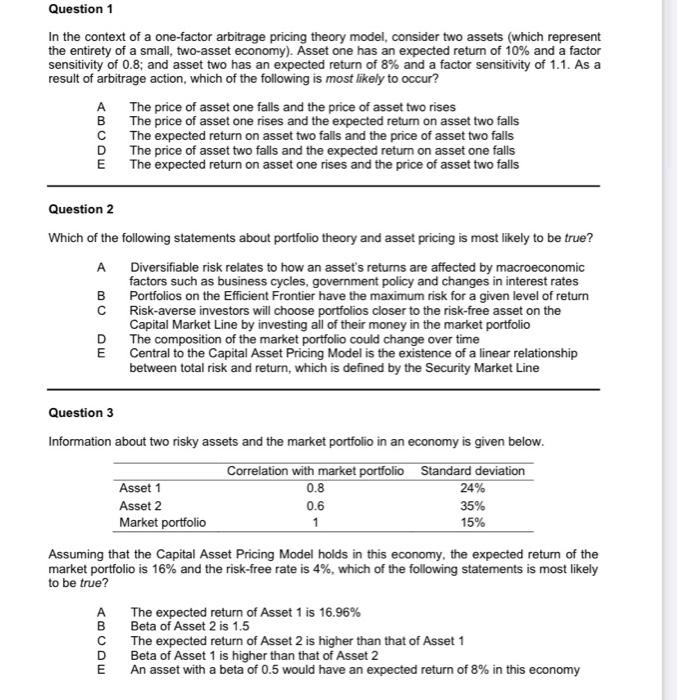

Question 1 In the context of a one-factor arbitrage pricing theory model, consider two assets (which represent the entirety of a small, two-asset economy). Asset

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Comprehensive Guide To Information Security Management And Audit

Authors: Rajkumar Banoth, Gugulothu Narsimha, Aruna Kranthi Godishala

1st Edition

1032344431, 978-1032344430