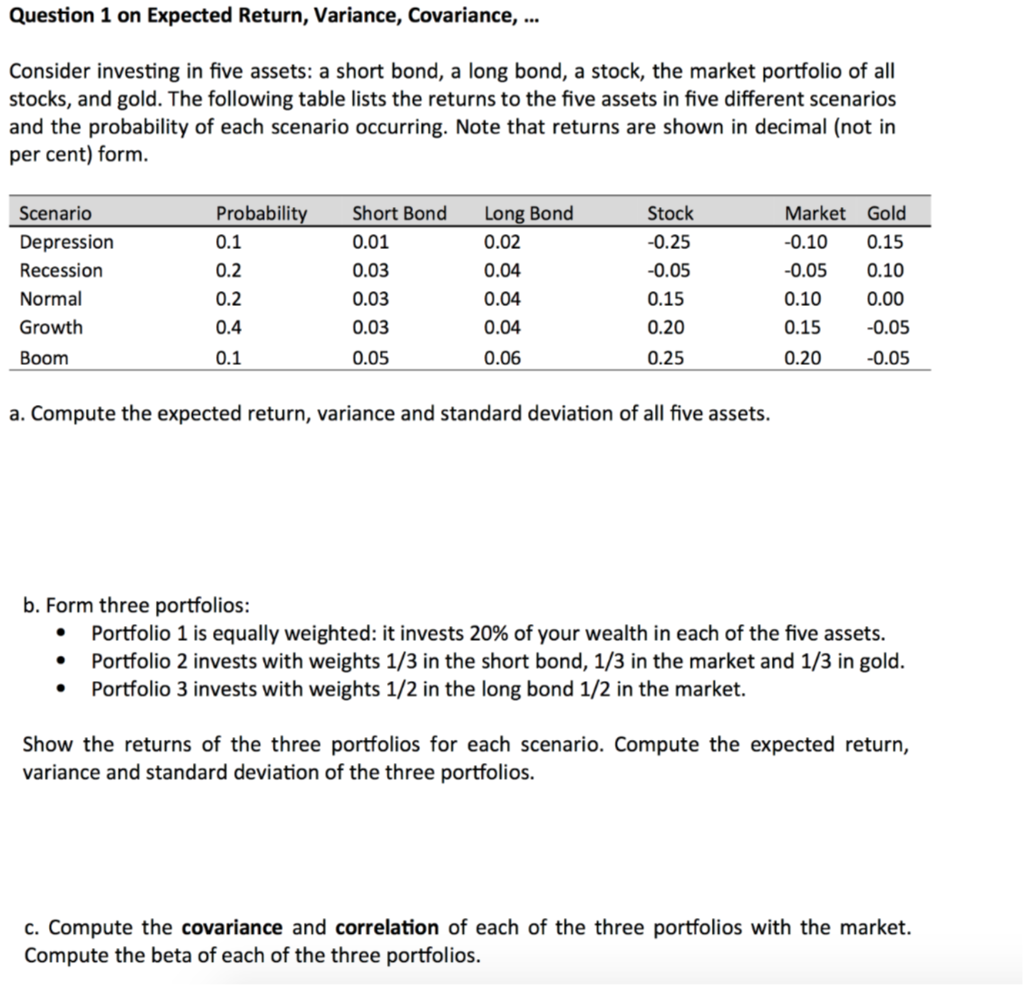

Question 1 on Expected Return, Variance, Covariance, ... Consider investing in five assets: a short bond, a long bond, a stock, the market portfolio of all stocks, and gold. The following table lists the returns to the five assets in five different scenarios and the probability of each scenario occurring. Note that returns are shown in decimal (not in per cent) form. Scenario Depression Recession Normal Growth Boom Probability 0.1 0.2 0.2 Short Bond 0.01 0.03 0.03 0.03 0.05 Long Bond 0.02 0.04 0.04 0.04 0.06 Stock -0.25 -0.05 0.15 0.20 0.25 Market Gold -0.10 0.15 -0.05 0.10 0.10 0.00 0.15 -0.05 0.20 -0.05 04 0.1 a. Compute the expected return, variance and standard deviation of all five assets. b. Form three portfolios: Portfolio 1 is equally weighted: it invests 20% of your wealth in each of the five assets. Portfolio 2 invests with weights 1/3 in the short bond, 1/3 in the market and 1/3 in gold. Portfolio 3 invests with weights 1/2 in the long bond 1/2 in the market. Show the returns of the three portfolios for each scenario. Compute the expected return, variance and standard deviation of the three portfolios. c. Compute the covariance and correlation of each of the three portfolios with the market. Compute the beta of each of the three portfolios. Question 1 on Expected Return, Variance, Covariance, ... Consider investing in five assets: a short bond, a long bond, a stock, the market portfolio of all stocks, and gold. The following table lists the returns to the five assets in five different scenarios and the probability of each scenario occurring. Note that returns are shown in decimal (not in per cent) form. Scenario Depression Recession Normal Growth Boom Probability 0.1 0.2 0.2 Short Bond 0.01 0.03 0.03 0.03 0.05 Long Bond 0.02 0.04 0.04 0.04 0.06 Stock -0.25 -0.05 0.15 0.20 0.25 Market Gold -0.10 0.15 -0.05 0.10 0.10 0.00 0.15 -0.05 0.20 -0.05 04 0.1 a. Compute the expected return, variance and standard deviation of all five assets. b. Form three portfolios: Portfolio 1 is equally weighted: it invests 20% of your wealth in each of the five assets. Portfolio 2 invests with weights 1/3 in the short bond, 1/3 in the market and 1/3 in gold. Portfolio 3 invests with weights 1/2 in the long bond 1/2 in the market. Show the returns of the three portfolios for each scenario. Compute the expected return, variance and standard deviation of the three portfolios. c. Compute the covariance and correlation of each of the three portfolios with the market. Compute the beta of each of the three portfolios