Answered step by step

Verified Expert Solution

Question

1 Approved Answer

QUESTION 1: QUESTION 2: QUESTION 3: QUESTION 4: QUESTION 5: If possible please fill out form 4562 from the IRS b. Compute the maximum 2023

QUESTION 1:

QUESTION 2:

QUESTION 3:

QUESTION 4:

QUESTION 5:

If possible please fill out form 4562 from the IRS

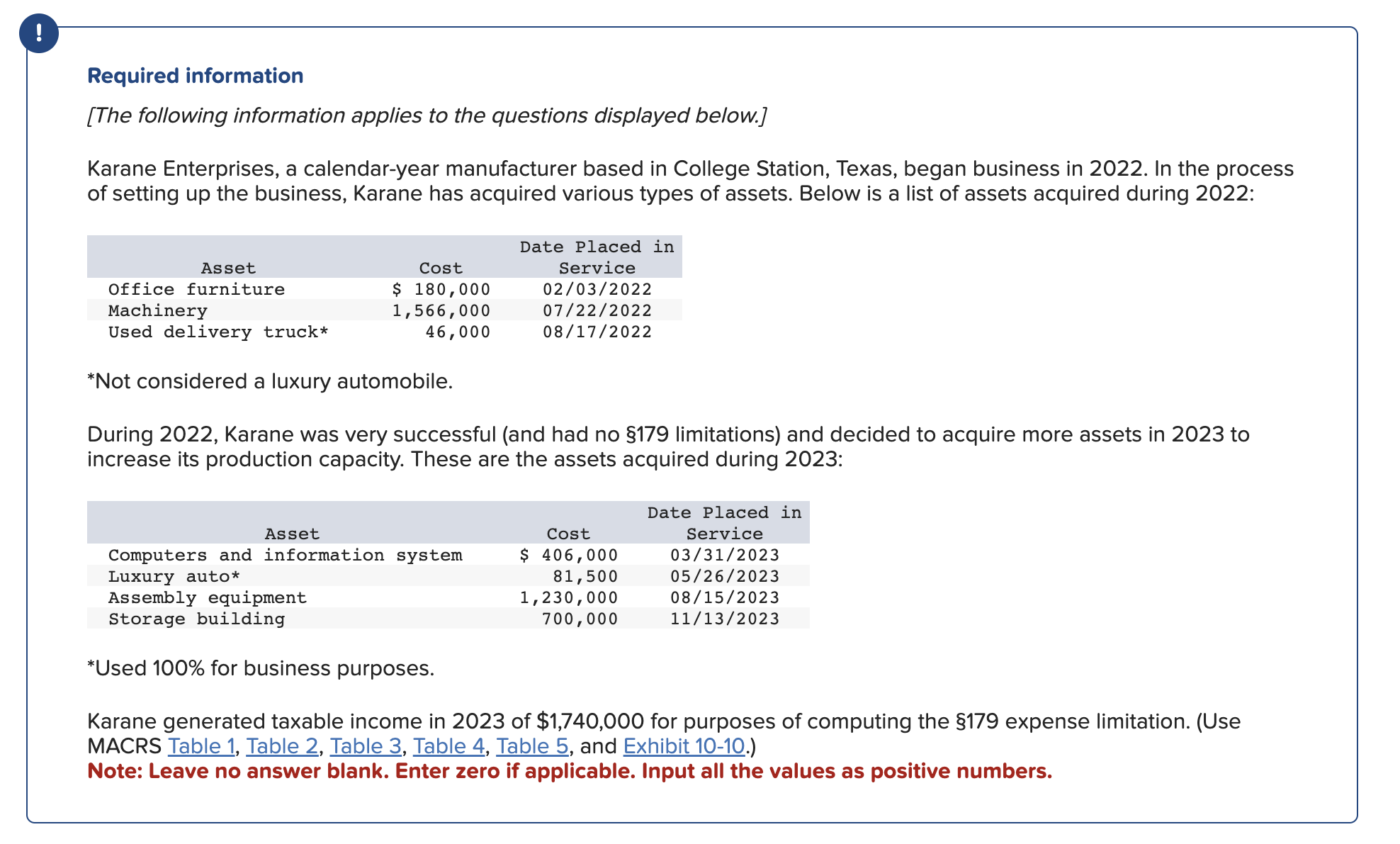

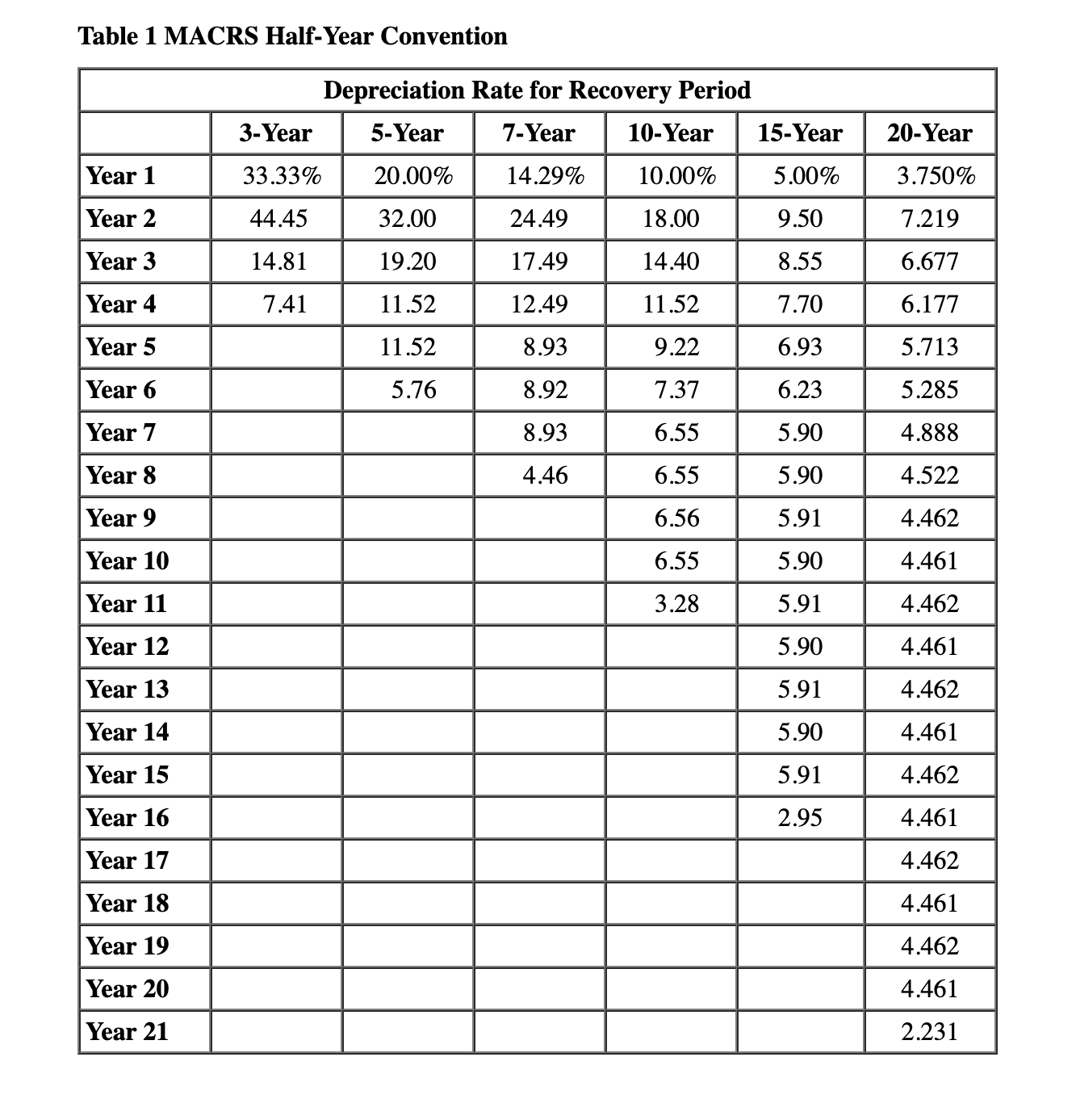

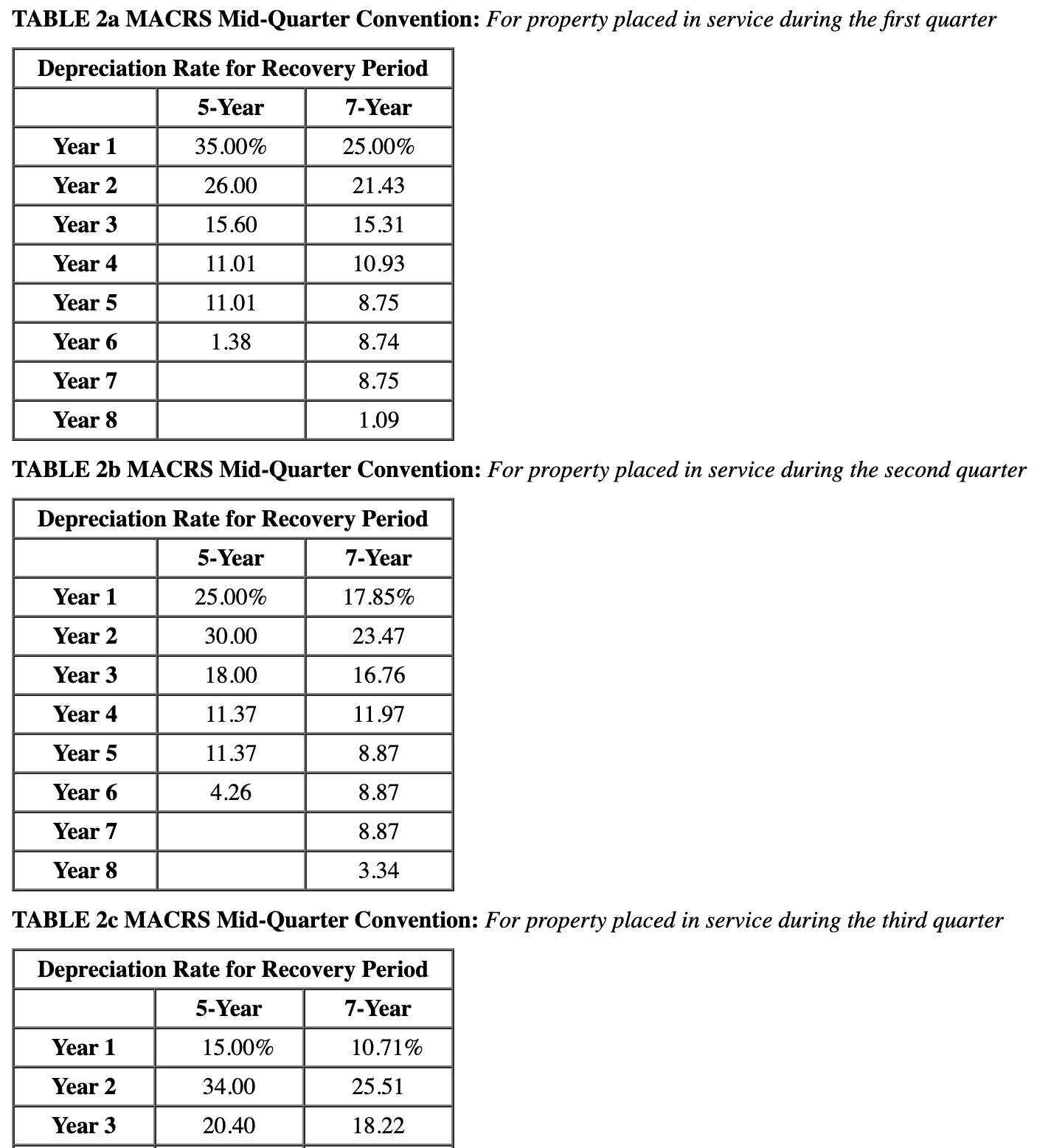

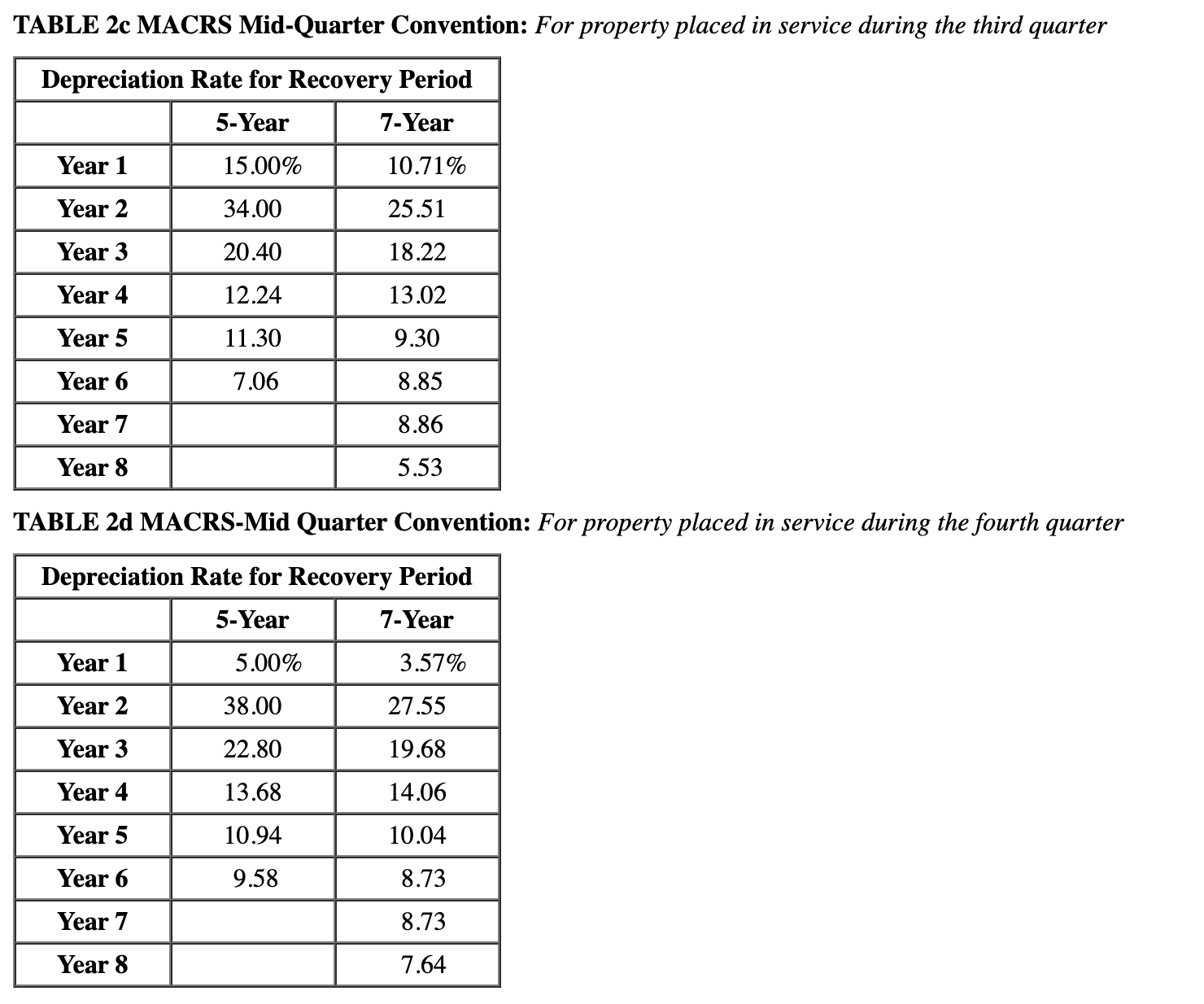

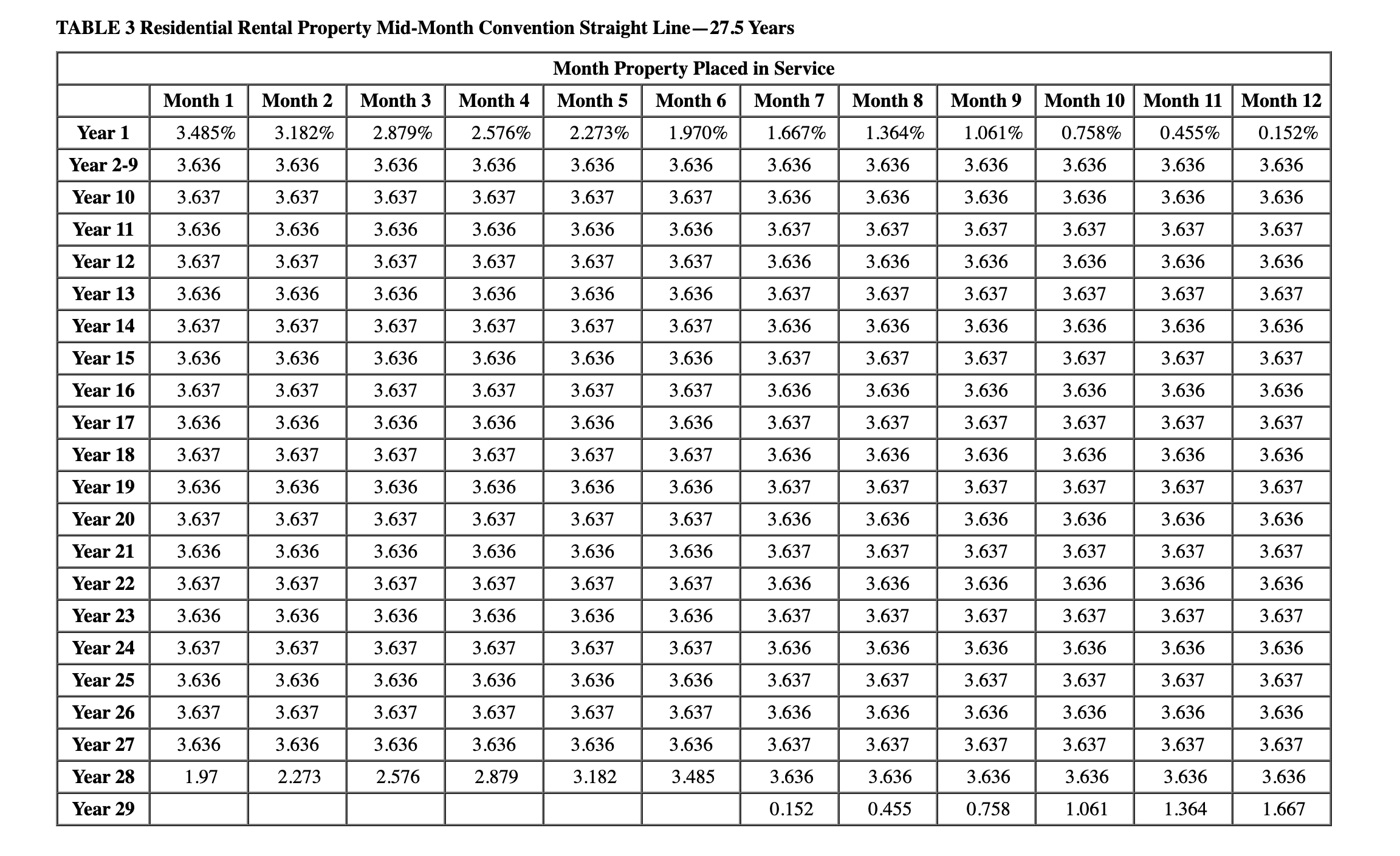

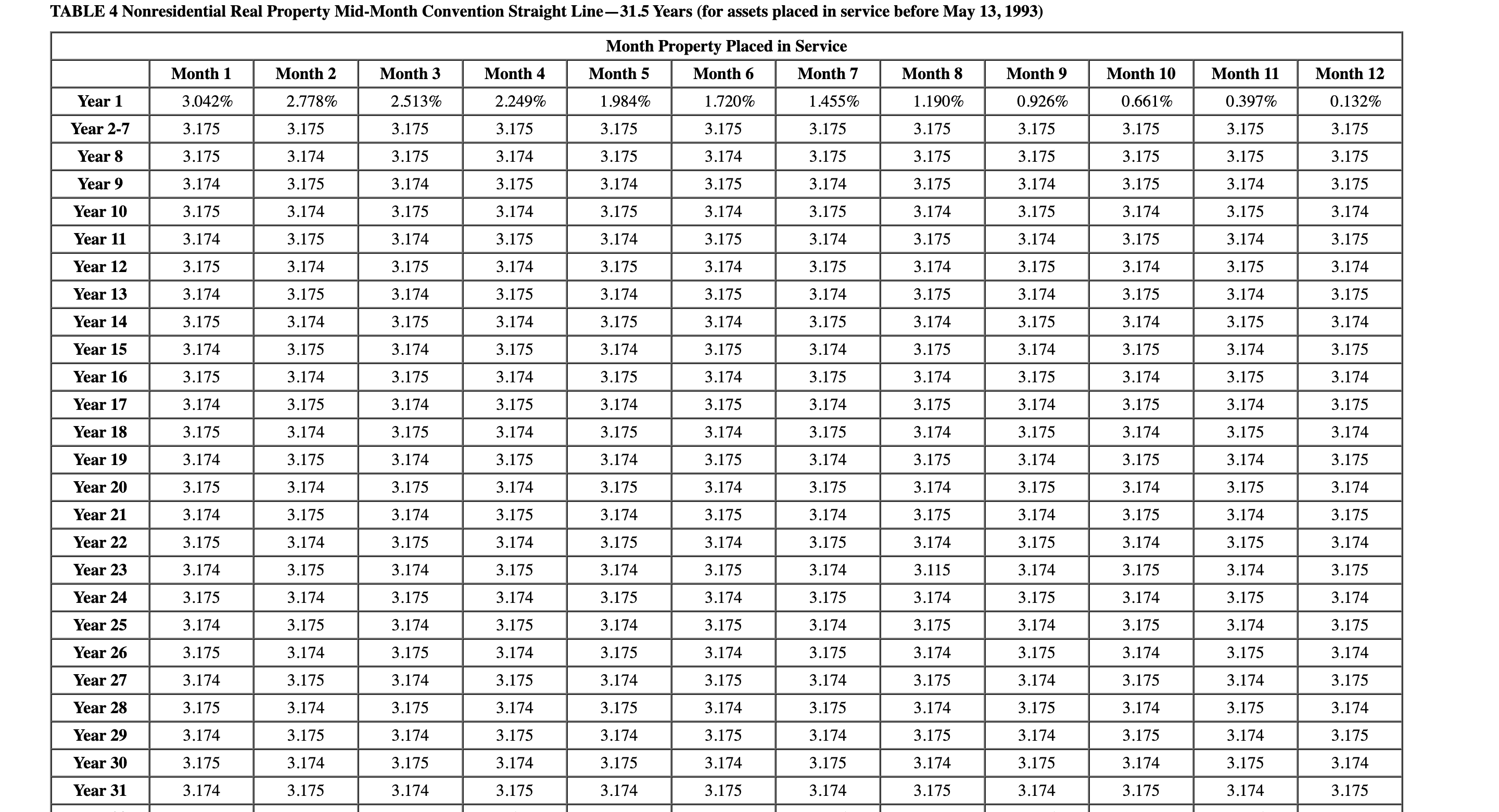

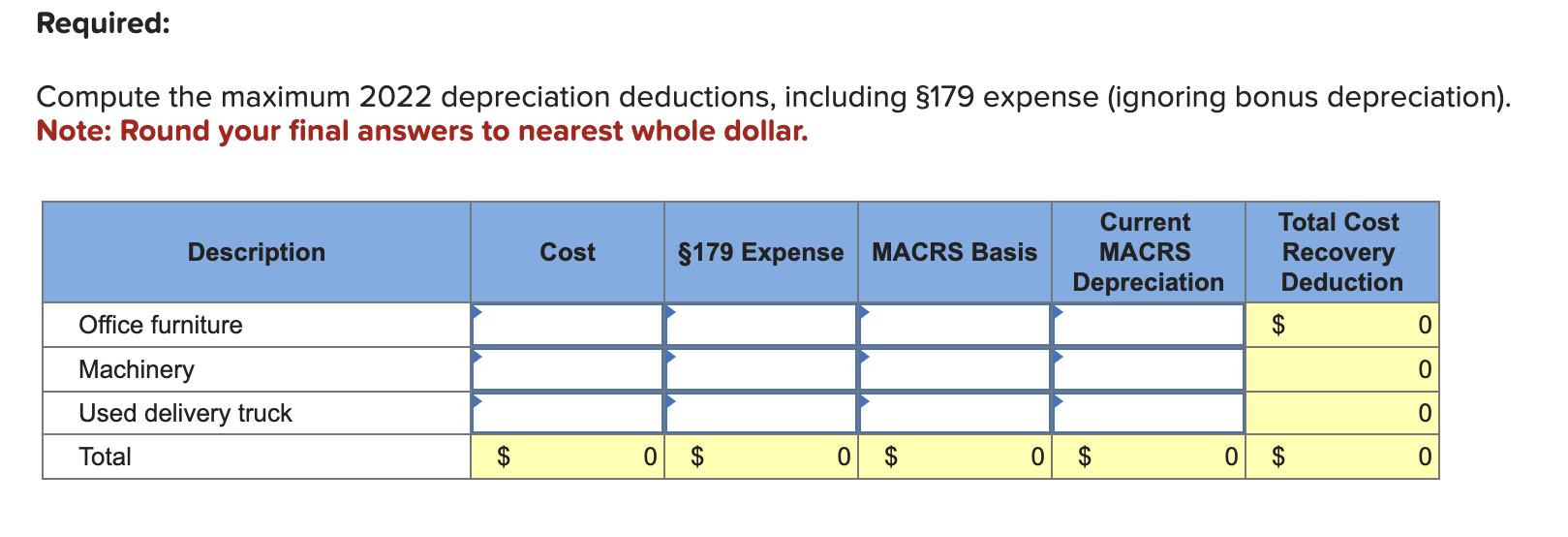

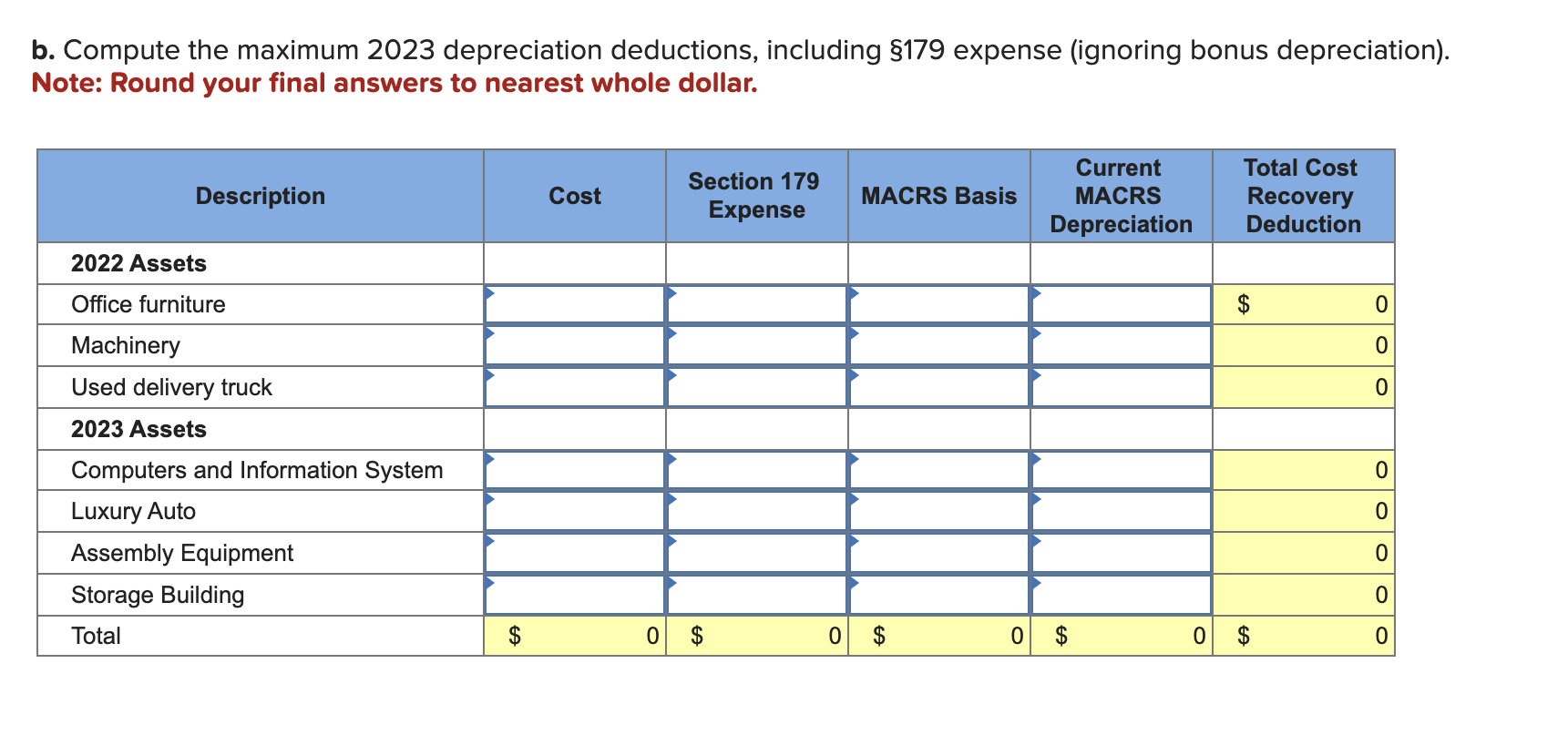

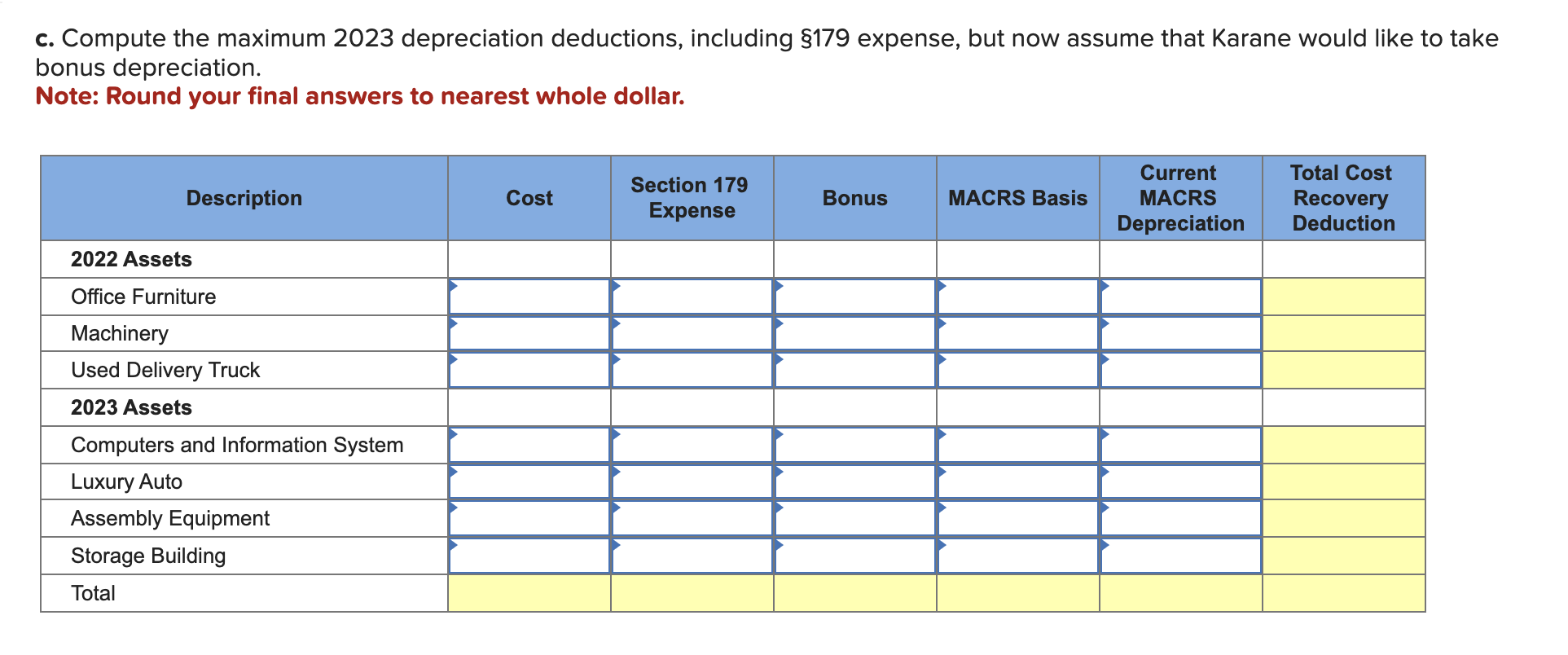

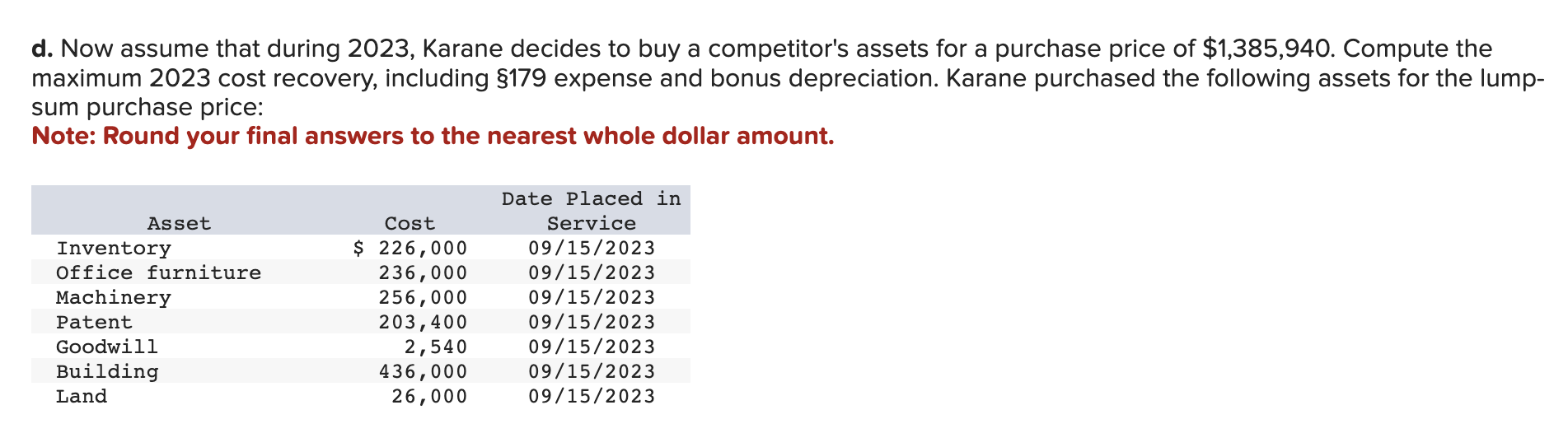

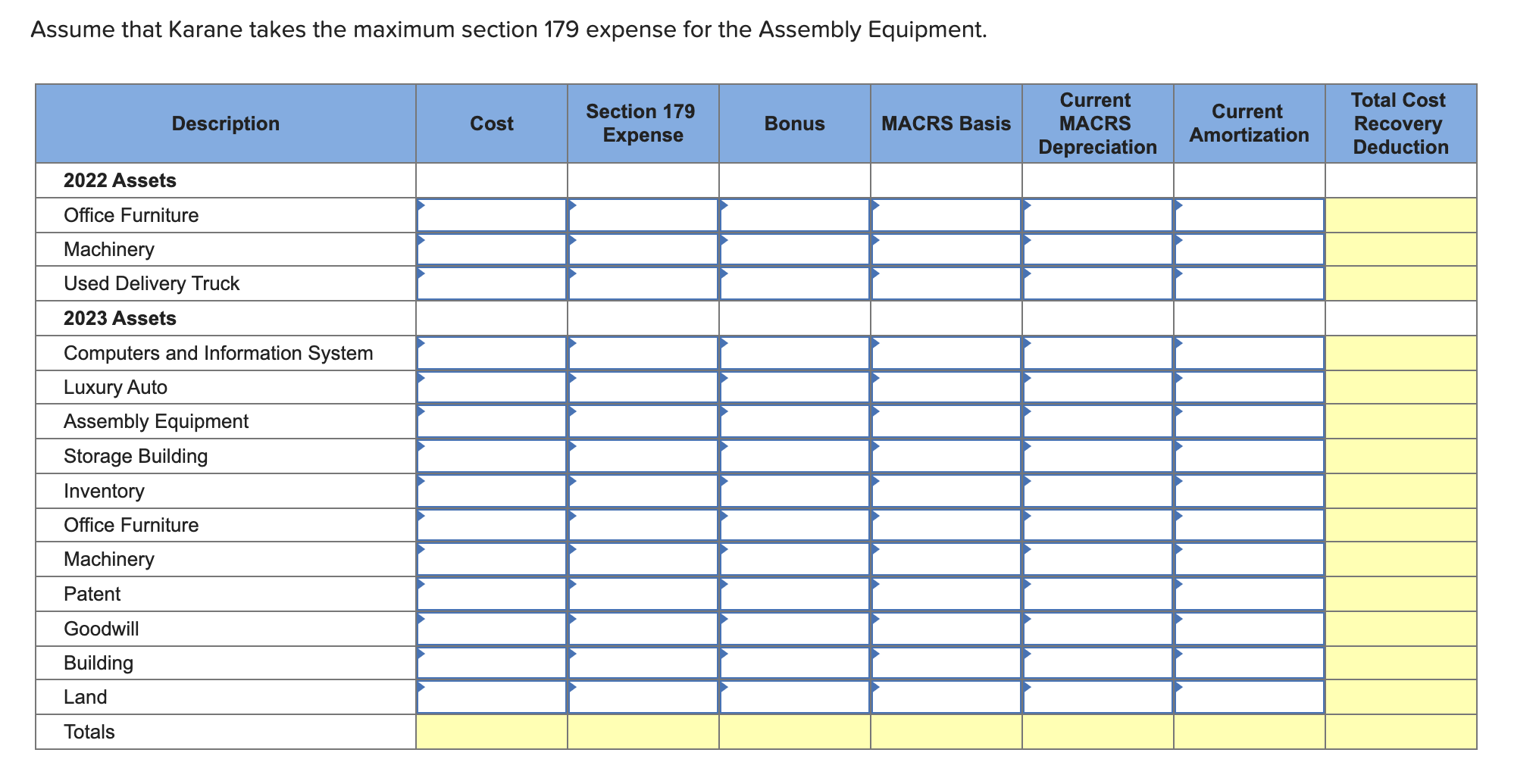

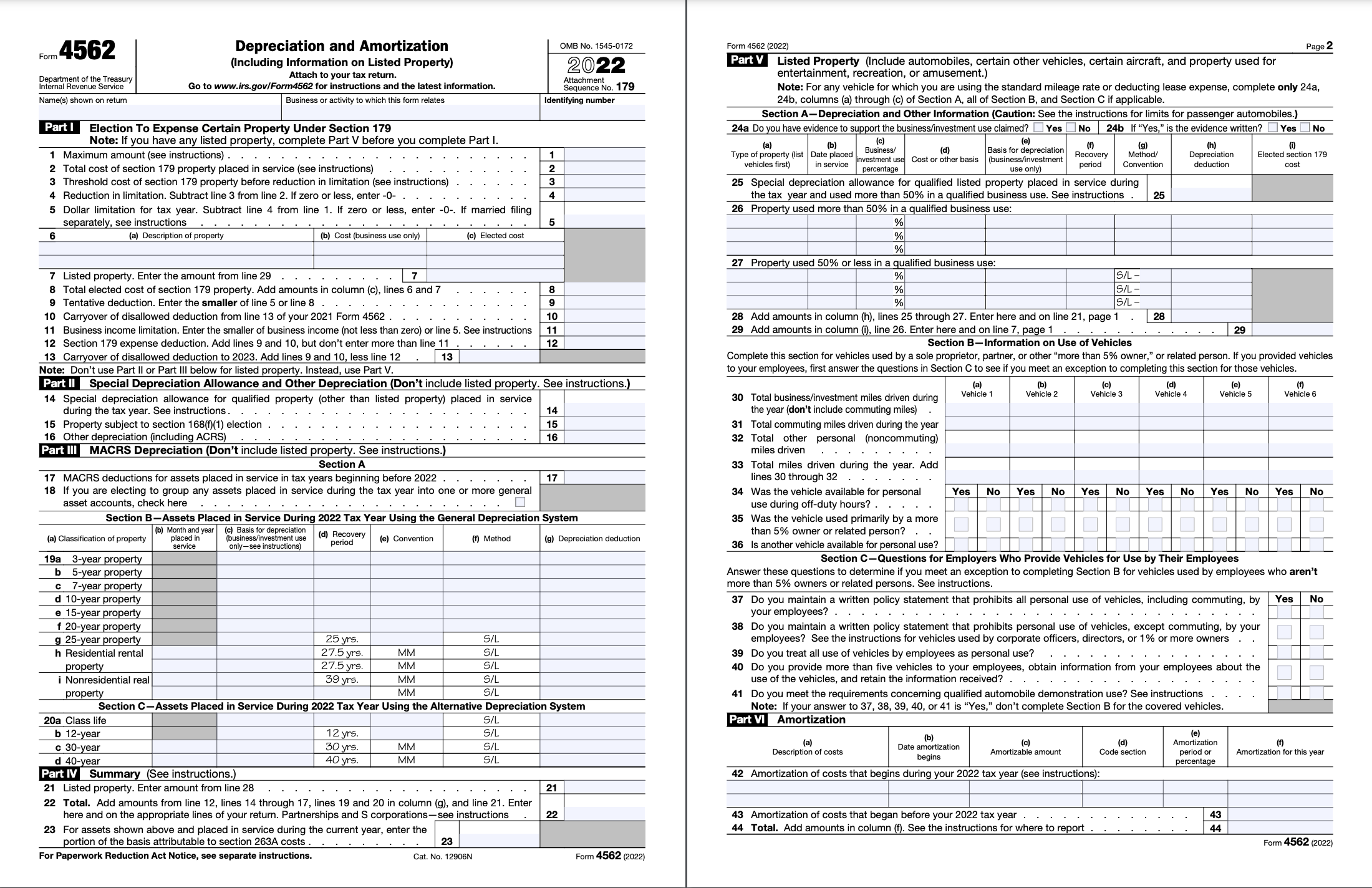

b. Compute the maximum 2023 depreciation deductions, including $179 expense (ignoring bonus depreciation). Note: Round your final answers to nearest whole dollar. TABLE 2c MACRS Mid-Quarter Convention: For property placed in service during the third quarter Compute the maximum 2022 depreciation deductions, including $179 expense (ignoring bonus depreciation). Note: Round your final answers to nearest whole dollar. Table 1 MACRS Half-Year Convention TABLE 2c MACRS Mid-Quarter Convention: For property placed in service during the third quarter \begin{tabular}{|c|c|c|} \hline \multicolumn{3}{|c|}{ Depreciation Rate for Recovery Period } \\ \hline & 5-Year & 7-Year \\ \hline Year 1 & 15.00% & 10.71% \\ \hline Year 2 & 34.00 & 25.51 \\ \hline Year 3 & 20.40 & 18.22 \\ \hline Year 4 & 12.24 & 13.02 \\ \hline Year 5 & 11.30 & 9.30 \\ \hline Year 6 & 7.06 & 8.85 \\ \hline Year 7 & & 8.86 \\ \hline Year 8 & & 5.53 \\ \hline \end{tabular} TABLE 2d MACRS-Mid Quarter Convention: For property placed in service during the fourth quarter \begin{tabular}{|c|c|c|} \hline \multicolumn{3}{|c|}{ Depreciation Rate for Recovery Period } \\ \hline & 5-Year & 7-Year \\ \hline Year 1 & 5.00% & 3.57% \\ \hline Year 2 & 38.00 & 27.55 \\ \hline Year 3 & 22.80 & 19.68 \\ \hline Year 4 & 13.68 & 14.06 \\ \hline Year 5 & 10.94 & 10.04 \\ \hline Year 6 & 9.58 & 8.73 \\ \hline Year 7 & & 8.73 \\ \hline Year 8 & & 7.64 \\ \hline \end{tabular} Assume that Karane takes the maximum section 179 expense for the Assembly Equipment. TABLE 3 Residential Rental Property Mid-Month Convention Straight Line-27.5 Years d. Now assume that during 2023 , Karane decides to buy a competitor's assets for a purchase price of $1,385,940. Compute the maximum 2023 cost recovery, including $179 expense and bonus depreciation. Karane purchased the following assets for the lumpsum purchase price: Note: Round your final answers to the nearest whole dollar amount. \begin{tabular}{|c|c|c|c|c|c|c|c|c|} \hline \multirow{2}{*}{\begin{tabular}{l|} Form 4562 \\ Department of the Treasury \\ Internal Revenue Service \end{tabular}} & \multirow{2}{*}{\multicolumn{6}{|c|}{DepreciationandAmortization(IncludingInformationonListedProperty)Attachtoyourtaxreturn.Gotowww.irs.gov/Form4562forinstructionsandthelatestinformation.}} & \multicolumn{2}{|r|}{ OMB No. 1545-0172 } \\ \hline & & & & & & & \multicolumn{2}{|c|}{\begin{tabular}{|c|c|c|} 2(0)22 \\ Attachment \\ Sequence No. 179 \end{tabular}} \\ \hline \multicolumn{3}{|l|}{ Name(s) shown on return } & \multicolumn{4}{|c|}{ Business or activity to which this form relates } & \multicolumn{2}{|c|}{ Identifying number } \\ \hline \multicolumn{9}{|c|}{PartIElectionToExpenseCertainPropertyUnderSection179Note:Ifyouhaveanylistedproperty,completePartVbeforeyoucompletePartI.} \\ \hline & 1 & \\ \hline & & & & & & & 2 & \\ \hline & & & & & & & 3 & \\ \hline & & & & & & & 4 & \\ \hline & & & & & & & 5 & \\ \hline \multicolumn{4}{|c|}{ (a) Description of property } & \multicolumn{2}{|c|}{ (b) Cost (business use only) } & (c) Elected cost & & \\ \hline \multicolumn{8}{|c|}{7 Listed property. Enter the amount from line 29} & \\ \hline \multirow{6}{*}{\multicolumn{7}{|c|}{89101112Totalelectedcostofsection179property.Addamountsincolumn(c),lines6and7Tentativededuction.Enterthesmallerofline5orline8Carryoverofdisalloweddeductionfromline13ofyour2021Form4562.Businessincomelimitation.Enterthesmallerofbusinessincome(notlessthanzero)orline5.SeeinstructionsSection179expensededuction.Addlines9and10,butdontentermorethanline11}} & 8 & \\ \hline & & & & & & & 9 & \\ \hline & & & & & & & 10 & \\ \hline & & & & & & & 11 & \\ \hline & & & & & & & 12 & \\ \hline & & & & & & & & \\ \hline \multicolumn{9}{|c|}{ Note: Don't use Part II or Part III below for listed property. Instead, use Part V. } \\ \hline \multicolumn{9}{|c|}{ Part II Special Depreciation Allowance and Other Depreciation (Don't include listed property. See instructions.) } \\ \hline \multirow{4}{*}{\multicolumn{7}{|c|}{14Specialdepreciationallowanceforqualifiedproperty(otherthanlistedproperty)duringthetaxyear.Seeinstructions.15Propertysubecttosection168(f)(1)election.16Otherdepreciation(includingACRS)}} & 14 & \\ \hline & & & & & & & 15 & \\ \hline & & & & & & & 16 & \\ \hline & & & & \multicolumn{5}{|c|}{ Part III MACRS Depreciation (Don't include listed property. See instructions.) } \\ \hline \multicolumn{9}{|c|}{ Section A} \\ \hline 17 MACRS deductions & for assets pla & ced in service & in taxy & ears beginnin & ng before 2022 & & 17 & \\ \hline 18Ifyouareelectingassetaccounts,ch & togroupanyaeckhere.. & assets placed & in servi & ice during the & tax year into & one or more general & & \\ \hline Section B & -Assets Plac & ed in Service & During & g 2022TaxYe & ear Using the & General Depreciation & n Syste & \\ \hline (a) Classification of property & (b)Monthandyearplacedinservice & \begin{tabular}{|l|l} (c) Basis for dep \\ (businesslivivestry \\ only-see instru \end{tabular} & reciationnenttusections) & \begin{tabular}{|c|} (d) Recovery \\ period \end{tabular} & (e) Convention & (f) Method & (g) De & epreciation deduction \\ \hline 19a 3 -year property & & & & & & & & \\ \hline b 5-year property & & & & & & & & \\ \hline c 7-year property & & & & & & & & \\ \hline d 10-year property & & & & & & & & \\ \hline e 15-year property & & & & & & & & \\ \hline f 20-year property & & & & & & & & \\ \hline g 25-year property & & & & 25 yrs. & & S/L & & \\ \hline h Residential rental & & & & 27.5yrs. & MM & S/L & & \\ \hline property & & & & 27.5yrs. & MM & S/L & & \\ \hline i Nonresidential real & & & & 39yrs. & MM & S/L & & \\ \hline property & & & & & MM & S/L & & \\ \hline Section C- & -Assets Place & d in Service & During 2 & 2022 Tax Yea & ar Using the A & Alternative Depreciatic & on Sys & stem \\ \hline 20a Class life & & & & & & S/L & & \\ \hline b 12-year & & & & 12yrs. & & S/L & & \\ \hline c 30-year & & & & 30 yrs. & MM & S/L & & \\ \hline d 40-year & & & & 40yrs. & MM & S/L & & \\ \hline Part IV Summary & See instructio & ns.) & & & & & & \\ \hline 21 Listed property. En & ter amount fron & m line 28 & & . & . & . . & 21 & \\ \hline 22Total.Addamounhereandontheap & tsfromline12,propriatelines & lines14throuofyourreturn. & ugh17,Partner & lines19andrshipsandS & 20incolumncorporations- & (g),andline21.Enter-seeinstructions & 22 & \\ \hline 23Forassetsshownaportionofthebasis & boveandplacattributableto & edinservicesection263A & duringthcosts. & he current ye & ar, enter the & 23 & & \\ \hline \end{tabular} Form 4562 (2022) Page 2 Include automobiles, certain other vehicles, certain aircraft, and property used for entertainment, recreation, or amusement.) Note: For any vehicle for which you are using the standard mileage rate or deducting lease expense, complete only 24a, 24b, columns (a) through (c) of Section A, all of Section B, and Section C if applicable. Section A-Depreciation and Other Information (Caution: See the instructions for limits for passenger automobiles.) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|} \hline 24a Do you have e & evidence to su & upport the bu & Isiness/investment u & se claimed? & No & 24b If & Yes," i & he evidence w & en? & Yes \\ \hline (a)Typeofproperty(listvehiclesfirst) & \begin{tabular}{|c|} (b) \\ Date placed \\ in service \end{tabular} & \begin{tabular}{|c|} (c) \\ Business/ \\ investment use \\ percentage \\ \end{tabular} & (d)Costorotherbasis & \begin{tabular}{|c|} (e) \\ Basisfordepreciation(business/investmentuseonly) \\ \end{tabular} & (f)Recoveryperiod & MetConv & & (h)Depreciationdeduction & & (i)ectedsection179cost \\ \hline 5 & & & & & & & 25 & & & \\ \hline \end{tabular} 26 Property used more than 50% in a qualified business use: 27 Property used 50% or less in a qualified business use: Complete this section for vehicles used by a sole proprietor, partner, or other "more than 5% owner," or related person. If you provided vehicles to your employees, first answer the questions in Section C to see if you meet an exception to completing this section for those vehicles. \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline 30 & Totalbusiness/investmentmilesdrivenduringtheyear(dontincludecommutingmiles) & \multicolumn{2}{|c|}{(a)Vehicle1} & \multicolumn{2}{|c|}{(b)Vehicle2} & \multicolumn{2}{|c|}{(c)Vehicle3} & \multicolumn{2}{|c|}{(d)Vehicle4} & \multicolumn{2}{|c|}{(e)Vehicle5} & \multicolumn{2}{|c|}{(f)Vehicle6} \\ \hline 31 & Total commuting miles driven during the year & & & & & & & & & & & & \\ \hline 32 & Totalotherpersonal(noncommuting)milesdriven & & & & & & & & & & & & \\ \hline 33 & Totalmilesdrivenduringtheyear.Addlines30through32 & & & & & & & & & & & & \\ \hline 34 & Was the vehicle available for personal & Yes & No & Yes & No & Yes & No & Yes & No & Yes & No & Yes & No \\ \hline & use during off-duty hours? & & & & & & & & & & & & \\ \hline 35 & Wasthevehicleusedprimarilybyamorethan5%ownerorrelatedperson? & & & & & & & & & & & & \\ \hline 36 & Is another vehicle available for personal use? & & & & & & & & & & & & \\ \hline \end{tabular} Section C-Questions for Employers Who Provide Vehicles for Use by Their Employees Answer these questions to determine if you meet an exception to completing Section B for vehicles used by employees who aren't more than 5% owners or related persons. See instructions. \begin{tabular}{ll|l|l} \hline 37 Do you maintain a written policy statement that prohibits all personal use of vehicles, including commuting, by & Yes & No \end{tabular} your employees? 38 Do you maintain a written policy statement that prohibits personal use of vehicles, except commuting, by your employees? See the instructions for vehicles used by corporate officers, directors, or 1% or more owners 39 Do you treat all use of vehicles by employees as personal use? 40 Do you provide more than five vehicles to your employees, obtain information from your employees about the use of the vehicles, and retain the information received? 41 Do you meet the requirements concerning qualified automobile demonstration use? See instructions Note: If your answer to 37,38,39,40, or 41 is "Yes," don't complete Section B for the covered vehicles. Part VI Amortization TABLE 5 Nonresidential Real Property Mid-Month Convention Straight Line-39 Years (for assets placed in service on or after May 13, 1993) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline \multicolumn{13}{|c|}{ Month Property Placed in Service } \\ \hline & Month 1 & Month 2 & Month 3 & Month 4 & Month 5 & Month 6 & Month 7 & Month 8 & Month 9 & Month 10 & Month 11 & Month 12 \\ \hline Year 1 & 2.461% & 2.247% & 2.033% & 1.819% & 1.605% & 1.391% & 1.177% & 0.963% & 0.749% & 0.535% & 0.321% & 0.107% \\ \hline Year 2-39 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 \\ \hline Year 40 & 0.107 & 0.321 & 0.535 & 0.749 & 0.963 & 1.177 & 1.391 & 1.605 & 1.819 & 2.033 & 2.247 & 2.461 \\ \hline \end{tabular} Required information [The following information applies to the questions displayed below.] Karane Enterprises, a calendar-year manufacturer based in College Station, Texas, began business in 2022. In the process of setting up the business, Karane has acquired various types of assets. Below is a list of assets acquired during 2022 : Not considered a luxury automobile. During 2022, Karane was very successful (and had no $179 limitations) and decided to acquire more assets in 2023 to increase its production capacity. These are the assets acquired during 2023: *Used 100% for business purposes. Karane generated taxable income in 2023 of $1,740,000 for purposes of computing the $179 expense limitation. (Use MACRS Table 1, Table 2, Table 3, Table 4, Table 5, and 1 Note: Leave no answer blank. Enter zero if applicable. Input all the values as positive numbers. TABLE 4 Nonresidential Real Property Mid-Month Convention Straight Line-31.5 Years (for assets placed in service before May 13, 1993) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline \multicolumn{13}{|c|}{ Month Property Placed in Service } \\ \hline & Month 1 & Month 2 & Month 3 & Month 4 & Month 5 & Month 6 & Month 7 & Month 8 & Month 9 & Month 10 & Month 11 & Month 12 \\ \hline Year 1 & 3.042% & 2.778% & 2.513% & 2.249% & 1.984% & 1.720% & 1.455% & 1.190% & 0.926% & 0.661% & 0.397% & 0.132% \\ \hline Year 2-7 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 \\ \hline Year 8 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 \\ \hline Year 9 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 10 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 11 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 12 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 13 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 14 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 15 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 16 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 17 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 19 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 20 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 21 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 22 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 23 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.115 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 24 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 25 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 26 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 27 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 28 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 29 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 30 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline \end{tabular} c. Compute the maximum 2023 depreciation deductions, including $179 expense, but now assume that Karane would like to take bonus depreciation. Note: Round your final answers to nearest whole dollar. b. Compute the maximum 2023 depreciation deductions, including $179 expense (ignoring bonus depreciation). Note: Round your final answers to nearest whole dollar. TABLE 2c MACRS Mid-Quarter Convention: For property placed in service during the third quarter Compute the maximum 2022 depreciation deductions, including $179 expense (ignoring bonus depreciation). Note: Round your final answers to nearest whole dollar. Table 1 MACRS Half-Year Convention TABLE 2c MACRS Mid-Quarter Convention: For property placed in service during the third quarter \begin{tabular}{|c|c|c|} \hline \multicolumn{3}{|c|}{ Depreciation Rate for Recovery Period } \\ \hline & 5-Year & 7-Year \\ \hline Year 1 & 15.00% & 10.71% \\ \hline Year 2 & 34.00 & 25.51 \\ \hline Year 3 & 20.40 & 18.22 \\ \hline Year 4 & 12.24 & 13.02 \\ \hline Year 5 & 11.30 & 9.30 \\ \hline Year 6 & 7.06 & 8.85 \\ \hline Year 7 & & 8.86 \\ \hline Year 8 & & 5.53 \\ \hline \end{tabular} TABLE 2d MACRS-Mid Quarter Convention: For property placed in service during the fourth quarter \begin{tabular}{|c|c|c|} \hline \multicolumn{3}{|c|}{ Depreciation Rate for Recovery Period } \\ \hline & 5-Year & 7-Year \\ \hline Year 1 & 5.00% & 3.57% \\ \hline Year 2 & 38.00 & 27.55 \\ \hline Year 3 & 22.80 & 19.68 \\ \hline Year 4 & 13.68 & 14.06 \\ \hline Year 5 & 10.94 & 10.04 \\ \hline Year 6 & 9.58 & 8.73 \\ \hline Year 7 & & 8.73 \\ \hline Year 8 & & 7.64 \\ \hline \end{tabular} Assume that Karane takes the maximum section 179 expense for the Assembly Equipment. TABLE 3 Residential Rental Property Mid-Month Convention Straight Line-27.5 Years d. Now assume that during 2023 , Karane decides to buy a competitor's assets for a purchase price of $1,385,940. Compute the maximum 2023 cost recovery, including $179 expense and bonus depreciation. Karane purchased the following assets for the lumpsum purchase price: Note: Round your final answers to the nearest whole dollar amount. \begin{tabular}{|c|c|c|c|c|c|c|c|c|} \hline \multirow{2}{*}{\begin{tabular}{l|} Form 4562 \\ Department of the Treasury \\ Internal Revenue Service \end{tabular}} & \multirow{2}{*}{\multicolumn{6}{|c|}{DepreciationandAmortization(IncludingInformationonListedProperty)Attachtoyourtaxreturn.Gotowww.irs.gov/Form4562forinstructionsandthelatestinformation.}} & \multicolumn{2}{|r|}{ OMB No. 1545-0172 } \\ \hline & & & & & & & \multicolumn{2}{|c|}{\begin{tabular}{|c|c|c|} 2(0)22 \\ Attachment \\ Sequence No. 179 \end{tabular}} \\ \hline \multicolumn{3}{|l|}{ Name(s) shown on return } & \multicolumn{4}{|c|}{ Business or activity to which this form relates } & \multicolumn{2}{|c|}{ Identifying number } \\ \hline \multicolumn{9}{|c|}{PartIElectionToExpenseCertainPropertyUnderSection179Note:Ifyouhaveanylistedproperty,completePartVbeforeyoucompletePartI.} \\ \hline & 1 & \\ \hline & & & & & & & 2 & \\ \hline & & & & & & & 3 & \\ \hline & & & & & & & 4 & \\ \hline & & & & & & & 5 & \\ \hline \multicolumn{4}{|c|}{ (a) Description of property } & \multicolumn{2}{|c|}{ (b) Cost (business use only) } & (c) Elected cost & & \\ \hline \multicolumn{8}{|c|}{7 Listed property. Enter the amount from line 29} & \\ \hline \multirow{6}{*}{\multicolumn{7}{|c|}{89101112Totalelectedcostofsection179property.Addamountsincolumn(c),lines6and7Tentativededuction.Enterthesmallerofline5orline8Carryoverofdisalloweddeductionfromline13ofyour2021Form4562.Businessincomelimitation.Enterthesmallerofbusinessincome(notlessthanzero)orline5.SeeinstructionsSection179expensededuction.Addlines9and10,butdontentermorethanline11}} & 8 & \\ \hline & & & & & & & 9 & \\ \hline & & & & & & & 10 & \\ \hline & & & & & & & 11 & \\ \hline & & & & & & & 12 & \\ \hline & & & & & & & & \\ \hline \multicolumn{9}{|c|}{ Note: Don't use Part II or Part III below for listed property. Instead, use Part V. } \\ \hline \multicolumn{9}{|c|}{ Part II Special Depreciation Allowance and Other Depreciation (Don't include listed property. See instructions.) } \\ \hline \multirow{4}{*}{\multicolumn{7}{|c|}{14Specialdepreciationallowanceforqualifiedproperty(otherthanlistedproperty)duringthetaxyear.Seeinstructions.15Propertysubecttosection168(f)(1)election.16Otherdepreciation(includingACRS)}} & 14 & \\ \hline & & & & & & & 15 & \\ \hline & & & & & & & 16 & \\ \hline & & & & \multicolumn{5}{|c|}{ Part III MACRS Depreciation (Don't include listed property. See instructions.) } \\ \hline \multicolumn{9}{|c|}{ Section A} \\ \hline 17 MACRS deductions & for assets pla & ced in service & in taxy & ears beginnin & ng before 2022 & & 17 & \\ \hline 18Ifyouareelectingassetaccounts,ch & togroupanyaeckhere.. & assets placed & in servi & ice during the & tax year into & one or more general & & \\ \hline Section B & -Assets Plac & ed in Service & During & g 2022TaxYe & ear Using the & General Depreciation & n Syste & \\ \hline (a) Classification of property & (b)Monthandyearplacedinservice & \begin{tabular}{|l|l} (c) Basis for dep \\ (businesslivivestry \\ only-see instru \end{tabular} & reciationnenttusections) & \begin{tabular}{|c|} (d) Recovery \\ period \end{tabular} & (e) Convention & (f) Method & (g) De & epreciation deduction \\ \hline 19a 3 -year property & & & & & & & & \\ \hline b 5-year property & & & & & & & & \\ \hline c 7-year property & & & & & & & & \\ \hline d 10-year property & & & & & & & & \\ \hline e 15-year property & & & & & & & & \\ \hline f 20-year property & & & & & & & & \\ \hline g 25-year property & & & & 25 yrs. & & S/L & & \\ \hline h Residential rental & & & & 27.5yrs. & MM & S/L & & \\ \hline property & & & & 27.5yrs. & MM & S/L & & \\ \hline i Nonresidential real & & & & 39yrs. & MM & S/L & & \\ \hline property & & & & & MM & S/L & & \\ \hline Section C- & -Assets Place & d in Service & During 2 & 2022 Tax Yea & ar Using the A & Alternative Depreciatic & on Sys & stem \\ \hline 20a Class life & & & & & & S/L & & \\ \hline b 12-year & & & & 12yrs. & & S/L & & \\ \hline c 30-year & & & & 30 yrs. & MM & S/L & & \\ \hline d 40-year & & & & 40yrs. & MM & S/L & & \\ \hline Part IV Summary & See instructio & ns.) & & & & & & \\ \hline 21 Listed property. En & ter amount fron & m line 28 & & . & . & . . & 21 & \\ \hline 22Total.Addamounhereandontheap & tsfromline12,propriatelines & lines14throuofyourreturn. & ugh17,Partner & lines19andrshipsandS & 20incolumncorporations- & (g),andline21.Enter-seeinstructions & 22 & \\ \hline 23Forassetsshownaportionofthebasis & boveandplacattributableto & edinservicesection263A & duringthcosts. & he current ye & ar, enter the & 23 & & \\ \hline \end{tabular} Form 4562 (2022) Page 2 Include automobiles, certain other vehicles, certain aircraft, and property used for entertainment, recreation, or amusement.) Note: For any vehicle for which you are using the standard mileage rate or deducting lease expense, complete only 24a, 24b, columns (a) through (c) of Section A, all of Section B, and Section C if applicable. Section A-Depreciation and Other Information (Caution: See the instructions for limits for passenger automobiles.) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|} \hline 24a Do you have e & evidence to su & upport the bu & Isiness/investment u & se claimed? & No & 24b If & Yes," i & he evidence w & en? & Yes \\ \hline (a)Typeofproperty(listvehiclesfirst) & \begin{tabular}{|c|} (b) \\ Date placed \\ in service \end{tabular} & \begin{tabular}{|c|} (c) \\ Business/ \\ investment use \\ percentage \\ \end{tabular} & (d)Costorotherbasis & \begin{tabular}{|c|} (e) \\ Basisfordepreciation(business/investmentuseonly) \\ \end{tabular} & (f)Recoveryperiod & MetConv & & (h)Depreciationdeduction & & (i)ectedsection179cost \\ \hline 5 & & & & & & & 25 & & & \\ \hline \end{tabular} 26 Property used more than 50% in a qualified business use: 27 Property used 50% or less in a qualified business use: Complete this section for vehicles used by a sole proprietor, partner, or other "more than 5% owner," or related person. If you provided vehicles to your employees, first answer the questions in Section C to see if you meet an exception to completing this section for those vehicles. \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline 30 & Totalbusiness/investmentmilesdrivenduringtheyear(dontincludecommutingmiles) & \multicolumn{2}{|c|}{(a)Vehicle1} & \multicolumn{2}{|c|}{(b)Vehicle2} & \multicolumn{2}{|c|}{(c)Vehicle3} & \multicolumn{2}{|c|}{(d)Vehicle4} & \multicolumn{2}{|c|}{(e)Vehicle5} & \multicolumn{2}{|c|}{(f)Vehicle6} \\ \hline 31 & Total commuting miles driven during the year & & & & & & & & & & & & \\ \hline 32 & Totalotherpersonal(noncommuting)milesdriven & & & & & & & & & & & & \\ \hline 33 & Totalmilesdrivenduringtheyear.Addlines30through32 & & & & & & & & & & & & \\ \hline 34 & Was the vehicle available for personal & Yes & No & Yes & No & Yes & No & Yes & No & Yes & No & Yes & No \\ \hline & use during off-duty hours? & & & & & & & & & & & & \\ \hline 35 & Wasthevehicleusedprimarilybyamorethan5%ownerorrelatedperson? & & & & & & & & & & & & \\ \hline 36 & Is another vehicle available for personal use? & & & & & & & & & & & & \\ \hline \end{tabular} Section C-Questions for Employers Who Provide Vehicles for Use by Their Employees Answer these questions to determine if you meet an exception to completing Section B for vehicles used by employees who aren't more than 5% owners or related persons. See instructions. \begin{tabular}{ll|l|l} \hline 37 Do you maintain a written policy statement that prohibits all personal use of vehicles, including commuting, by & Yes & No \end{tabular} your employees? 38 Do you maintain a written policy statement that prohibits personal use of vehicles, except commuting, by your employees? See the instructions for vehicles used by corporate officers, directors, or 1% or more owners 39 Do you treat all use of vehicles by employees as personal use? 40 Do you provide more than five vehicles to your employees, obtain information from your employees about the use of the vehicles, and retain the information received? 41 Do you meet the requirements concerning qualified automobile demonstration use? See instructions Note: If your answer to 37,38,39,40, or 41 is "Yes," don't complete Section B for the covered vehicles. Part VI Amortization TABLE 5 Nonresidential Real Property Mid-Month Convention Straight Line-39 Years (for assets placed in service on or after May 13, 1993) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline \multicolumn{13}{|c|}{ Month Property Placed in Service } \\ \hline & Month 1 & Month 2 & Month 3 & Month 4 & Month 5 & Month 6 & Month 7 & Month 8 & Month 9 & Month 10 & Month 11 & Month 12 \\ \hline Year 1 & 2.461% & 2.247% & 2.033% & 1.819% & 1.605% & 1.391% & 1.177% & 0.963% & 0.749% & 0.535% & 0.321% & 0.107% \\ \hline Year 2-39 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 \\ \hline Year 40 & 0.107 & 0.321 & 0.535 & 0.749 & 0.963 & 1.177 & 1.391 & 1.605 & 1.819 & 2.033 & 2.247 & 2.461 \\ \hline \end{tabular} Required information [The following information applies to the questions displayed below.] Karane Enterprises, a calendar-year manufacturer based in College Station, Texas, began business in 2022. In the process of setting up the business, Karane has acquired various types of assets. Below is a list of assets acquired during 2022 : Not considered a luxury automobile. During 2022, Karane was very successful (and had no $179 limitations) and decided to acquire more assets in 2023 to increase its production capacity. These are the assets acquired during 2023: *Used 100% for business purposes. Karane generated taxable income in 2023 of $1,740,000 for purposes of computing the $179 expense limitation. (Use MACRS Table 1, Table 2, Table 3, Table 4, Table 5, and 1 Note: Leave no answer blank. Enter zero if applicable. Input all the values as positive numbers. TABLE 4 Nonresidential Real Property Mid-Month Convention Straight Line-31.5 Years (for assets placed in service before May 13, 1993) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline \multicolumn{13}{|c|}{ Month Property Placed in Service } \\ \hline & Month 1 & Month 2 & Month 3 & Month 4 & Month 5 & Month 6 & Month 7 & Month 8 & Month 9 & Month 10 & Month 11 & Month 12 \\ \hline Year 1 & 3.042% & 2.778% & 2.513% & 2.249% & 1.984% & 1.720% & 1.455% & 1.190% & 0.926% & 0.661% & 0.397% & 0.132% \\ \hline Year 2-7 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 \\ \hline Year 8 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 \\ \hline Year 9 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 10 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 11 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 12 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 13 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 14 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 15 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 16 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 17 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 19 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 20 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 21 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 22 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 23 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.115 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 24 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 25 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 26 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 27 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 28 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 29 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 30 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline \end{tabular} c. Compute the maximum 2023 depreciation deductions, including $179 expense, but now assume that Karane would like to take bonus depreciation. Note: Round your final answers to nearest whole dollar

b. Compute the maximum 2023 depreciation deductions, including $179 expense (ignoring bonus depreciation). Note: Round your final answers to nearest whole dollar. TABLE 2c MACRS Mid-Quarter Convention: For property placed in service during the third quarter Compute the maximum 2022 depreciation deductions, including $179 expense (ignoring bonus depreciation). Note: Round your final answers to nearest whole dollar. Table 1 MACRS Half-Year Convention TABLE 2c MACRS Mid-Quarter Convention: For property placed in service during the third quarter \begin{tabular}{|c|c|c|} \hline \multicolumn{3}{|c|}{ Depreciation Rate for Recovery Period } \\ \hline & 5-Year & 7-Year \\ \hline Year 1 & 15.00% & 10.71% \\ \hline Year 2 & 34.00 & 25.51 \\ \hline Year 3 & 20.40 & 18.22 \\ \hline Year 4 & 12.24 & 13.02 \\ \hline Year 5 & 11.30 & 9.30 \\ \hline Year 6 & 7.06 & 8.85 \\ \hline Year 7 & & 8.86 \\ \hline Year 8 & & 5.53 \\ \hline \end{tabular} TABLE 2d MACRS-Mid Quarter Convention: For property placed in service during the fourth quarter \begin{tabular}{|c|c|c|} \hline \multicolumn{3}{|c|}{ Depreciation Rate for Recovery Period } \\ \hline & 5-Year & 7-Year \\ \hline Year 1 & 5.00% & 3.57% \\ \hline Year 2 & 38.00 & 27.55 \\ \hline Year 3 & 22.80 & 19.68 \\ \hline Year 4 & 13.68 & 14.06 \\ \hline Year 5 & 10.94 & 10.04 \\ \hline Year 6 & 9.58 & 8.73 \\ \hline Year 7 & & 8.73 \\ \hline Year 8 & & 7.64 \\ \hline \end{tabular} Assume that Karane takes the maximum section 179 expense for the Assembly Equipment. TABLE 3 Residential Rental Property Mid-Month Convention Straight Line-27.5 Years d. Now assume that during 2023 , Karane decides to buy a competitor's assets for a purchase price of $1,385,940. Compute the maximum 2023 cost recovery, including $179 expense and bonus depreciation. Karane purchased the following assets for the lumpsum purchase price: Note: Round your final answers to the nearest whole dollar amount. \begin{tabular}{|c|c|c|c|c|c|c|c|c|} \hline \multirow{2}{*}{\begin{tabular}{l|} Form 4562 \\ Department of the Treasury \\ Internal Revenue Service \end{tabular}} & \multirow{2}{*}{\multicolumn{6}{|c|}{DepreciationandAmortization(IncludingInformationonListedProperty)Attachtoyourtaxreturn.Gotowww.irs.gov/Form4562forinstructionsandthelatestinformation.}} & \multicolumn{2}{|r|}{ OMB No. 1545-0172 } \\ \hline & & & & & & & \multicolumn{2}{|c|}{\begin{tabular}{|c|c|c|} 2(0)22 \\ Attachment \\ Sequence No. 179 \end{tabular}} \\ \hline \multicolumn{3}{|l|}{ Name(s) shown on return } & \multicolumn{4}{|c|}{ Business or activity to which this form relates } & \multicolumn{2}{|c|}{ Identifying number } \\ \hline \multicolumn{9}{|c|}{PartIElectionToExpenseCertainPropertyUnderSection179Note:Ifyouhaveanylistedproperty,completePartVbeforeyoucompletePartI.} \\ \hline & 1 & \\ \hline & & & & & & & 2 & \\ \hline & & & & & & & 3 & \\ \hline & & & & & & & 4 & \\ \hline & & & & & & & 5 & \\ \hline \multicolumn{4}{|c|}{ (a) Description of property } & \multicolumn{2}{|c|}{ (b) Cost (business use only) } & (c) Elected cost & & \\ \hline \multicolumn{8}{|c|}{7 Listed property. Enter the amount from line 29} & \\ \hline \multirow{6}{*}{\multicolumn{7}{|c|}{89101112Totalelectedcostofsection179property.Addamountsincolumn(c),lines6and7Tentativededuction.Enterthesmallerofline5orline8Carryoverofdisalloweddeductionfromline13ofyour2021Form4562.Businessincomelimitation.Enterthesmallerofbusinessincome(notlessthanzero)orline5.SeeinstructionsSection179expensededuction.Addlines9and10,butdontentermorethanline11}} & 8 & \\ \hline & & & & & & & 9 & \\ \hline & & & & & & & 10 & \\ \hline & & & & & & & 11 & \\ \hline & & & & & & & 12 & \\ \hline & & & & & & & & \\ \hline \multicolumn{9}{|c|}{ Note: Don't use Part II or Part III below for listed property. Instead, use Part V. } \\ \hline \multicolumn{9}{|c|}{ Part II Special Depreciation Allowance and Other Depreciation (Don't include listed property. See instructions.) } \\ \hline \multirow{4}{*}{\multicolumn{7}{|c|}{14Specialdepreciationallowanceforqualifiedproperty(otherthanlistedproperty)duringthetaxyear.Seeinstructions.15Propertysubecttosection168(f)(1)election.16Otherdepreciation(includingACRS)}} & 14 & \\ \hline & & & & & & & 15 & \\ \hline & & & & & & & 16 & \\ \hline & & & & \multicolumn{5}{|c|}{ Part III MACRS Depreciation (Don't include listed property. See instructions.) } \\ \hline \multicolumn{9}{|c|}{ Section A} \\ \hline 17 MACRS deductions & for assets pla & ced in service & in taxy & ears beginnin & ng before 2022 & & 17 & \\ \hline 18Ifyouareelectingassetaccounts,ch & togroupanyaeckhere.. & assets placed & in servi & ice during the & tax year into & one or more general & & \\ \hline Section B & -Assets Plac & ed in Service & During & g 2022TaxYe & ear Using the & General Depreciation & n Syste & \\ \hline (a) Classification of property & (b)Monthandyearplacedinservice & \begin{tabular}{|l|l} (c) Basis for dep \\ (businesslivivestry \\ only-see instru \end{tabular} & reciationnenttusections) & \begin{tabular}{|c|} (d) Recovery \\ period \end{tabular} & (e) Convention & (f) Method & (g) De & epreciation deduction \\ \hline 19a 3 -year property & & & & & & & & \\ \hline b 5-year property & & & & & & & & \\ \hline c 7-year property & & & & & & & & \\ \hline d 10-year property & & & & & & & & \\ \hline e 15-year property & & & & & & & & \\ \hline f 20-year property & & & & & & & & \\ \hline g 25-year property & & & & 25 yrs. & & S/L & & \\ \hline h Residential rental & & & & 27.5yrs. & MM & S/L & & \\ \hline property & & & & 27.5yrs. & MM & S/L & & \\ \hline i Nonresidential real & & & & 39yrs. & MM & S/L & & \\ \hline property & & & & & MM & S/L & & \\ \hline Section C- & -Assets Place & d in Service & During 2 & 2022 Tax Yea & ar Using the A & Alternative Depreciatic & on Sys & stem \\ \hline 20a Class life & & & & & & S/L & & \\ \hline b 12-year & & & & 12yrs. & & S/L & & \\ \hline c 30-year & & & & 30 yrs. & MM & S/L & & \\ \hline d 40-year & & & & 40yrs. & MM & S/L & & \\ \hline Part IV Summary & See instructio & ns.) & & & & & & \\ \hline 21 Listed property. En & ter amount fron & m line 28 & & . & . & . . & 21 & \\ \hline 22Total.Addamounhereandontheap & tsfromline12,propriatelines & lines14throuofyourreturn. & ugh17,Partner & lines19andrshipsandS & 20incolumncorporations- & (g),andline21.Enter-seeinstructions & 22 & \\ \hline 23Forassetsshownaportionofthebasis & boveandplacattributableto & edinservicesection263A & duringthcosts. & he current ye & ar, enter the & 23 & & \\ \hline \end{tabular} Form 4562 (2022) Page 2 Include automobiles, certain other vehicles, certain aircraft, and property used for entertainment, recreation, or amusement.) Note: For any vehicle for which you are using the standard mileage rate or deducting lease expense, complete only 24a, 24b, columns (a) through (c) of Section A, all of Section B, and Section C if applicable. Section A-Depreciation and Other Information (Caution: See the instructions for limits for passenger automobiles.) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|} \hline 24a Do you have e & evidence to su & upport the bu & Isiness/investment u & se claimed? & No & 24b If & Yes," i & he evidence w & en? & Yes \\ \hline (a)Typeofproperty(listvehiclesfirst) & \begin{tabular}{|c|} (b) \\ Date placed \\ in service \end{tabular} & \begin{tabular}{|c|} (c) \\ Business/ \\ investment use \\ percentage \\ \end{tabular} & (d)Costorotherbasis & \begin{tabular}{|c|} (e) \\ Basisfordepreciation(business/investmentuseonly) \\ \end{tabular} & (f)Recoveryperiod & MetConv & & (h)Depreciationdeduction & & (i)ectedsection179cost \\ \hline 5 & & & & & & & 25 & & & \\ \hline \end{tabular} 26 Property used more than 50% in a qualified business use: 27 Property used 50% or less in a qualified business use: Complete this section for vehicles used by a sole proprietor, partner, or other "more than 5% owner," or related person. If you provided vehicles to your employees, first answer the questions in Section C to see if you meet an exception to completing this section for those vehicles. \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline 30 & Totalbusiness/investmentmilesdrivenduringtheyear(dontincludecommutingmiles) & \multicolumn{2}{|c|}{(a)Vehicle1} & \multicolumn{2}{|c|}{(b)Vehicle2} & \multicolumn{2}{|c|}{(c)Vehicle3} & \multicolumn{2}{|c|}{(d)Vehicle4} & \multicolumn{2}{|c|}{(e)Vehicle5} & \multicolumn{2}{|c|}{(f)Vehicle6} \\ \hline 31 & Total commuting miles driven during the year & & & & & & & & & & & & \\ \hline 32 & Totalotherpersonal(noncommuting)milesdriven & & & & & & & & & & & & \\ \hline 33 & Totalmilesdrivenduringtheyear.Addlines30through32 & & & & & & & & & & & & \\ \hline 34 & Was the vehicle available for personal & Yes & No & Yes & No & Yes & No & Yes & No & Yes & No & Yes & No \\ \hline & use during off-duty hours? & & & & & & & & & & & & \\ \hline 35 & Wasthevehicleusedprimarilybyamorethan5%ownerorrelatedperson? & & & & & & & & & & & & \\ \hline 36 & Is another vehicle available for personal use? & & & & & & & & & & & & \\ \hline \end{tabular} Section C-Questions for Employers Who Provide Vehicles for Use by Their Employees Answer these questions to determine if you meet an exception to completing Section B for vehicles used by employees who aren't more than 5% owners or related persons. See instructions. \begin{tabular}{ll|l|l} \hline 37 Do you maintain a written policy statement that prohibits all personal use of vehicles, including commuting, by & Yes & No \end{tabular} your employees? 38 Do you maintain a written policy statement that prohibits personal use of vehicles, except commuting, by your employees? See the instructions for vehicles used by corporate officers, directors, or 1% or more owners 39 Do you treat all use of vehicles by employees as personal use? 40 Do you provide more than five vehicles to your employees, obtain information from your employees about the use of the vehicles, and retain the information received? 41 Do you meet the requirements concerning qualified automobile demonstration use? See instructions Note: If your answer to 37,38,39,40, or 41 is "Yes," don't complete Section B for the covered vehicles. Part VI Amortization TABLE 5 Nonresidential Real Property Mid-Month Convention Straight Line-39 Years (for assets placed in service on or after May 13, 1993) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline \multicolumn{13}{|c|}{ Month Property Placed in Service } \\ \hline & Month 1 & Month 2 & Month 3 & Month 4 & Month 5 & Month 6 & Month 7 & Month 8 & Month 9 & Month 10 & Month 11 & Month 12 \\ \hline Year 1 & 2.461% & 2.247% & 2.033% & 1.819% & 1.605% & 1.391% & 1.177% & 0.963% & 0.749% & 0.535% & 0.321% & 0.107% \\ \hline Year 2-39 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 \\ \hline Year 40 & 0.107 & 0.321 & 0.535 & 0.749 & 0.963 & 1.177 & 1.391 & 1.605 & 1.819 & 2.033 & 2.247 & 2.461 \\ \hline \end{tabular} Required information [The following information applies to the questions displayed below.] Karane Enterprises, a calendar-year manufacturer based in College Station, Texas, began business in 2022. In the process of setting up the business, Karane has acquired various types of assets. Below is a list of assets acquired during 2022 : Not considered a luxury automobile. During 2022, Karane was very successful (and had no $179 limitations) and decided to acquire more assets in 2023 to increase its production capacity. These are the assets acquired during 2023: *Used 100% for business purposes. Karane generated taxable income in 2023 of $1,740,000 for purposes of computing the $179 expense limitation. (Use MACRS Table 1, Table 2, Table 3, Table 4, Table 5, and 1 Note: Leave no answer blank. Enter zero if applicable. Input all the values as positive numbers. TABLE 4 Nonresidential Real Property Mid-Month Convention Straight Line-31.5 Years (for assets placed in service before May 13, 1993) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline \multicolumn{13}{|c|}{ Month Property Placed in Service } \\ \hline & Month 1 & Month 2 & Month 3 & Month 4 & Month 5 & Month 6 & Month 7 & Month 8 & Month 9 & Month 10 & Month 11 & Month 12 \\ \hline Year 1 & 3.042% & 2.778% & 2.513% & 2.249% & 1.984% & 1.720% & 1.455% & 1.190% & 0.926% & 0.661% & 0.397% & 0.132% \\ \hline Year 2-7 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 \\ \hline Year 8 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 \\ \hline Year 9 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 10 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 11 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 12 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 13 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 14 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 15 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 16 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 17 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 19 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 20 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 21 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 22 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 23 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.115 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 24 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 25 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 26 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 27 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 28 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 29 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 30 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline \end{tabular} c. Compute the maximum 2023 depreciation deductions, including $179 expense, but now assume that Karane would like to take bonus depreciation. Note: Round your final answers to nearest whole dollar. b. Compute the maximum 2023 depreciation deductions, including $179 expense (ignoring bonus depreciation). Note: Round your final answers to nearest whole dollar. TABLE 2c MACRS Mid-Quarter Convention: For property placed in service during the third quarter Compute the maximum 2022 depreciation deductions, including $179 expense (ignoring bonus depreciation). Note: Round your final answers to nearest whole dollar. Table 1 MACRS Half-Year Convention TABLE 2c MACRS Mid-Quarter Convention: For property placed in service during the third quarter \begin{tabular}{|c|c|c|} \hline \multicolumn{3}{|c|}{ Depreciation Rate for Recovery Period } \\ \hline & 5-Year & 7-Year \\ \hline Year 1 & 15.00% & 10.71% \\ \hline Year 2 & 34.00 & 25.51 \\ \hline Year 3 & 20.40 & 18.22 \\ \hline Year 4 & 12.24 & 13.02 \\ \hline Year 5 & 11.30 & 9.30 \\ \hline Year 6 & 7.06 & 8.85 \\ \hline Year 7 & & 8.86 \\ \hline Year 8 & & 5.53 \\ \hline \end{tabular} TABLE 2d MACRS-Mid Quarter Convention: For property placed in service during the fourth quarter \begin{tabular}{|c|c|c|} \hline \multicolumn{3}{|c|}{ Depreciation Rate for Recovery Period } \\ \hline & 5-Year & 7-Year \\ \hline Year 1 & 5.00% & 3.57% \\ \hline Year 2 & 38.00 & 27.55 \\ \hline Year 3 & 22.80 & 19.68 \\ \hline Year 4 & 13.68 & 14.06 \\ \hline Year 5 & 10.94 & 10.04 \\ \hline Year 6 & 9.58 & 8.73 \\ \hline Year 7 & & 8.73 \\ \hline Year 8 & & 7.64 \\ \hline \end{tabular} Assume that Karane takes the maximum section 179 expense for the Assembly Equipment. TABLE 3 Residential Rental Property Mid-Month Convention Straight Line-27.5 Years d. Now assume that during 2023 , Karane decides to buy a competitor's assets for a purchase price of $1,385,940. Compute the maximum 2023 cost recovery, including $179 expense and bonus depreciation. Karane purchased the following assets for the lumpsum purchase price: Note: Round your final answers to the nearest whole dollar amount. \begin{tabular}{|c|c|c|c|c|c|c|c|c|} \hline \multirow{2}{*}{\begin{tabular}{l|} Form 4562 \\ Department of the Treasury \\ Internal Revenue Service \end{tabular}} & \multirow{2}{*}{\multicolumn{6}{|c|}{DepreciationandAmortization(IncludingInformationonListedProperty)Attachtoyourtaxreturn.Gotowww.irs.gov/Form4562forinstructionsandthelatestinformation.}} & \multicolumn{2}{|r|}{ OMB No. 1545-0172 } \\ \hline & & & & & & & \multicolumn{2}{|c|}{\begin{tabular}{|c|c|c|} 2(0)22 \\ Attachment \\ Sequence No. 179 \end{tabular}} \\ \hline \multicolumn{3}{|l|}{ Name(s) shown on return } & \multicolumn{4}{|c|}{ Business or activity to which this form relates } & \multicolumn{2}{|c|}{ Identifying number } \\ \hline \multicolumn{9}{|c|}{PartIElectionToExpenseCertainPropertyUnderSection179Note:Ifyouhaveanylistedproperty,completePartVbeforeyoucompletePartI.} \\ \hline & 1 & \\ \hline & & & & & & & 2 & \\ \hline & & & & & & & 3 & \\ \hline & & & & & & & 4 & \\ \hline & & & & & & & 5 & \\ \hline \multicolumn{4}{|c|}{ (a) Description of property } & \multicolumn{2}{|c|}{ (b) Cost (business use only) } & (c) Elected cost & & \\ \hline \multicolumn{8}{|c|}{7 Listed property. Enter the amount from line 29} & \\ \hline \multirow{6}{*}{\multicolumn{7}{|c|}{89101112Totalelectedcostofsection179property.Addamountsincolumn(c),lines6and7Tentativededuction.Enterthesmallerofline5orline8Carryoverofdisalloweddeductionfromline13ofyour2021Form4562.Businessincomelimitation.Enterthesmallerofbusinessincome(notlessthanzero)orline5.SeeinstructionsSection179expensededuction.Addlines9and10,butdontentermorethanline11}} & 8 & \\ \hline & & & & & & & 9 & \\ \hline & & & & & & & 10 & \\ \hline & & & & & & & 11 & \\ \hline & & & & & & & 12 & \\ \hline & & & & & & & & \\ \hline \multicolumn{9}{|c|}{ Note: Don't use Part II or Part III below for listed property. Instead, use Part V. } \\ \hline \multicolumn{9}{|c|}{ Part II Special Depreciation Allowance and Other Depreciation (Don't include listed property. See instructions.) } \\ \hline \multirow{4}{*}{\multicolumn{7}{|c|}{14Specialdepreciationallowanceforqualifiedproperty(otherthanlistedproperty)duringthetaxyear.Seeinstructions.15Propertysubecttosection168(f)(1)election.16Otherdepreciation(includingACRS)}} & 14 & \\ \hline & & & & & & & 15 & \\ \hline & & & & & & & 16 & \\ \hline & & & & \multicolumn{5}{|c|}{ Part III MACRS Depreciation (Don't include listed property. See instructions.) } \\ \hline \multicolumn{9}{|c|}{ Section A} \\ \hline 17 MACRS deductions & for assets pla & ced in service & in taxy & ears beginnin & ng before 2022 & & 17 & \\ \hline 18Ifyouareelectingassetaccounts,ch & togroupanyaeckhere.. & assets placed & in servi & ice during the & tax year into & one or more general & & \\ \hline Section B & -Assets Plac & ed in Service & During & g 2022TaxYe & ear Using the & General Depreciation & n Syste & \\ \hline (a) Classification of property & (b)Monthandyearplacedinservice & \begin{tabular}{|l|l} (c) Basis for dep \\ (businesslivivestry \\ only-see instru \end{tabular} & reciationnenttusections) & \begin{tabular}{|c|} (d) Recovery \\ period \end{tabular} & (e) Convention & (f) Method & (g) De & epreciation deduction \\ \hline 19a 3 -year property & & & & & & & & \\ \hline b 5-year property & & & & & & & & \\ \hline c 7-year property & & & & & & & & \\ \hline d 10-year property & & & & & & & & \\ \hline e 15-year property & & & & & & & & \\ \hline f 20-year property & & & & & & & & \\ \hline g 25-year property & & & & 25 yrs. & & S/L & & \\ \hline h Residential rental & & & & 27.5yrs. & MM & S/L & & \\ \hline property & & & & 27.5yrs. & MM & S/L & & \\ \hline i Nonresidential real & & & & 39yrs. & MM & S/L & & \\ \hline property & & & & & MM & S/L & & \\ \hline Section C- & -Assets Place & d in Service & During 2 & 2022 Tax Yea & ar Using the A & Alternative Depreciatic & on Sys & stem \\ \hline 20a Class life & & & & & & S/L & & \\ \hline b 12-year & & & & 12yrs. & & S/L & & \\ \hline c 30-year & & & & 30 yrs. & MM & S/L & & \\ \hline d 40-year & & & & 40yrs. & MM & S/L & & \\ \hline Part IV Summary & See instructio & ns.) & & & & & & \\ \hline 21 Listed property. En & ter amount fron & m line 28 & & . & . & . . & 21 & \\ \hline 22Total.Addamounhereandontheap & tsfromline12,propriatelines & lines14throuofyourreturn. & ugh17,Partner & lines19andrshipsandS & 20incolumncorporations- & (g),andline21.Enter-seeinstructions & 22 & \\ \hline 23Forassetsshownaportionofthebasis & boveandplacattributableto & edinservicesection263A & duringthcosts. & he current ye & ar, enter the & 23 & & \\ \hline \end{tabular} Form 4562 (2022) Page 2 Include automobiles, certain other vehicles, certain aircraft, and property used for entertainment, recreation, or amusement.) Note: For any vehicle for which you are using the standard mileage rate or deducting lease expense, complete only 24a, 24b, columns (a) through (c) of Section A, all of Section B, and Section C if applicable. Section A-Depreciation and Other Information (Caution: See the instructions for limits for passenger automobiles.) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|} \hline 24a Do you have e & evidence to su & upport the bu & Isiness/investment u & se claimed? & No & 24b If & Yes," i & he evidence w & en? & Yes \\ \hline (a)Typeofproperty(listvehiclesfirst) & \begin{tabular}{|c|} (b) \\ Date placed \\ in service \end{tabular} & \begin{tabular}{|c|} (c) \\ Business/ \\ investment use \\ percentage \\ \end{tabular} & (d)Costorotherbasis & \begin{tabular}{|c|} (e) \\ Basisfordepreciation(business/investmentuseonly) \\ \end{tabular} & (f)Recoveryperiod & MetConv & & (h)Depreciationdeduction & & (i)ectedsection179cost \\ \hline 5 & & & & & & & 25 & & & \\ \hline \end{tabular} 26 Property used more than 50% in a qualified business use: 27 Property used 50% or less in a qualified business use: Complete this section for vehicles used by a sole proprietor, partner, or other "more than 5% owner," or related person. If you provided vehicles to your employees, first answer the questions in Section C to see if you meet an exception to completing this section for those vehicles. \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline 30 & Totalbusiness/investmentmilesdrivenduringtheyear(dontincludecommutingmiles) & \multicolumn{2}{|c|}{(a)Vehicle1} & \multicolumn{2}{|c|}{(b)Vehicle2} & \multicolumn{2}{|c|}{(c)Vehicle3} & \multicolumn{2}{|c|}{(d)Vehicle4} & \multicolumn{2}{|c|}{(e)Vehicle5} & \multicolumn{2}{|c|}{(f)Vehicle6} \\ \hline 31 & Total commuting miles driven during the year & & & & & & & & & & & & \\ \hline 32 & Totalotherpersonal(noncommuting)milesdriven & & & & & & & & & & & & \\ \hline 33 & Totalmilesdrivenduringtheyear.Addlines30through32 & & & & & & & & & & & & \\ \hline 34 & Was the vehicle available for personal & Yes & No & Yes & No & Yes & No & Yes & No & Yes & No & Yes & No \\ \hline & use during off-duty hours? & & & & & & & & & & & & \\ \hline 35 & Wasthevehicleusedprimarilybyamorethan5%ownerorrelatedperson? & & & & & & & & & & & & \\ \hline 36 & Is another vehicle available for personal use? & & & & & & & & & & & & \\ \hline \end{tabular} Section C-Questions for Employers Who Provide Vehicles for Use by Their Employees Answer these questions to determine if you meet an exception to completing Section B for vehicles used by employees who aren't more than 5% owners or related persons. See instructions. \begin{tabular}{ll|l|l} \hline 37 Do you maintain a written policy statement that prohibits all personal use of vehicles, including commuting, by & Yes & No \end{tabular} your employees? 38 Do you maintain a written policy statement that prohibits personal use of vehicles, except commuting, by your employees? See the instructions for vehicles used by corporate officers, directors, or 1% or more owners 39 Do you treat all use of vehicles by employees as personal use? 40 Do you provide more than five vehicles to your employees, obtain information from your employees about the use of the vehicles, and retain the information received? 41 Do you meet the requirements concerning qualified automobile demonstration use? See instructions Note: If your answer to 37,38,39,40, or 41 is "Yes," don't complete Section B for the covered vehicles. Part VI Amortization TABLE 5 Nonresidential Real Property Mid-Month Convention Straight Line-39 Years (for assets placed in service on or after May 13, 1993) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline \multicolumn{13}{|c|}{ Month Property Placed in Service } \\ \hline & Month 1 & Month 2 & Month 3 & Month 4 & Month 5 & Month 6 & Month 7 & Month 8 & Month 9 & Month 10 & Month 11 & Month 12 \\ \hline Year 1 & 2.461% & 2.247% & 2.033% & 1.819% & 1.605% & 1.391% & 1.177% & 0.963% & 0.749% & 0.535% & 0.321% & 0.107% \\ \hline Year 2-39 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 & 2.564 \\ \hline Year 40 & 0.107 & 0.321 & 0.535 & 0.749 & 0.963 & 1.177 & 1.391 & 1.605 & 1.819 & 2.033 & 2.247 & 2.461 \\ \hline \end{tabular} Required information [The following information applies to the questions displayed below.] Karane Enterprises, a calendar-year manufacturer based in College Station, Texas, began business in 2022. In the process of setting up the business, Karane has acquired various types of assets. Below is a list of assets acquired during 2022 : Not considered a luxury automobile. During 2022, Karane was very successful (and had no $179 limitations) and decided to acquire more assets in 2023 to increase its production capacity. These are the assets acquired during 2023: *Used 100% for business purposes. Karane generated taxable income in 2023 of $1,740,000 for purposes of computing the $179 expense limitation. (Use MACRS Table 1, Table 2, Table 3, Table 4, Table 5, and 1 Note: Leave no answer blank. Enter zero if applicable. Input all the values as positive numbers. TABLE 4 Nonresidential Real Property Mid-Month Convention Straight Line-31.5 Years (for assets placed in service before May 13, 1993) \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline \multicolumn{13}{|c|}{ Month Property Placed in Service } \\ \hline & Month 1 & Month 2 & Month 3 & Month 4 & Month 5 & Month 6 & Month 7 & Month 8 & Month 9 & Month 10 & Month 11 & Month 12 \\ \hline Year 1 & 3.042% & 2.778% & 2.513% & 2.249% & 1.984% & 1.720% & 1.455% & 1.190% & 0.926% & 0.661% & 0.397% & 0.132% \\ \hline Year 2-7 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 \\ \hline Year 8 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 & 3.175 \\ \hline Year 9 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 10 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 11 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 12 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 13 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 14 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 15 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 16 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 17 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 19 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 20 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 21 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 22 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 23 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.115 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 24 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 25 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 26 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 27 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 28 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline Year 29 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 \\ \hline Year 30 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 & 3.175 & 3.174 \\ \hline \end{tabular} c. Compute the maximum 2023 depreciation deductions, including $179 expense, but now assume that Karane would like to take bonus depreciation. Note: Round your final answers to nearest whole dollar Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Traveling Consultants Guide To Auditing UNIX

Authors: Mark Adams

1st Edition

1105616398, 978-1105616396