Answered step by step

Verified Expert Solution

Question

1 Approved Answer

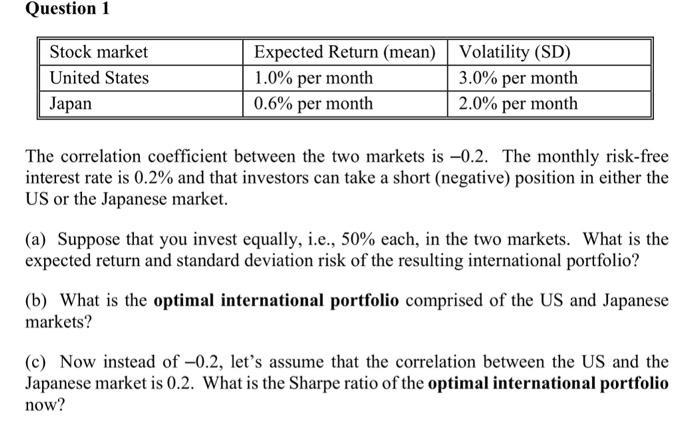

Question 1 Stock market United States Japan Expected Return (mean) 1.0% per month 0.6% per month Volatility (SD) 3.0% per month 2.0% per month

Question 1 Stock market United States Japan Expected Return (mean) 1.0% per month 0.6% per month Volatility (SD) 3.0% per month 2.0% per month The correlation coefficient between the two markets is -0.2. The monthly risk-free interest rate is 0.2% and that investors can take a short (negative) position in either the US or the Japanese market. (a) Suppose that you invest equally, i.e., 50% each, in the two markets. What is the expected return and standard deviation risk of the resulting international portfolio? (b) What is the optimal international portfolio comprised of the US and Japanese markets? (c) Now instead of -0.2, let's assume that the correlation between the US and the Japanese market is 0.2. What is the Sharpe ratio of the optimal international portfolio now?

Step by Step Solution

★★★★★

3.34 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

a The expected return of the international portfolio would ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol S. Eun, Bruce G.Resnick

6th Edition

71316973, 978-0071316972, 78034655, 978-0078034657