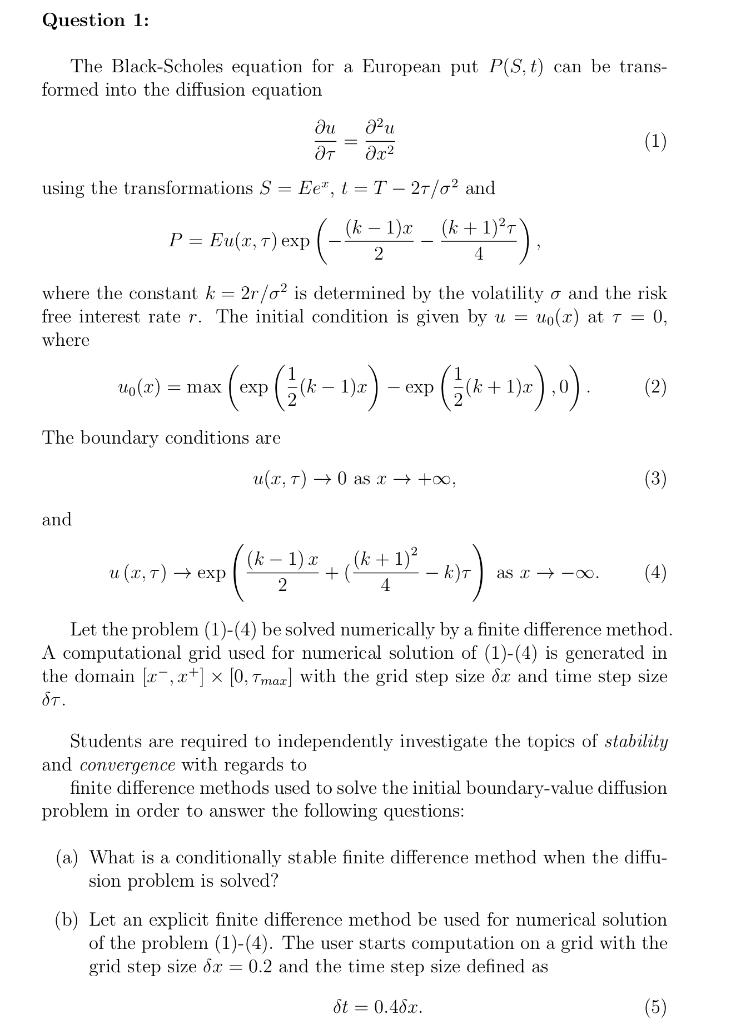

Question 1: The Black-Scholes equation for a European put P(S,t) can be trans- formed into the diffusion equation 22u AT (1) ar2 using the transformations S = Ee, 1 = T - 27/02 and (6 - 1}x_ (8+1787) P = Eur, T) exp k). 2 k + )T 4 where the constant k = 2r/o2 is determined by the volatility o and the risk free interest rater. The initial condition is given by u = uo(r) at T = 0, where volt) = max (exp(fra 1z) - csp ($(x+1)=))) (( x 2, 0 ) (k-).2exp . (2) The boundary conditions are , T) + 0 as r + +, (3) and u (1,7) + exp (471) + (6 + 732-1)=) (k- 2 + (k1) 4 as -. (4) Let the problem (1)-(4) be solved numerically by a finite difference method. A computational grid used for numerical solution of (1)-(4) is generated in the domain (2-,x+] x [0, Tmax] with the grid step size 8x and time step size . Students are required to independently investigate the topics of stability and convergence with regards to finite difference methods used to solve the initial boundary-value diffusion problem in order to answer the following questions: (a) What is a conditionally stable finite difference method when the diffu- sion problem is solved? (b) Let an explicit finite difference method be used for numerical solution of the problem (1)-(4). The user starts computation on a grid with the grid step size 8.r = 0.2 and the time step size defined as St = 0.48x. (5) Question 1: The Black-Scholes equation for a European put P(S,t) can be trans- formed into the diffusion equation 22u AT (1) ar2 using the transformations S = Ee, 1 = T - 27/02 and (6 - 1}x_ (8+1787) P = Eur, T) exp k). 2 k + )T 4 where the constant k = 2r/o2 is determined by the volatility o and the risk free interest rater. The initial condition is given by u = uo(r) at T = 0, where volt) = max (exp(fra 1z) - csp ($(x+1)=))) (( x 2, 0 ) (k-).2exp . (2) The boundary conditions are , T) + 0 as r + +, (3) and u (1,7) + exp (471) + (6 + 732-1)=) (k- 2 + (k1) 4 as -. (4) Let the problem (1)-(4) be solved numerically by a finite difference method. A computational grid used for numerical solution of (1)-(4) is generated in the domain (2-,x+] x [0, Tmax] with the grid step size 8x and time step size . Students are required to independently investigate the topics of stability and convergence with regards to finite difference methods used to solve the initial boundary-value diffusion problem in order to answer the following questions: (a) What is a conditionally stable finite difference method when the diffu- sion problem is solved? (b) Let an explicit finite difference method be used for numerical solution of the problem (1)-(4). The user starts computation on a grid with the grid step size 8.r = 0.2 and the time step size defined as St = 0.48x