Answered step by step

Verified Expert Solution

Question

1 Approved Answer

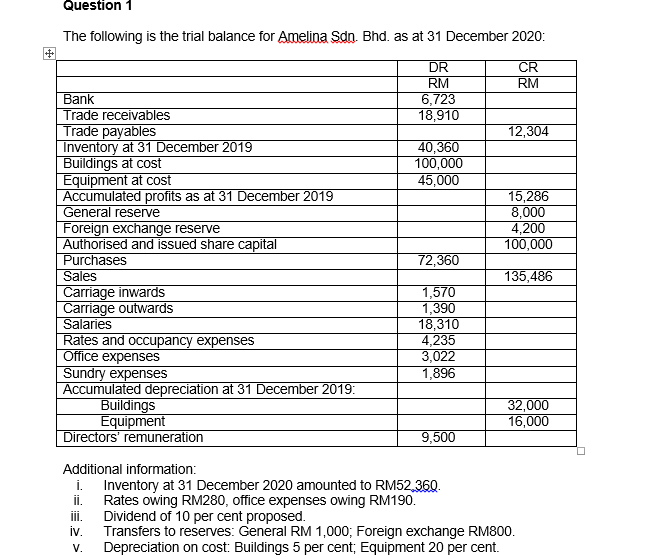

+ Question 1 The following is the trial balance for Amelina Sdn. Bhd. as at 31 December 2020: DR CR RM RM Bank Trade

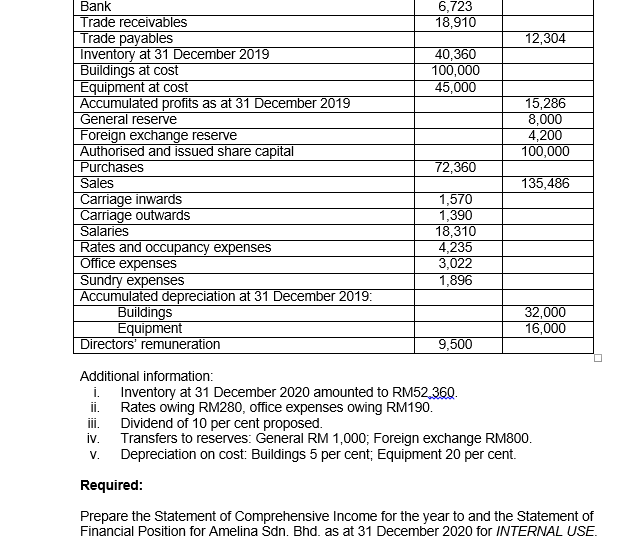

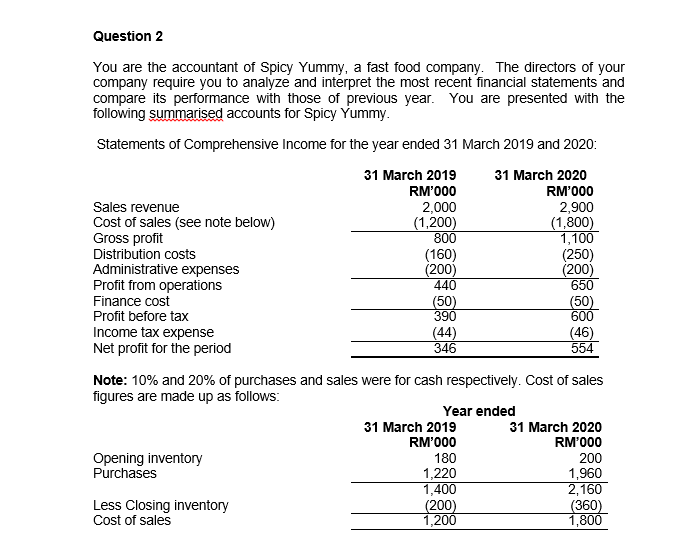

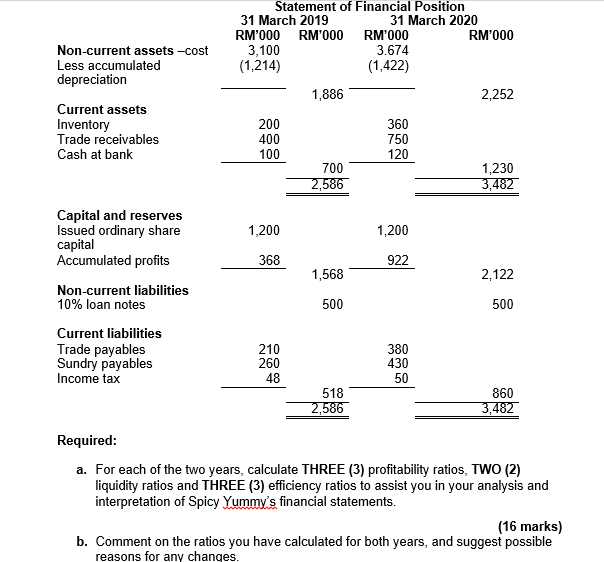

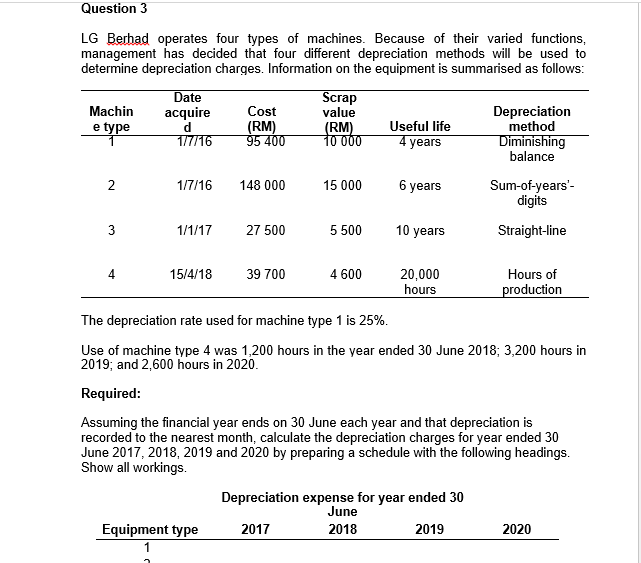

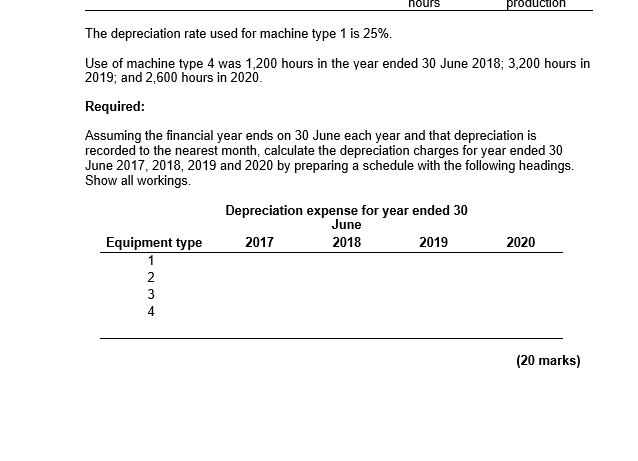

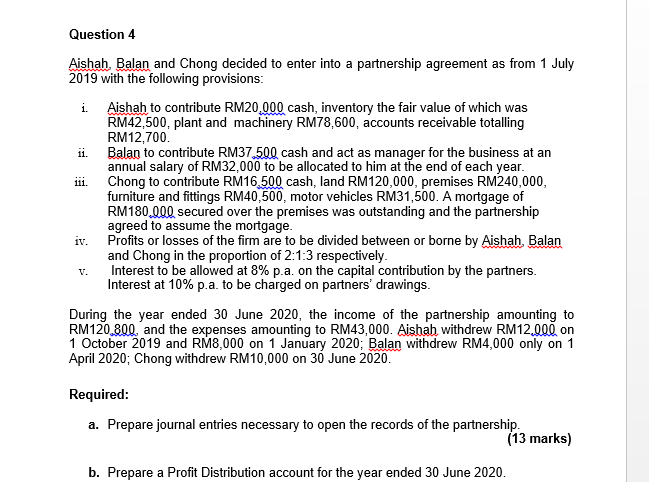

+ Question 1 The following is the trial balance for Amelina Sdn. Bhd. as at 31 December 2020: DR CR RM RM Bank Trade receivables 6,723 18,910 Trade payables 12,304 Inventory at 31 December 2019 40,360 Buildings at cost 100,000 Equipment at cost 45,000 Accumulated profits as at 31 December 2019 15,286 General reserve 8,000 Foreign exchange reserve 4,200 Authorised and issued share capital 100,000 Purchases 72,360 Sales 135,486 Carriage inwards 1,570 Carriage outwards 1,390 Salaries 18,310 Rates and occupancy expenses 4,235 Office expenses 3,022 Sundry expenses 1,896 Accumulated depreciation at 31 December 2019: Buildings 32,000 Equipment 16,000 Directors' remuneration 9,500 i. Inventory at 31 December 2020 amounted to RM52.360. Additional information: II. iii. Rates owing RM280, office expenses owing RM190. Dividend of 10 per cent proposed. iv. V. Transfers to reserves: General RM 1,000; Foreign exchange RM800. Depreciation on cost: Buildings 5 per cent; Equipment 20 per cent. Bank Trade receivables 6,723 18,910 Trade payables 12,304 Inventory at 31 December 2019 40,360 Buildings at cost 100,000 Equipment at cost 45,000 Accumulated profits as at 31 December 2019 15,286 General reserve 8,000 Foreign exchange reserve 4,200 Authorised and issued share capital 100,000 Purchases 72,360 Sales 135,486 Carriage inwards 1,570 Carriage outwards 1,390 Salaries 18,310 Rates and occupancy expenses 4,235 Office expenses 3,022 Sundry expenses 1,896 Accumulated depreciation at 31 December 2019: Buildings 32,000 Equipment 16,000 Directors' remuneration 9,500 Additional information: i. ii. iii. iv. V. Inventory at 31 December 2020 amounted to RM52.360. Rates owing RM280, office expenses owing RM190. Dividend of 10 per cent proposed. Transfers to reserves: General RM 1,000; Foreign exchange RM800. Depreciation on cost: Buildings 5 per cent; Equipment 20 per cent. Required: Prepare the Statement of Comprehensive Income for the year to and the Statement of Financial Position for Amelina Sdn. Bhd. as at 31 December 2020 for INTERNAL USE. Question 2 You are the accountant of Spicy Yummy, a fast food company. The directors of your company require you to analyze and interpret the most recent financial statements and compare its performance with those of previous year. You are presented with the following summarised accounts for Spicy Yummy. Statements of Comprehensive Income for the year ended 31 March 2019 and 2020: Sales revenue Cost of sales (see note below) Gross profit Distribution costs Administrative expenses Profit from operations Finance cost Profit before tax Income tax expense Net profit for the period 31 March 2019 RM'000 31 March 2020 RM'000 2,000 2,900 (1,200) (1,800) 800 1,100 (160) (250) (200) (200) 440 650 (50) (50) 390 600 (44) (46) 346 554 Note: 10% and 20% of purchases and sales were for cash respectively. Cost of sales figures are made up as follows: Opening inventory Purchases Less Closing inventory Cost of sales Year ended 31 March 2019 RM'000 31 March 2020 RM'000 180 200 1,220 1,960 1,400 2,160 (200) (360) 1,200 1,800 RM'000 (1,214) Non-current assets -cost Less accumulated Statement of Financial Position 31 March 2019 RM'000 31 March 2020 RM'000 RM'000 3,100 3.674 (1,422) depreciation 1,886 2,252 Current assets Inventory 200 360 Trade receivables 400 750 Cash at bank 100 120 700 1,230 2,586 3,482 Capital and reserves Issued ordinary share 1,200 1,200 capital Accumulated profits 368 922 1,568 2,122 Non-current liabilities 10% loan notes 500 500 Current liabilities Trade payables Sundry payables Income tax Required: 210 260 380 430 48 50 518 2,586 860 3,482 a. For each of the two years, calculate THREE (3) profitability ratios, TWO (2) liquidity ratios and THREE (3) efficiency ratios to assist you in your analysis and interpretation of Spicy Yummy's financial statements. (16 marks) b. Comment on the ratios you have calculated for both years, and suggest possible reasons for any changes. Question 3 LG Berhad operates four types of machines. Because of their varied functions, management has decided that four different depreciation methods will be used to determine depreciation charges. Information on the equipment is summarised as follows: Machin Date acquire Cost Scrap value Depreciation e type d (RM) 1/7/16 95 400 Useful life 4 years method Diminishing balance 2 1/7/16 148 000 15 000 6 years Sum-of-years'- digits 3 1/1/17 27 500 5 500 10 years Straight-line 4 15/4/18 39 700 4 600 20,000 hours Hours of production The depreciation rate used for machine type 1 is 25%. Use of machine type 4 was 1,200 hours in the year ended 30 June 2018; 3,200 hours in 2019; and 2,600 hours in 2020. Required: Assuming the financial year ends on 30 June each year and that depreciation is recorded to the nearest month, calculate the depreciation charges for year ended 30 June 2017, 2018, 2019 and 2020 by preparing a schedule with the following headings. Show all workings. Depreciation expense for year ended 30 Equipment type 1 2017 June 2018 2019 2020 nours production The depreciation rate used for machine type 1 is 25%. Use of machine type 4 was 1,200 hours in the year ended 30 June 2018; 3,200 hours in 2019; and 2,600 hours in 2020. Required: Assuming the financial year ends on 30 June each year and that depreciation is recorded to the nearest month, calculate the depreciation charges for year ended 30 June 2017, 2018, 2019 and 2020 by preparing a schedule with the following headings. Show all workings. Depreciation expense for year ended 30 Equipment type 2017 1 2 234 June 2018 2019 2020 (20 marks) Question 4 Aishah, Balan and Chong decided to enter into a partnership agreement as from 1 July 2019 with the following provisions: i. Aishah to contribute RM20,000 cash, inventory the fair value of which was RM42,500, plant and machinery RM78,600, accounts receivable totalling RM12,700. ii. 111. iv. V. Balan to contribute RM37,500 cash and act as manager for the business at an annual salary of RM32,000 to be allocated to him at the end of each year. Chong to contribute RM16,500 cash, land RM120,000, premises RM240,000, furniture and fittings RM40,500, motor vehicles RM31,500. A mortgage of RM180,000 secured over the premises was outstanding and the partnership agreed to assume the mortgage. Profits or losses of the firm are to be divided between or borne by Aishah, Balan and Chong in the proportion of 2:1:3 respectively. Interest to be allowed at 8% p.a. on the capital contribution by the partners. Interest at 10% p.a. to be charged on partners' drawings. During the year ended 30 June 2020, the income of the partnership amounting to RM120,800, and the expenses amounting to RM43,000. Aishah withdrew RM12,000 on 1 October 2019 and RM8,000 on 1 January 2020; Balan withdrew RM4,000 only on 1 April 2020; Chong withdrew RM10,000 on 30 June 2020. Required: a. Prepare journal entries necessary to open the records of the partnership. b. Prepare a Profit Distribution account for the year ended 30 June 2020. (13 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial and Managerial Accounting

Authors: Jonathan E. Duchac, James M. Reeve, Carl S. Warren

11th Edition

9780538480901, 9781111525774, 538480890, 538480904, 1111525773, 978-0538480895