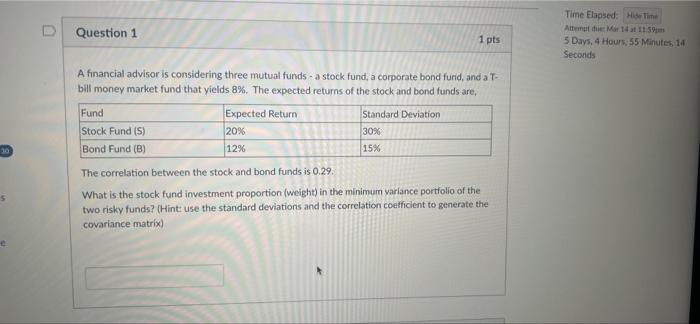

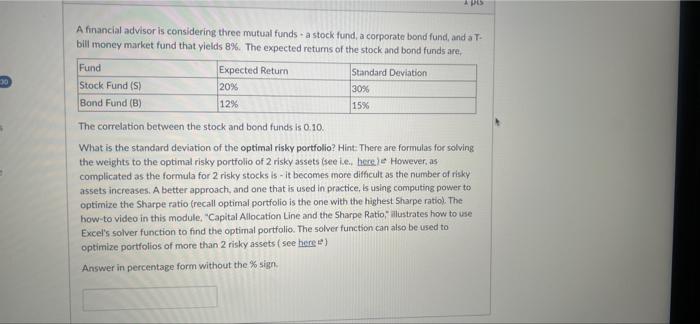

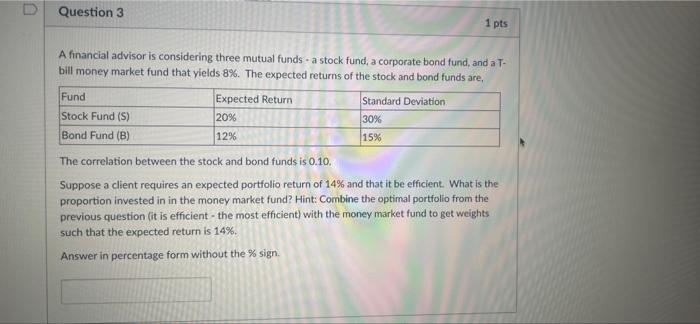

Question 1 Time Elapsed: Hide Time Attemut Mar 14 of 11 59 5 Days, 4 Hours 55 Minutes, 14 Seconds 1 pts A financial advisor is considering three mutual funds - a stock fund, a corporate bond fund, and a T- bill money market fund that yields 8%. The expected returns of the stock and bond funds are, Fund Expected Return Standard Deviation Stock Fund (S) 20% 30% Bond Fund (B) 12% 15% The correlation between the stock and bond funds is 0.29. What is the stock fund investment proportion (weight) in the minimum varlance portfolio of the two risky funds? (Hint use the standard deviations and the correlation coefficient to generate the covariance matrix) 5 e APES A financial advisor is considering three mutual funds - a stock fund, a corporate bond fund, and a bill money market fund that yields 8%. The expected retums of the stock and bond funds are 20% Fund Expected Return Standard Deviation Stock Fund (S) 30% Bond Fund (B) 12% 15% The correlation between the stock and bond funds is 0.10. What is the standard deviation of the optimal risky portfolio? Hint: There are formulas for solving the weights to the optimal risky portfolio of 2 risky assets (seele, beree However, as complicated as the formula for 2 risky stocks is - it becomes more difficult as the number of risky assets increases. A better approach, and one that is used in practice, is using computing power to optimize the Sharpe ratio (recall optimal portfolio is the one with the highest Sharpe ratio). The how to video in this module, "Capital Allocation Line and the Sharpe Ratio, illustrates how to use Excel's solver function to find the optimal portfolio. The solver function can also be used to optimize portfolios of more than 2 risky assets (see here) Answer in percentage form without the sign Question 3 1 pts A financial advisor is considering three mutual funds. a stock fund, a corporate bond fund, and a T- bill money market fund that yields 8%. The expected returns of the stock and bond funds are, Fund Expected Return Standard Deviation Stock Fund (S) 20% 30% Bond Fund (B) 12% 15% The correlation between the stock and bond funds is 0.10 Suppose a client requires an expected portfolio return of 14% and that it be efficient. What is the proportion invested in in the money market fund? Hint: Combine the optimal portfolio from the previous question (it is efficient - the most efficient) with the money market fund to get weights such that the expected return is 14%. Answer in percentage form without the % sign