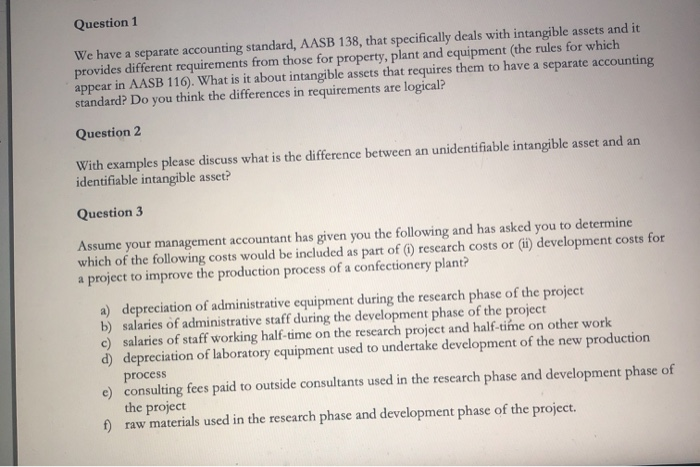

Question 1 We have a separate accounting standard, AASB 138, that specifically deals with intangible assets and it provides different requirements from those for property, plant and equipment (the rules for which appear in AASB 116). What is it about intangible assets that requires them to have a separate accounting standard? Do you think the differences in requirements are logical? Question 2 With examples please discuss what is the difference between an unidentifiable intangible asset and an identifiable intangible asset? Question 3 Assume your management accountant has given you the following and has asked you to determine which of the following costs would be included as part of (1) research costs or (ii) development costs for a project to improve the production process of a confectionery plant? a) depreciation of administrative equipment during the research phase of the project b) salaries of administrative staff during the development phase of the project c) salaries of staff working half-time on the research project and half-time on other work d) depreciation of laboratory equipment used to undertake development of the new production process c) consulting fees paid to outside consultants used in the research phase and development phase of the project f) raw materials used in the research phase and development phase of the project. Question 1 We have a separate accounting standard, AASB 138, that specifically deals with intangible assets and it provides different requirements from those for property, plant and equipment (the rules for which appear in AASB 116). What is it about intangible assets that requires them to have a separate accounting standard? Do you think the differences in requirements are logical? Question 2 With examples please discuss what is the difference between an unidentifiable intangible asset and an identifiable intangible asset? Question 3 Assume your management accountant has given you the following and has asked you to determine which of the following costs would be included as part of (1) research costs or (ii) development costs for a project to improve the production process of a confectionery plant? a) depreciation of administrative equipment during the research phase of the project b) salaries of administrative staff during the development phase of the project c) salaries of staff working half-time on the research project and half-time on other work d) depreciation of laboratory equipment used to undertake development of the new production process c) consulting fees paid to outside consultants used in the research phase and development phase of the project f) raw materials used in the research phase and development phase of the project