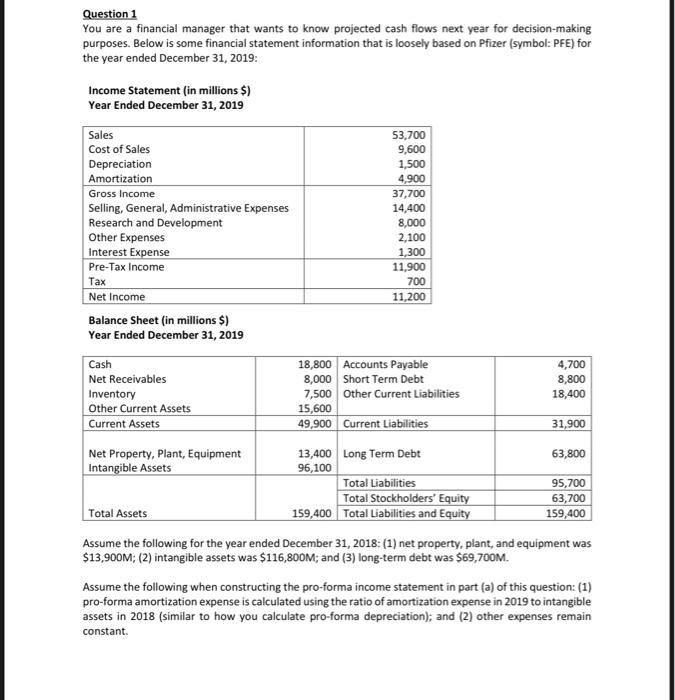

Question 1 You are a financial manager that wants to know projected cash flows next year for decision-making purposes. Below is some financial statement information that is loosely based on Pfizer (symbol: PFE) for the year ended December 31, 2019: Income Statement (in millions $) Year Ended December 31, 2019 Sales Cost of Sales Depreciation Amortization Gross Income Selling, General, Administrative Expenses Research and Development Other Expenses Interest Expense Pre-Tax Income Tax Net Income Balance Sheet (in millions $) Year Ended December 31, 2019 Cash Net Receivables Inventory Other Current Assets Current Assets Net Property, Plant, Equipment Intangible Assets Total Assets 53,700 9,600 1,500 4,900 37,700 14,400 8,000 2,100 1,300 11,900 700 11,200 18,800 Accounts Payable 8,000 Short Term Debt 7,500 Other Current Liabilities 15,600 49,900 Current Liabilities 13,400 Long Term Debt 96,100 Total Liabilities Total Stockholders' Equity Total Liabilities and Equity 4,700 8,800 18,400 31,900 63,800 95,700 63,700 159,400 159,400 Assume the following for the year ended December 31, 2018: (1) net property, plant, and equipment was $13,900M; (2) intangible assets was $116,800M; and (3) long-term debt was $69,700M. Assume the following when constructing the pro-forma income statement in part (a) of this question: (1) pro-forma amortization expense is calculated using the ratio of amortization expense in 2019 to intangible assets in 2018 (similar to how you calculate pro-forma depreciation); and (2) other expenses remain constant.

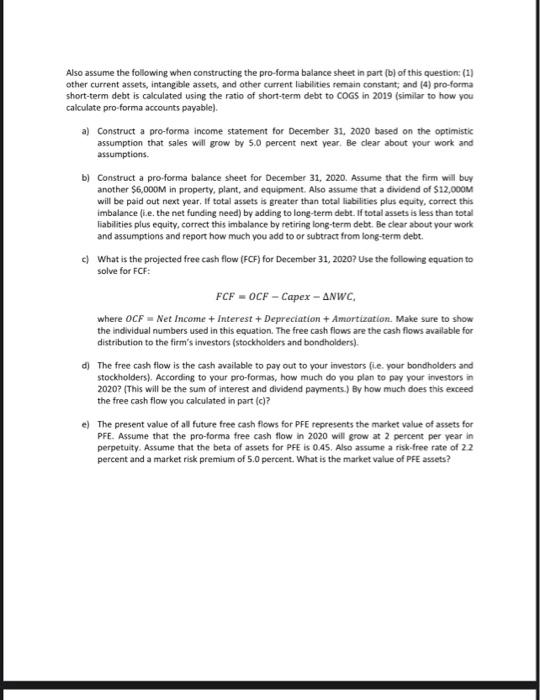

Also assume the following when constructing the pro-forma balance sheet in part (b) of this question: (1) other current assets, intangible assets, and other current liabilities remain constant; and (4) pro-forma short-term debt is calculated using the ratio of short-term debt to COGS in 2019 (similar to how you calculate pro-forma accounts payable). a) Construct a pro-forma income statement for December 31, 2020 based on the optimistic assumption that sales will grow by 5.0 percent next year. Be clear about your work and assumptions. b) Construct a pro-forma balance sheet for December 31, 2020. Assume that the firm will buy another $6,000M in property, plant, and equipment. Also assume that a dividend of $12,000M will be paid out next year, If total assets is greater than total liabilities plus equity, correct this imbalance (i.e. the net funding need) by adding to long-term debt. If total assets is less than total liabilities plus equity, correct this imbalance by retiring long-term debt. Be clear about your work and assumptions and report how much you add to or subtract from long-term debt. c) What is the projected free cash flow (FCF) for December 31, 2020? Use the following equation to solve for FCF: FCF=OCFCapexNWC, where OCF= Net Income + Interest + Depreciation + Amortization. Make sure to show the individual numbers used in this equation. The free cash flows are the cash flows available for distribution to the firm's investors (stockholders and bondholders). d) The free cash flow is the cash available to pay out to your investors fi.e. your bondholders and stockholders). According to your pro-formas, how much do you plan to pay your investors in 2020 ? (This will be the sum of interest and dividend payments.) By how much does this exceed the free cash flow you calculated in part (c)? e) The present value of all future free cash flows for PFE represents the market value of assets for PFE. Assume that the pro-forma free cash flow in 2020 will grow at 2 percent per vear in perpetuity. Assume that the beta of assets for PFE is 0.45 . Also assume a risk-free rate of 2.2 percent and a market risk premium of 5.0 percent. What is the market value of PFE assets? Question 2 Suppose you want to create a "Condor Spread" option strategy based on PFE call options. The condor spread will involve the following: - Buying a call option with strike price $35 - Selling a call option with strike price $40 - Selling a call option with strike price $50 - Buying a call option with strike price \$55 You want all these options to have the same maturity of January 17, 2025. a) Go to Yahool Finance and search for Pfizer (symbol: PFE), then click on the "Options" tab, then select "january 17, 2025" from the dropdown box below the stock price to obtain a list of PFE options with approximately twelve months to expiration. The "Ask" price is the price at which you can buy an option while the "Bid" price is the price at which you can sell an option. Report the bid and ask prices for each of the four call options described above. Also report the date, time, and stock price when you retrieved these options prices. You should collect these data during regular trading hours (9:30am to 4:00pm EST on weekdays), as bid and ask prices are sometimes not available during off-market hours. b) What is the net cost of this condor spread? Remember to use the bid price when you sell a call option, and the ask price when you buy a call option. You receive money when you sell an option and pay money when you buy an option. c) What kind of price movement are we betting on with this strategy? (no calculations needed for this question) Question 3 You are the sole bondholder in a firm that will be liquidated at its market value next year. For example, if the market value of the firm ends up being $70M next year, then the firm will be sold (liquidated) for $70M. Your main concern is that you will not be paid back the $50M you are owed next year, as the market value of the firm next year could end up being less than the $50M that you are owed. a) Provide the payoff diagram for the bondholder with the market value of the firm on the x-axis. The financial manager of the firm is deciding whether she should take on one last risky project before the firm is liquidated next year. If this project is accepted, then the potential liquidation value of the firm could be much higher next year, but it could also be much lower. If the manager does not take on the risky project, we will assume that the manager does nothing instead. b) Suppose that the financial manager decides to do nothing. In this case, the market value of the firm will equal either $60M (state A ) or $40M (state B) next year, with equal probability. It follows that upon liquidation next year, the bondholder with either receive the 550M they are owed (state A) or only $40M (state B). In each state, the stockholder receives whatever is left over after the bondholder is paid off. What is the expected liquidation value of the firm? What is the expected payoff to the bondhoider? What is the expected payoff to the stockholder? c) Suppose that the financial manager accepts the risky project. In this case, the market value of the firm will equal either $90M (state A ) or zero (state B) next year, with equal probability. It follows that upon liquidation next year, the bondholder with either receive the 550M they are owed (state A) or nothing (state B). In each state, the stockholder receives whatever is left over after the bondholder is paid off. What is the expected liquidation value of the firm? What is the expected payoff to the bondholder? What is the expected payoff to the stockholder? d) Assume that the manager wants to maximize the expected payoff to the stockholders. Would she choose to do nothing (as in part (b)) or take on the risky project (as in part (c))? Explain. e) The financial manager decides to take on the risky project from part (c). This is detrimental to the bondholder because there is now a chance that the bondholder will not be repaid any of \$50M he is owed. If you were the bondholder and wanted to completely protect yourself against the state of the world where the firm does not pay you back (so that the option payoff is \$5OM in state B), would you buy a (call or put) option on the final market value of the assets of the firm, and at what strike price? Bondholders can protect themselves from these bankruptcy events by purchasing a "Credit Default Swap," an agreement in which the bondholder pays a third counterparty a fee or a sequence of fees over time; in exchange, the third counterparty repays the bondholder what he is owed in the event that the firm goes bankrupt and cannot repay the bondholder