Answered step by step

Verified Expert Solution

Question

1 Approved Answer

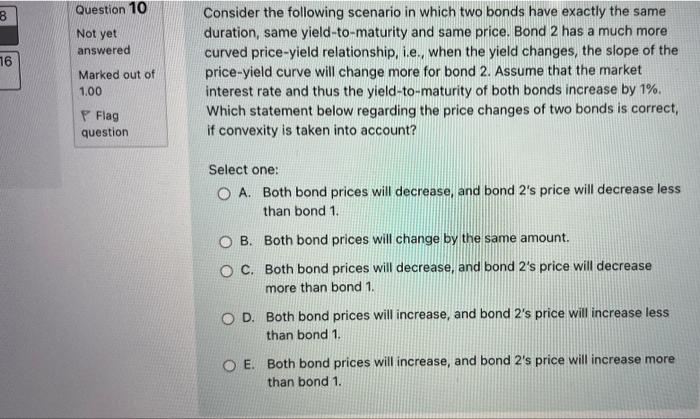

Question 10 8 Not yet answered 76 Marked out of 1.00 Consider the following scenario in which two bonds have exactly the same duration, same

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Comes Alive The Color Accounting Parable

Authors: Mark Robilliard ,Peter Frampton, Chang Chang, Mark Morrow, John Gorman

1st Edition

1450769608, 978-1450769600