Answered step by step

Verified Expert Solution

Question

1 Approved Answer

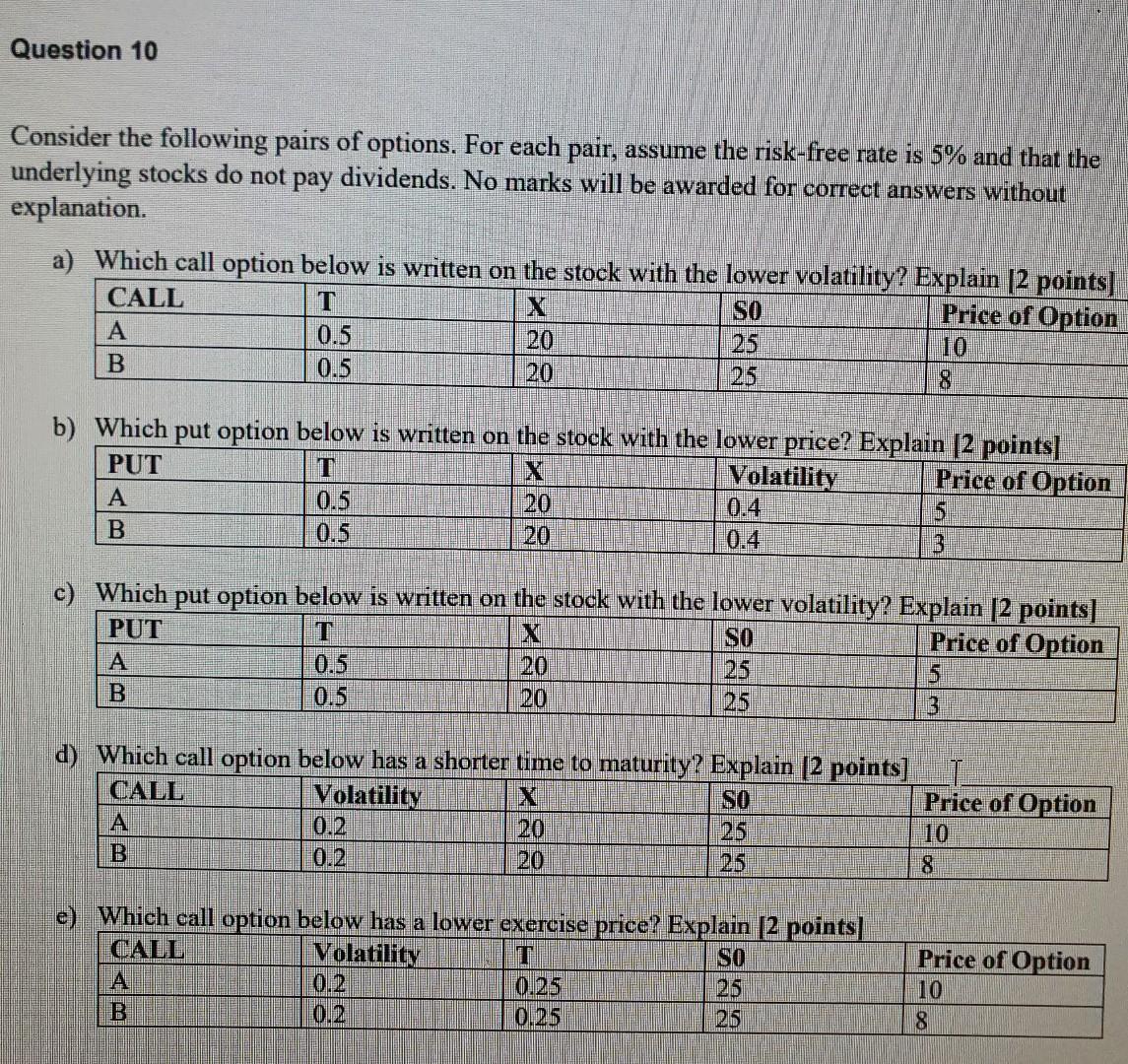

Question 10 Consider the following pairs of options. For each pair, assume the risk-free rate is 5% and that the underlying stocks do not pay

Question 10 Consider the following pairs of options. For each pair, assume the risk-free rate is 5% and that the underlying stocks do not pay dividends. No marks will be awarded for correct answers without explanation. a) Which call option below is written on the stock with the lower volatility? Explain [2 points] CALL X SO Price of Option A 0.5 20 10 B 0.5 20 25 8 b) Which put option below is written on the stock with the lower price? Explain [2 points] PUT T Volatility Price of Option A 0.5 20 0.4 B 0.5 20 3 c) Which put option below is written on the stock with the lower volatility? Explain [2 points] PUT X SO Price of Option A 0.5 5 B 0.5 20 25 3 d) Which call option below has a shorter time to maturity? Explain (2 points] CALL Volatility SO Price of Option A 0.2 20 25 10 B 0.2 20 25 e) Which call option below has a lower exercise price? Explain [2 points) CALL Volatility T SO A 0.2 0.25 25 B 0.2 0.25 26 Price of Option 10 8

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applied International Finance

Authors: Thomas J O'Brien

1st Edition

1606497340, 9781606497340