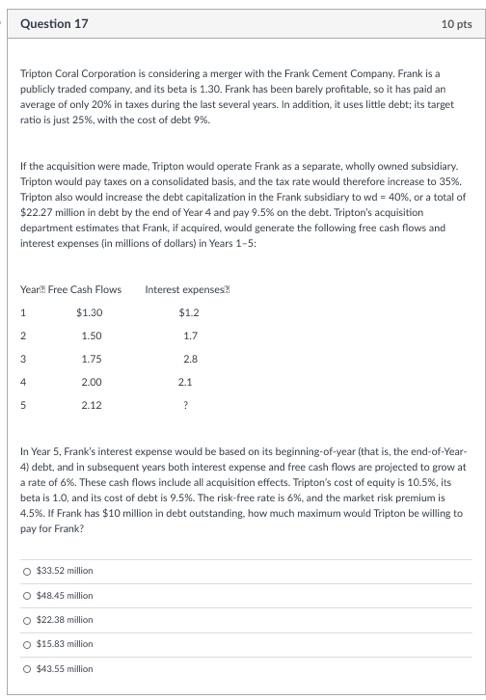

Question 17 10 pts Tripton Coral Corporation is considering a merger with the Frank Cement Company. Frank is a publicly traded company, and its beta is 1.30. Frank has been barely profitable, so it has paid an average of only 20% in taxes during the last several years. In addition, it uses little debt; its target ratio is just 25%, with the cost of debt 9% If the acquisition were made. Tripton would operate Frank as a separate, wholly owned subsidiary. Tripton would pay taxes on a consolidated basis, and the tax rate would therefore increase to 35%. Tripton also would increase the debt capitalization in the Frank subsidiary to wd = 40%, or a total of $22.27 million in debt by the end of Year 4 and pay 9.5% on the debt. Tripton's acquisition department estimates that Frank, if acquired, would generate the following free cash flows and interest expenses (in millions of dollars) in Years 1-5: Year! Free Cash Flows $1.30 Interest expenses? $1.2 1 2 1.50 1.7 1.75 2.8 4 2.00 2.1 5 2.12 ? In Year 5, Frank's interest expense would be based on its beginning-of-year (that is the end-of-Year- 4) debt, and in subsequent years both interest expense and free cash flows are projected to grow at a rate of 6%. These cash flows include all acquisition effects. Tripton's cost of equity is 10.5%, its beta is 1.0, and its cost of debt is 9.5%. The risk-free rate is 6%, and the market risk premium is 4.5%. If Frank has $10 million in debt outstanding, how much maximum would Tripton be willing to pay for Frank? $33.52 million O $48.45 million $22.38 million O $15.83 million O $43.55 million Question 17 10 pts Tripton Coral Corporation is considering a merger with the Frank Cement Company. Frank is a publicly traded company, and its beta is 1.30. Frank has been barely profitable, so it has paid an average of only 20% in taxes during the last several years. In addition, it uses little debt; its target ratio is just 25%, with the cost of debt 9% If the acquisition were made. Tripton would operate Frank as a separate, wholly owned subsidiary. Tripton would pay taxes on a consolidated basis, and the tax rate would therefore increase to 35%. Tripton also would increase the debt capitalization in the Frank subsidiary to wd = 40%, or a total of $22.27 million in debt by the end of Year 4 and pay 9.5% on the debt. Tripton's acquisition department estimates that Frank, if acquired, would generate the following free cash flows and interest expenses (in millions of dollars) in Years 1-5: Year! Free Cash Flows $1.30 Interest expenses? $1.2 1 2 1.50 1.7 1.75 2.8 4 2.00 2.1 5 2.12 ? In Year 5, Frank's interest expense would be based on its beginning-of-year (that is the end-of-Year- 4) debt, and in subsequent years both interest expense and free cash flows are projected to grow at a rate of 6%. These cash flows include all acquisition effects. Tripton's cost of equity is 10.5%, its beta is 1.0, and its cost of debt is 9.5%. The risk-free rate is 6%, and the market risk premium is 4.5%. If Frank has $10 million in debt outstanding, how much maximum would Tripton be willing to pay for Frank? $33.52 million O $48.45 million $22.38 million O $15.83 million O $43.55 million