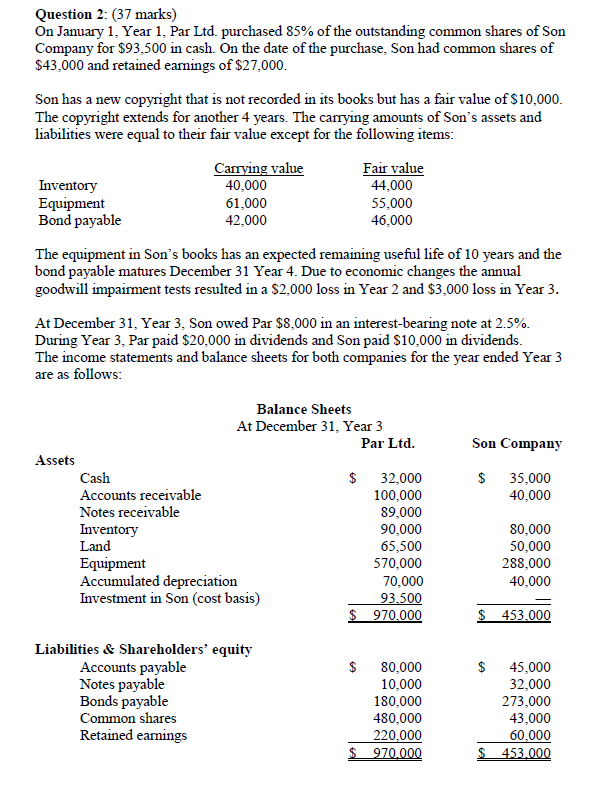

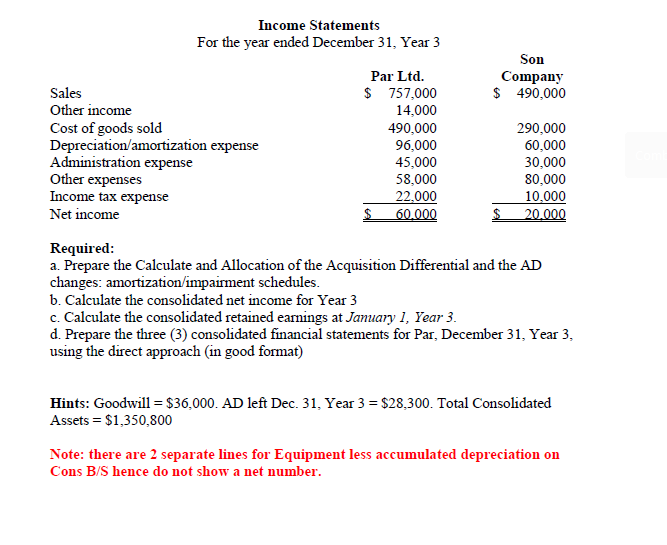

Question 2: (37 marks) On January 1, Year 1, Par Ltd. purchased 85% of the outstanding con Company for $93,500 in cash. On the date of the purchase, Son had common shares of $43,000 and retained eamings of $27,000 common shares of Son Son has a new copyright that is not recorded in its books but has a fair value of S10,000. The copyright extends for another 4 years. The carrying amounts of Son's assets and labilities were equal to their fair value except for the following items: Carrying value 40,000 61,000 42,000 Fair value 44,000 Inventory Equipment Bond payable 55,000 46,000 The equipment in Son's books has an expected remaining useful life of 10 years and the bond payable matures December 31 Year 4. Due to economic changes the annual goodwill impaiment tests resulted in a $2,000 loss in Year 2 and $3,000 loss in Year 3. At December 31, Year 3, Son owed Par $8,000 in an interest-bearing note at 2.5%. During Year 3, Par paid $20,000 in dividends and Son paid s10,000 in dividends. The income statements and balance sheets for both companies for the year ended Year 3 are as follows: Balance Sheets At December 31, Year 3 Par Ltd Son Company Assets $ 32,000 100,000 Cash $ 35,000 Accounts receivable Notes receivable 40,000 89,000 90,000 65,500 570,000 70,000 93.500 970.000 Inventory Land Equipment Accumulated depreciation Investment in Son (cost basis) 80,000 50,000 288,000 40,000 $ 453.000 Liabilities & Shareholders' equity Accounts payable Notes payable Bonds payable Common shares $ 80,000 10,000 $ 45,000 32,000 273,000 43,000 60.000 S 453.000 180,000 480,000 220,000 $ 970.000 Retained earmings Income Statements For the year ended December 31, Year 3 Son Par Ltd $ 757,000 14,000 ompany 490,000 Sales Other income Cost of goods sold Depreciation/amortization expense Administration expense Other expenses Income tax expense 490,000 96,000 45,000 58,000 22,000 $ 290,000 60,000 30,000 80,000 10.000 20.000 Net income 60.000 Required: a. Prepare the Calculate and Allocation of the Acquisition Differential and the AD changes: amortization/impairment schedules. b. Calculate the consolidated net income for Year 3 c. Calculate the consolidated retained eamings at Jamuary 1, Year 3. d. Prepare the three (3) consolidated financial statements for Par, December 31. Year 3, using the direct approach (in good format) Hints: Goodwill $36,000. AD left Dec. 31, Year 3 $28,300. Total Consolidated Assets $1,350,800 Note: there are 2 separate lines for Equipment less accumulated depreciation on Cons B/S hence do not show a net number Question 2: (37 marks) On January 1, Year 1, Par Ltd. purchased 85% of the outstanding con Company for $93,500 in cash. On the date of the purchase, Son had common shares of $43,000 and retained eamings of $27,000 common shares of Son Son has a new copyright that is not recorded in its books but has a fair value of S10,000. The copyright extends for another 4 years. The carrying amounts of Son's assets and labilities were equal to their fair value except for the following items: Carrying value 40,000 61,000 42,000 Fair value 44,000 Inventory Equipment Bond payable 55,000 46,000 The equipment in Son's books has an expected remaining useful life of 10 years and the bond payable matures December 31 Year 4. Due to economic changes the annual goodwill impaiment tests resulted in a $2,000 loss in Year 2 and $3,000 loss in Year 3. At December 31, Year 3, Son owed Par $8,000 in an interest-bearing note at 2.5%. During Year 3, Par paid $20,000 in dividends and Son paid s10,000 in dividends. The income statements and balance sheets for both companies for the year ended Year 3 are as follows: Balance Sheets At December 31, Year 3 Par Ltd Son Company Assets $ 32,000 100,000 Cash $ 35,000 Accounts receivable Notes receivable 40,000 89,000 90,000 65,500 570,000 70,000 93.500 970.000 Inventory Land Equipment Accumulated depreciation Investment in Son (cost basis) 80,000 50,000 288,000 40,000 $ 453.000 Liabilities & Shareholders' equity Accounts payable Notes payable Bonds payable Common shares $ 80,000 10,000 $ 45,000 32,000 273,000 43,000 60.000 S 453.000 180,000 480,000 220,000 $ 970.000 Retained earmings Income Statements For the year ended December 31, Year 3 Son Par Ltd $ 757,000 14,000 ompany 490,000 Sales Other income Cost of goods sold Depreciation/amortization expense Administration expense Other expenses Income tax expense 490,000 96,000 45,000 58,000 22,000 $ 290,000 60,000 30,000 80,000 10.000 20.000 Net income 60.000 Required: a. Prepare the Calculate and Allocation of the Acquisition Differential and the AD changes: amortization/impairment schedules. b. Calculate the consolidated net income for Year 3 c. Calculate the consolidated retained eamings at Jamuary 1, Year 3. d. Prepare the three (3) consolidated financial statements for Par, December 31. Year 3, using the direct approach (in good format) Hints: Goodwill $36,000. AD left Dec. 31, Year 3 $28,300. Total Consolidated Assets $1,350,800 Note: there are 2 separate lines for Equipment less accumulated depreciation on Cons B/S hence do not show a net number