Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Question 2 6 2 0 p t s You are given the following data for a European Call Option on a non - dividend paying

Question

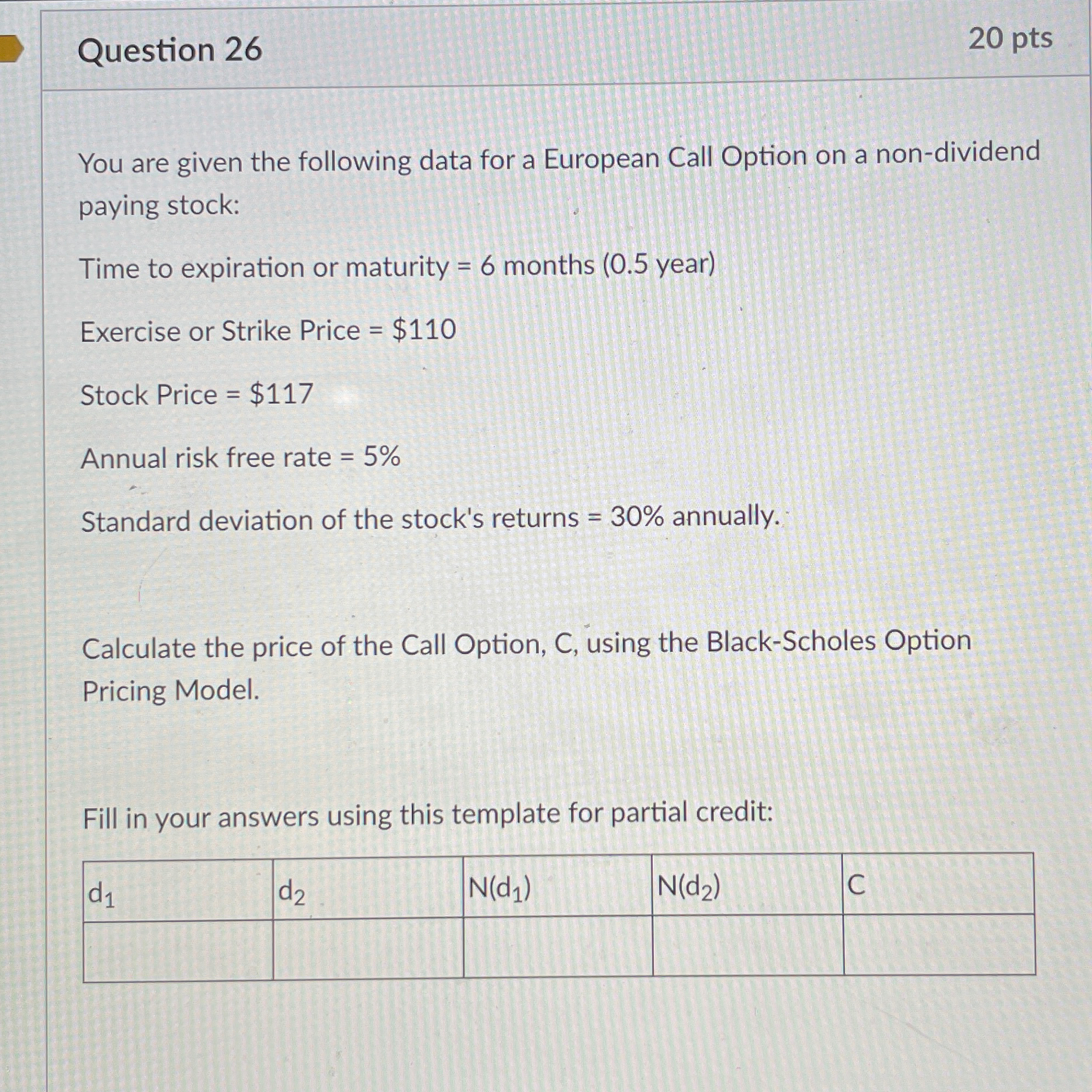

You are given the following data for a European Call Option on a nondividend paying stock:

Time to expiration or maturity months year

Exercise or Strike Price $

Stock Price $

Annual risk free rate

Standard deviation of the stock's returns annually.

Calculate the price of the Call Option, C using the BlackScholes Option Pricing Model.

Fill in your answers using this template for partial credit:

table

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: R. Charles Moyer, William J. Kretlow, James R. Mcguigan

8th Edition

0324065914, 9780324065916