Question

Question 2 (7 points total): Suppose the company A entered into an interest rate swap deal with a notional amount of $100M USD that is

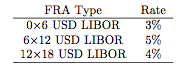

Question 2 (7 points total): Suppose the company A entered into an interest rate swap deal with a notional amount of $100M USD that is written on 6M LIBOR rate. The exchange is made semi-annually and the swap had maturity of 2 years at the time of initiation with a fixed swap rate of 4%. What is the present value of this swap to Company A, who is receiving fixed side of cash flow, today which is after 1 year since the swap deal was initiated? Assume that the exchange of cash has just taken place. Also assume that continuously compounded annual OIS rate is 5% for all maturities. The following FRA rates are observed in the market today on 6M LIBOR.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Richard Stanton

2nd Edition

1519662106, 978-1519662101