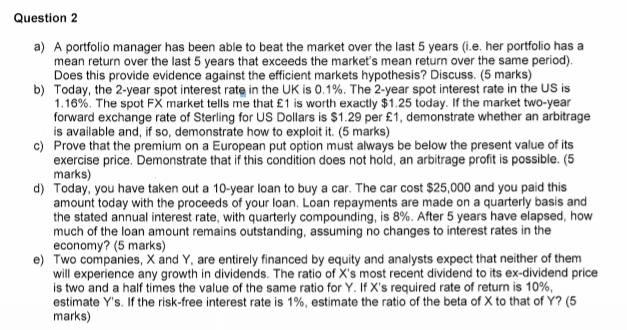

Question 2 a) A portfolio Manager has been able to beat the market over the last 5 years (.e. her portfolio has a mean return over the last 5 years that exceeds the market's mean return over the same period). Does this provide evidence against the efficient markets hypothesis? Discuss. (5 marks) b) Today, the 2-year spot interest rate in the UK is 0.1%. The 2-year spot interest rate in the US is 1.16%. The spot FX market tells me that 1 is worth exactly $1.25 today. If the market two-year forward exchange rate of Sterling for US Dollars is $1.29 per 1, demonstrate whether an arbitrage is available and if so, demonstrate how to exploit it. (5 marks) c) Prove that the premium on a European put option must always be below the present value of its exercise price. Demonstrate that if this condition does not hold, an arbitrage profit is possible. (5 marks) d) Today, you have taken out a 10-year loan to buy a car. The car cost $25,000 and you paid this amount today with the proceeds of your loan. Loan repayments are made on a quarterly basis and the stated annual interest rate, with quarterly compounding, is 8%. After 5 years have elapsed, how much of the loan amount remains outstanding, assuming no changes to interest rates in the economy? (5 marks) e) Two companies, X and Y are entirely financed by equity and analysts expect that neither of them will experience any growth in dividends. The ratio of X's most recent dividend to its ex-dividend price is two and a half times the value of the same ratio for Y. If X's required rate of return is 10% estimate Y's. If the risk-free interest rate is 1%, estimate the ratio of the beta of X to that of Y? (5 marks) Question 2 a) A portfolio Manager has been able to beat the market over the last 5 years (.e. her portfolio has a mean return over the last 5 years that exceeds the market's mean return over the same period). Does this provide evidence against the efficient markets hypothesis? Discuss. (5 marks) b) Today, the 2-year spot interest rate in the UK is 0.1%. The 2-year spot interest rate in the US is 1.16%. The spot FX market tells me that 1 is worth exactly $1.25 today. If the market two-year forward exchange rate of Sterling for US Dollars is $1.29 per 1, demonstrate whether an arbitrage is available and if so, demonstrate how to exploit it. (5 marks) c) Prove that the premium on a European put option must always be below the present value of its exercise price. Demonstrate that if this condition does not hold, an arbitrage profit is possible. (5 marks) d) Today, you have taken out a 10-year loan to buy a car. The car cost $25,000 and you paid this amount today with the proceeds of your loan. Loan repayments are made on a quarterly basis and the stated annual interest rate, with quarterly compounding, is 8%. After 5 years have elapsed, how much of the loan amount remains outstanding, assuming no changes to interest rates in the economy? (5 marks) e) Two companies, X and Y are entirely financed by equity and analysts expect that neither of them will experience any growth in dividends. The ratio of X's most recent dividend to its ex-dividend price is two and a half times the value of the same ratio for Y. If X's required rate of return is 10% estimate Y's. If the risk-free interest rate is 1%, estimate the ratio of the beta of X to that of Y