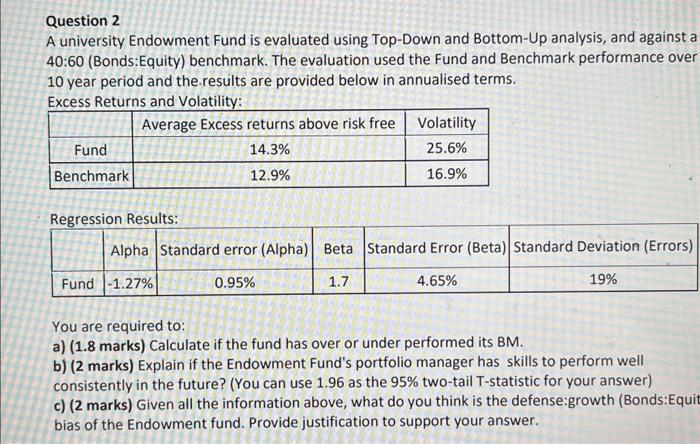

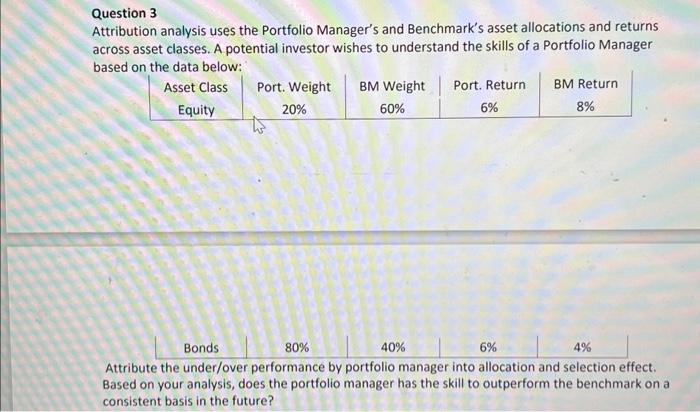

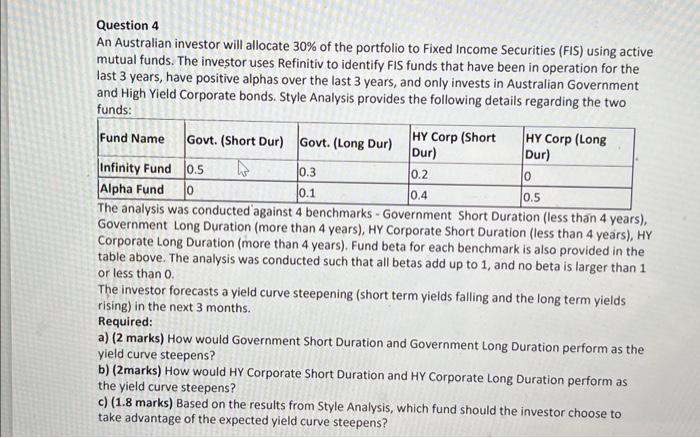

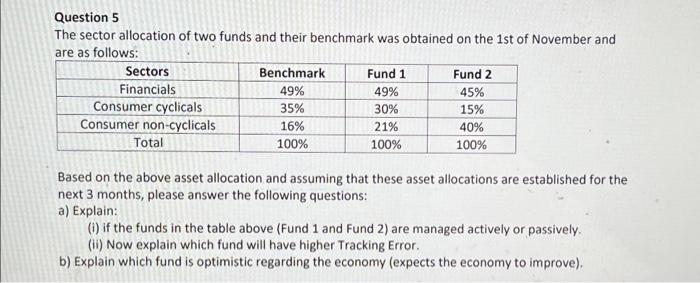

Question 2 A university Endowment Fund is evaluated using Top-Down and Bottom-Up analysis, and against a 40:60 (Bonds: Equity) benchmark. The evaluation used the Fund and Benchmark performance over 10 year period and the results are provided below in annualised terms. Excess Returns and Volatilitv: You are required to: a) (1.8 marks) Calculate if the fund has over or under performed its BM. b) ( 2 marks) Explain if the Endowment Fund's portfolio manager has skills to perform well consistently in the future? (You can use 1.96 as the 95% two-tail T-statistic for your answer) c) ( 2 marks) Given all the information above, what do you think is the defense:growth (Bonds:Equit bias of the Endowment fund. Provide justification to support your answer. Question 3 Attribution analysis uses the Portfolio Manager's and Benchmark's asset allocations and returns across asset classes. A potential investor wishes to understand the skills of a Portfolio Manager based on the data holnw: Attribute the under/over performance by portfolio manager into allocation and selection effect. Based on your analysis, does the portfolio manager has the skill to outperform the benchmark on a consistent basis in the future? Question 4 An Australian investor will allocate 30% of the portfolio to Fixed Income Securities (FIS) using active mutual funds. The investor uses Refinitiv to identify FIS funds that have been in operation for the last 3 years, have positive alphas over the last 3 years, and only invests in Australian Government and High Yield Corporate bonds. Style Analysis provides the following details regarding the two funds: Mc adiysis was conducted against 4 benchmarks - Government Short Duration (less than 4 years), Government Long Duration (more than 4 years), HY Corporate Short Duration (less than 4 years), HY Corporate Long Duration (more than 4 years). Fund beta for each benchmark is also provided in the table above. The analysis was conducted such that all betas add up to 1 , and no beta is larger than 1 or less than 0. The investor forecasts a yield curve steepening (short term yields falling and the long term yields rising) in the next 3 months. Required: a) ( 2 marks) How would Government Short Duration and Government Long Duration perform as the yield curve steepens? b) (2marks) How would HY Corporate Short Duration and HY Corporate Long Duration perform as the yield curve steepens? c) (1.8 marks) Based on the results from Style Analysis, which fund should the investor choose to take advantage of the expected yield curve steepens? Question 5 The sector allocation of two funds and their benchmark was obtained on the 1st of November and are as follows: Based on the above asset allocation and assuming that these asset allocations are established for the next 3 months, please answer the following questions: a) Explain: (i) if the funds in the table above (Fund 1 and Fund 2) are managed actively or passively. (ii) Now explain which fund will have higher Tracking Error. b) Explain which fund is optimistic regarding the economy (expects the economy to improve). Question 6 James makes the following incorrect statements regarding the advantages and disadvantages of an Open-end funds (OEF) over Close-end funds (CEFs). Explain why his statements are incorrect. Make sure you address each statement individually. Statement 1: Open-end funds will have lower (compared with CEFs) management fee since they can increase the assets undermanagement and take advantage of the economies of scale. Statement 2: Open end funds are not riskier than CEFs since OEFs are restricted from holding short positions, use derivatives or borrow money, while OEFs have an all-equity structure. Statement 3: Open-end funds' NAV are more transparent than close-end funds, because the NAV of an OEF will only increase or decrease If the value of the asset changes in value