Answered step by step

Verified Expert Solution

Question

1 Approved Answer

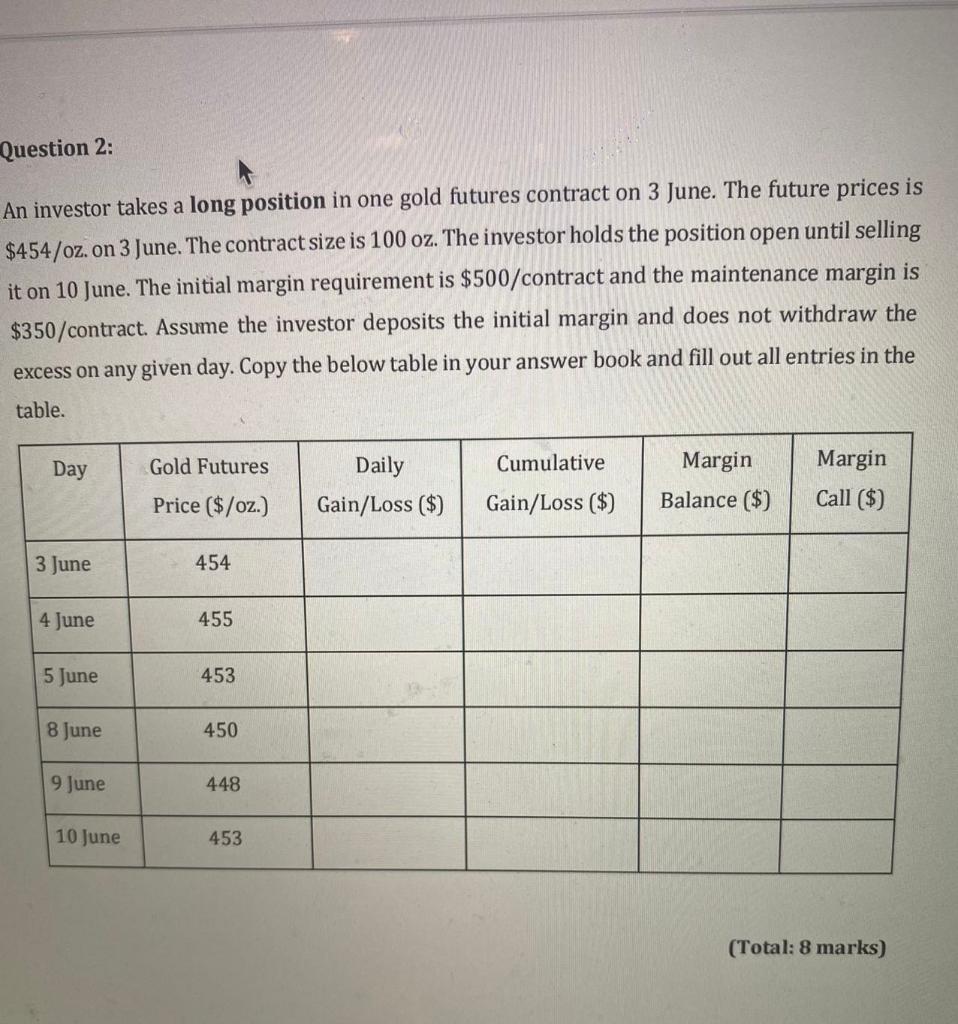

Question 2: An investor takes a long position in one gold futures contract on 3 June. The future prices is $454/ oz. on 3 June.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Emerald Handbook On Cryptoassets Investment Opportunities And Challenges

Authors: H. Kent Baker, Hugo Benedetti, Ehsan Nikbakht, Sean Stein Smith

1st Edition

1804553212, 978-1804553213