Answered step by step

Verified Expert Solution

Question

1 Approved Answer

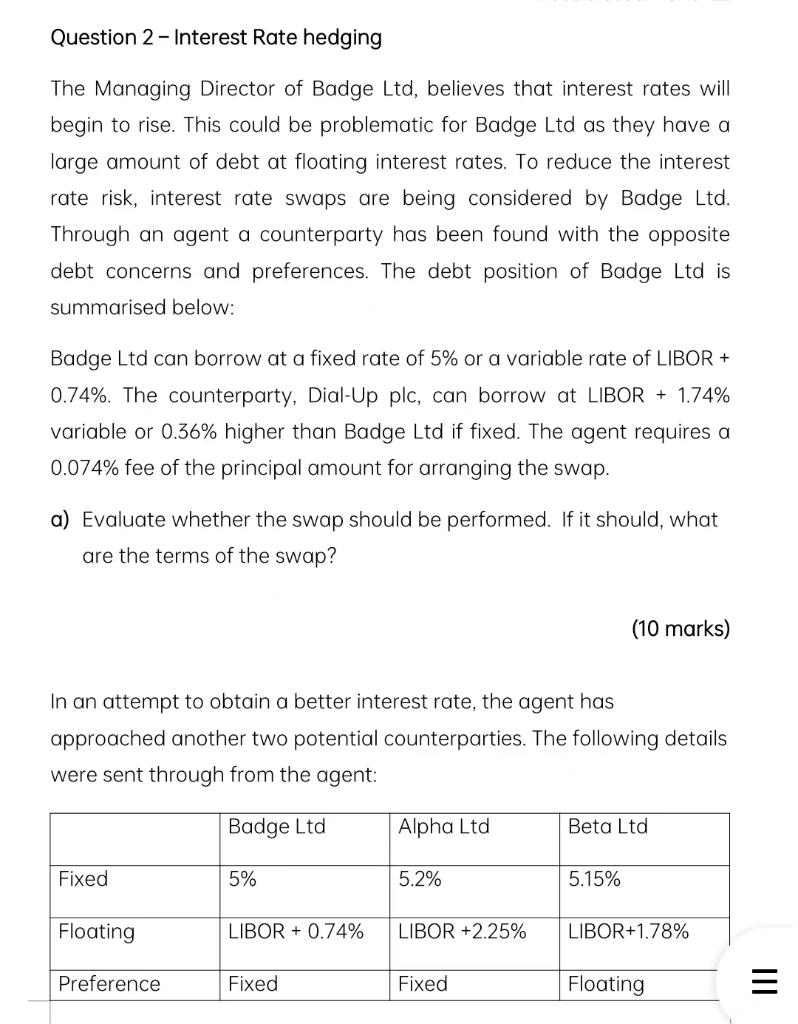

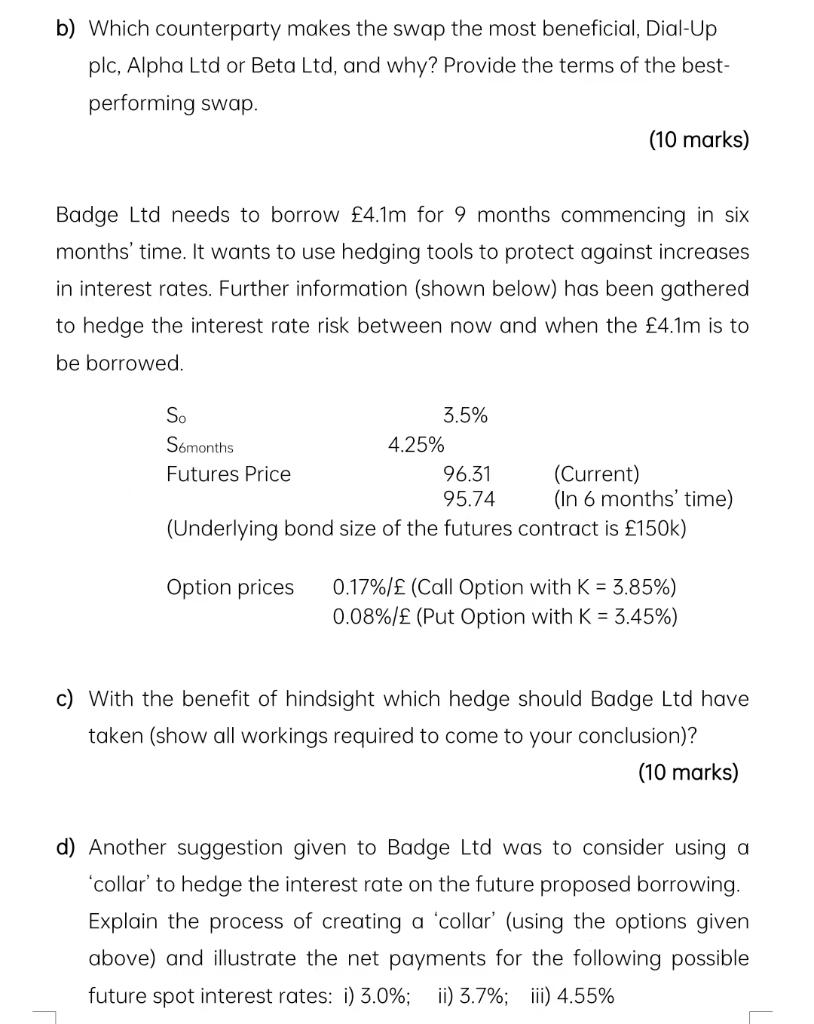

Question 2 - Interest Rate hedging The Managing Director of Badge Ltd, believes that interest rates will begin to rise. This could be problematic for

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How Much Can I Spend In Retirement A Guide To Investment Based Retirement Income Strategies

Authors: Wade D Pfau

1st Edition

1945640022, 978-1945640025