Answered step by step

Verified Expert Solution

Question

1 Approved Answer

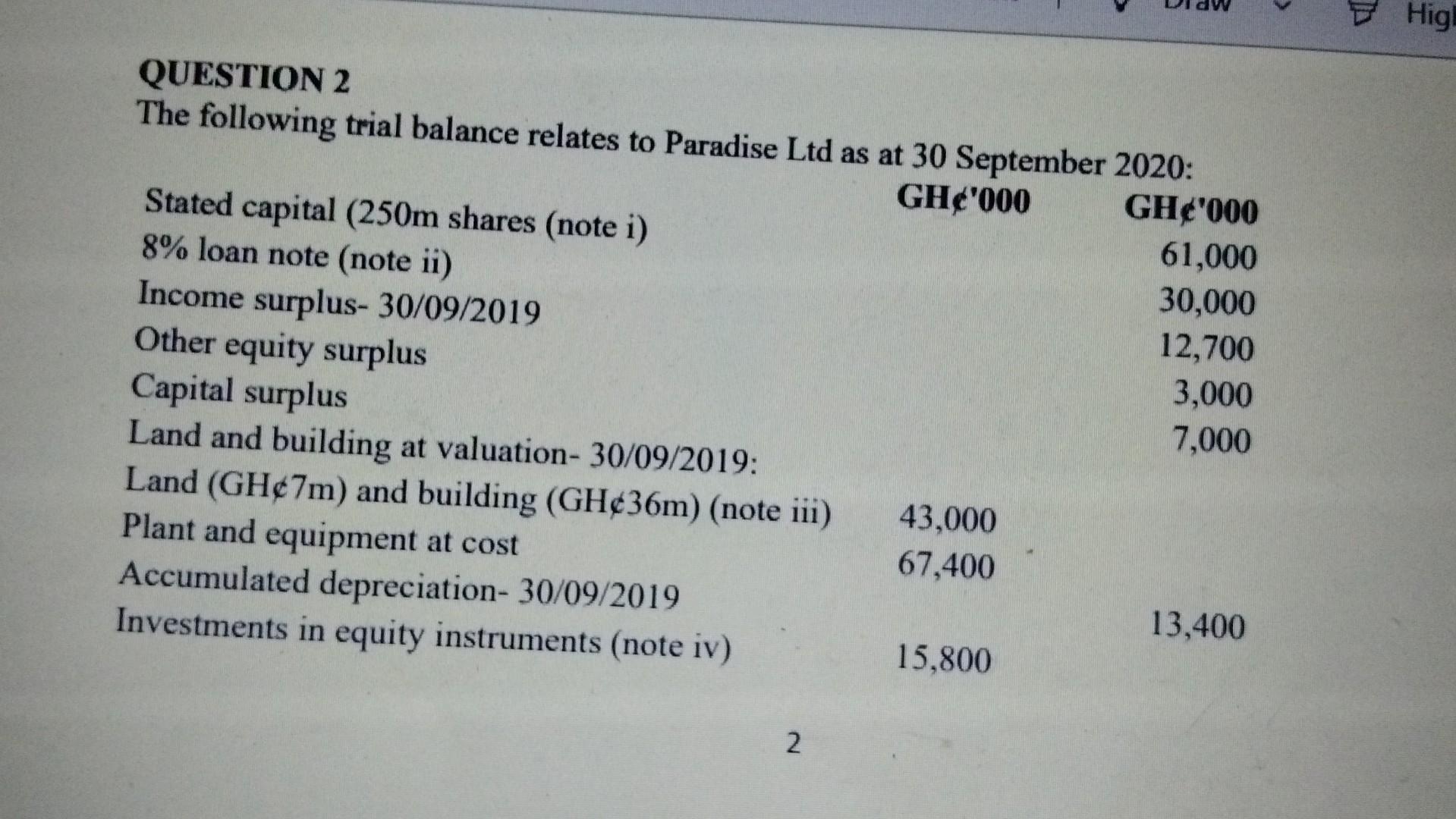

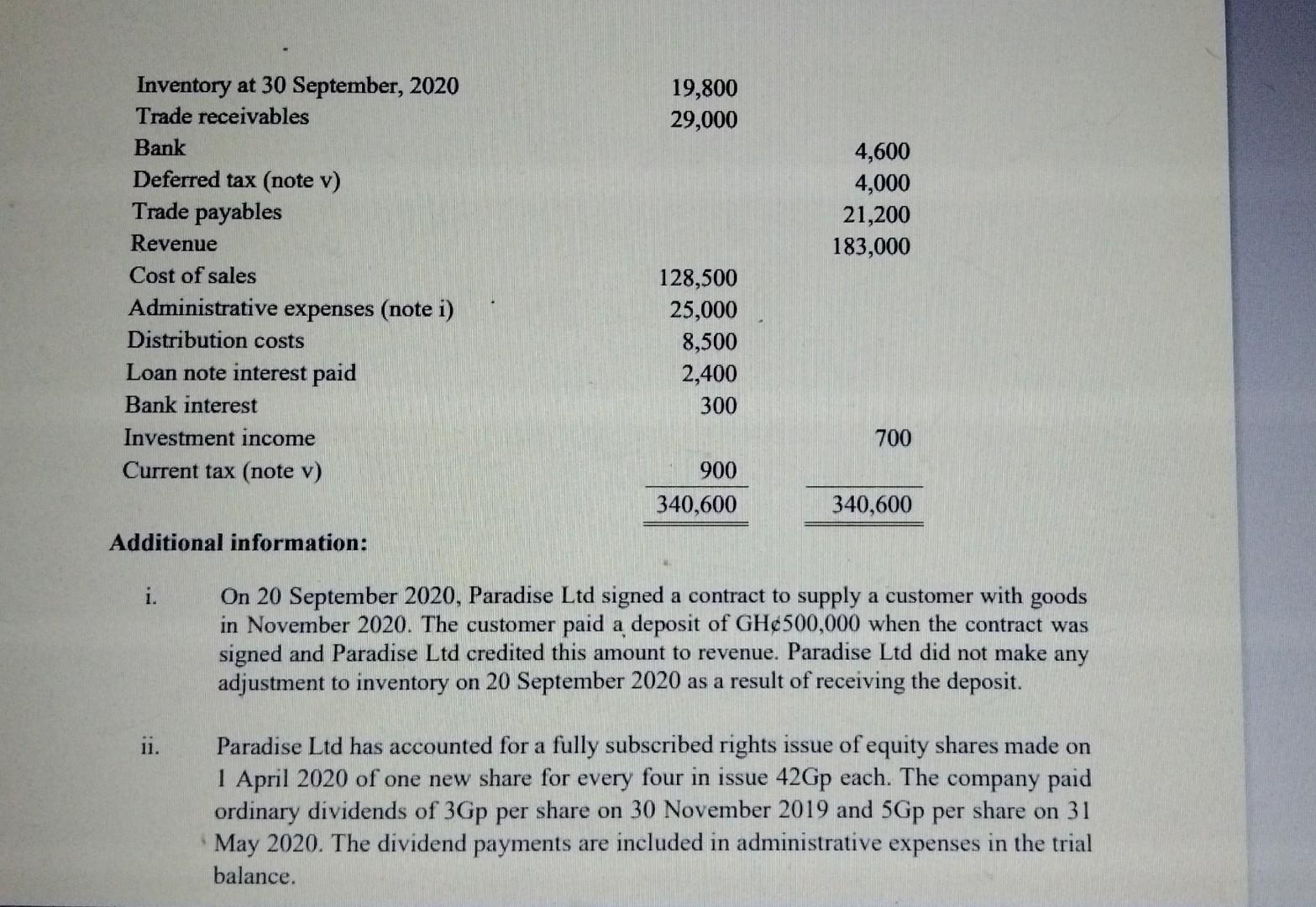

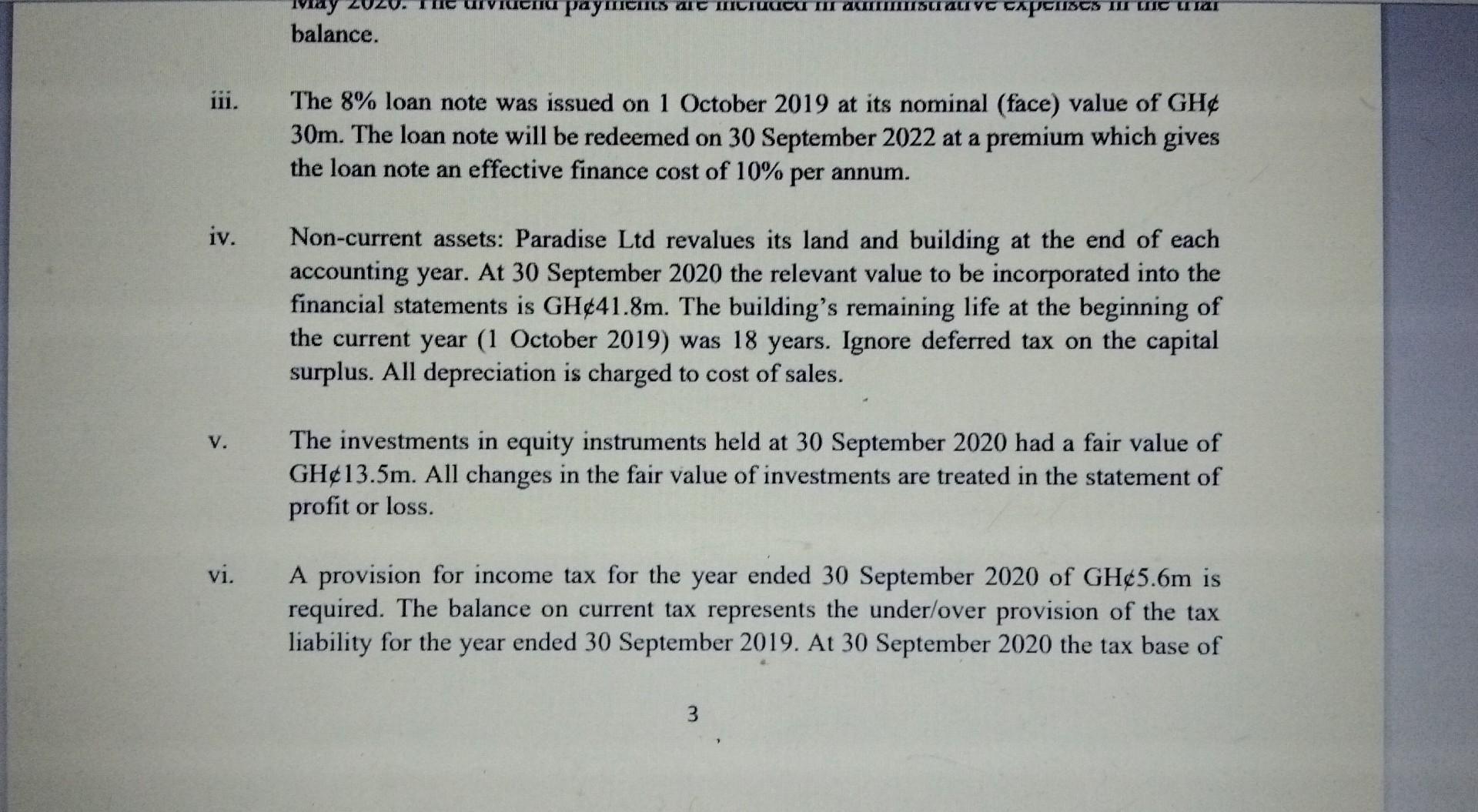

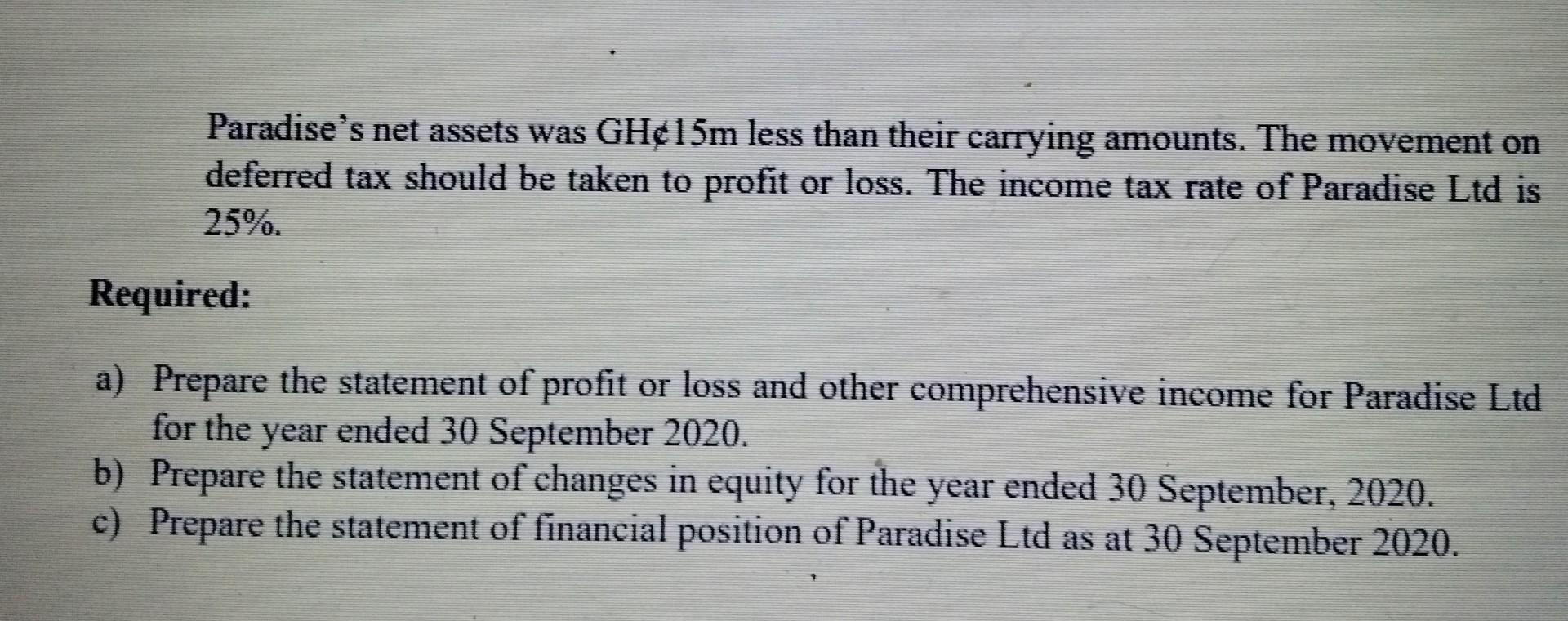

QUESTION 2 The following trial balance relates to Paradise Ltd as at 30 September 202n. i. On 20 September 2020, Paradise Ltd signed a contract

QUESTION 2 The following trial balance relates to Paradise Ltd as at 30 September 202n. i. On 20 September 2020, Paradise Ltd signed a contract to supply a customer with goods in November 2020. The customer paid a deposit of GH500,000 when the contract was signed and Paradise Ltd credited this amount to revenue. Paradise Ltd did not make any adjustment to inventory on 20 September 2020 as a result of receiving the deposit. ii. Paradise Ltd has accounted for a fully subscribed rights issue of equity shares made on 1 April 2020 of one new share for every four in issue 42Gp each. The company paid ordinary dividends of 3Gp per share on 30 November 2019 and 5Gp per share on 31 May 2020. The dividend payments are included in administrative expenses in the trial balance. iii. The 8% loan note was issued on 1 October 2019 at its nominal (face) value of GH 30m. The loan note will be redeemed on 30 September 2022 at a premium which gives the loan note an effective finance cost of 10% per annum. iv. Non-current assets: Paradise Ltd revalues its land and building at the end of each accounting year. At 30 September 2020 the relevant value to be incorporated into the financial statements is GH41.8m. The building's remaining life at the beginning of the current year (1 October 2019) was 18 years. Ignore deferred tax on the capital surplus. All depreciation is charged to cost of sales. v. The investments in equity instruments held at 30 September 2020 had a fair value of GH /13.5m. All changes in the fair value of investments are treated in the statement of profit or loss. vi. A provision for income tax for the year ended 30 September 2020 of GH\&5.6m is required. The balance on current tax represents the under/over provision of the tax liability for the year ended 30 September 2019. At 30 September 2020 the tax base of Paradise's net assets was GH\&15m less than their carrying amounts. The movement on deferred tax should be taken to profit or loss. The income tax rate of Paradise Ltd is 25% Required: a) Prepare the statement of profit or loss and other comprehensive income for Paradise Ltd for the year ended 30 September 2020. b) Prepare the statement of changes in equity for the year ended 30 September, 2020. c) Prepare the statement of financial position of Paradise Ltd as at 30 September 2020. QUESTION 2 The following trial balance relates to Paradise Ltd as at 30 September 202n. i. On 20 September 2020, Paradise Ltd signed a contract to supply a customer with goods in November 2020. The customer paid a deposit of GH500,000 when the contract was signed and Paradise Ltd credited this amount to revenue. Paradise Ltd did not make any adjustment to inventory on 20 September 2020 as a result of receiving the deposit. ii. Paradise Ltd has accounted for a fully subscribed rights issue of equity shares made on 1 April 2020 of one new share for every four in issue 42Gp each. The company paid ordinary dividends of 3Gp per share on 30 November 2019 and 5Gp per share on 31 May 2020. The dividend payments are included in administrative expenses in the trial balance. iii. The 8% loan note was issued on 1 October 2019 at its nominal (face) value of GH 30m. The loan note will be redeemed on 30 September 2022 at a premium which gives the loan note an effective finance cost of 10% per annum. iv. Non-current assets: Paradise Ltd revalues its land and building at the end of each accounting year. At 30 September 2020 the relevant value to be incorporated into the financial statements is GH41.8m. The building's remaining life at the beginning of the current year (1 October 2019) was 18 years. Ignore deferred tax on the capital surplus. All depreciation is charged to cost of sales. v. The investments in equity instruments held at 30 September 2020 had a fair value of GH /13.5m. All changes in the fair value of investments are treated in the statement of profit or loss. vi. A provision for income tax for the year ended 30 September 2020 of GH\&5.6m is required. The balance on current tax represents the under/over provision of the tax liability for the year ended 30 September 2019. At 30 September 2020 the tax base of Paradise's net assets was GH\&15m less than their carrying amounts. The movement on deferred tax should be taken to profit or loss. The income tax rate of Paradise Ltd is 25% Required: a) Prepare the statement of profit or loss and other comprehensive income for Paradise Ltd for the year ended 30 September 2020. b) Prepare the statement of changes in equity for the year ended 30 September, 2020. c) Prepare the statement of financial position of Paradise Ltd as at 30 September 2020

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Charles Horngren

2nd Edition

0558514847, 978-0558514846