Answered step by step

Verified Expert Solution

Question

1 Approved Answer

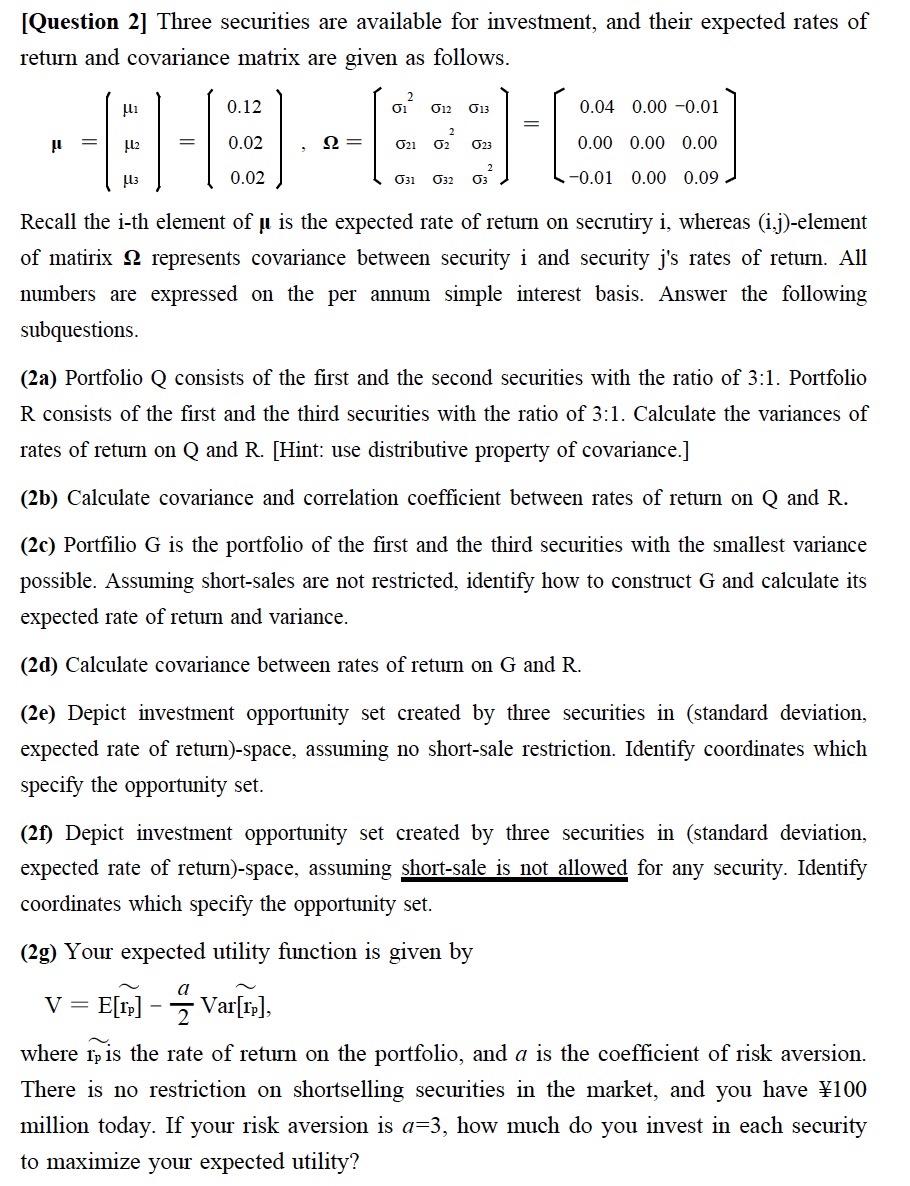

[ Question 2 ] Three securities are available for investment, and their expected rates of return and covariance matrix are given as follows. = (

Question Three securities are available for investment, and their expected rates of

return and covariance matrix are given as follows.

Recall the th element of is the expected rate of return on secrutiry whereas element

of matirix represents covariance between security i and security js rates of return. All

numbers are expressed on the per annum simple interest basis. Answer the following

subquestions.

a Portfolio Q consists of the first and the second securities with the ratio of : Portfolio

consists of the first and the third securities with the ratio of : Calculate the variances of

rates of return on and Hint: use distributive property of covariance.

b Calculate covariance and correlation coefficient between rates of return on Q and R

c Portfilio is the portfolio of the first and the third securities with the smallest variance

possible. Assuming shortsales are not restricted, identify how to construct and calculate its

expected rate of return and variance.

d Calculate covariance between rates of return on and

e Depict investment opportunity set created by three securities in standard deviation,

expected rate of returnspace, assuming no shortsale restriction. Identify coordinates which

specify the opportunity set.

f Depict investment opportunity set created by three securities in standard deviation,

expected rate of returnspace, assuming shortsale is not allowed for any security. Identify

coordinates which specify the opportunity set.

g Your expected utility function is given by

where widetilde is the rate of return on the portfolio, and is the coefficient of risk aversion.

There is no restriction on shortselling securities in the market, and you have

million today. If your risk aversion is how much do you invest in each security

to maximize your expected utility?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Institutions

Authors: Jeff Madura

8th Edition

0324568215, 978-0324568219