Answered step by step

Verified Expert Solution

Question

1 Approved Answer

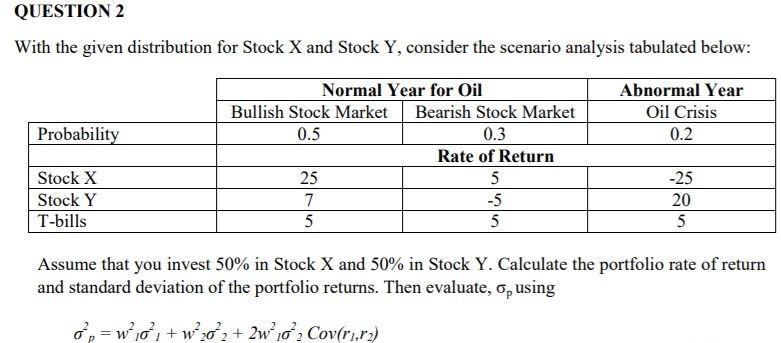

QUESTION 2 With the given distribution for Stock X and Stock Y, consider the scenario analysis tabulated below: Abnormal Year Oil Crisis 0.2 Probability Normal

QUESTION 2 With the given distribution for Stock X and Stock Y, consider the scenario analysis tabulated below: Abnormal Year Oil Crisis 0.2 Probability Normal Year for Oil Bullish Stock Market Bearish Stock Market 0.5 0.3 Rate of Return 25 5 7 -5 5 5 Stock X Stock Y T-bills -25 20 5 Assume that you invest 50% in Stock X and 50% in Stock Y. Calculate the portfolio rate of return and standard deviation of the portfolio returns. Then evaluate, or using =w? j, +w20+2 + 2w16 Cov(r,r2)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Econometrics

Authors: R Hill

4th Edition

1118136969, 9781118136966