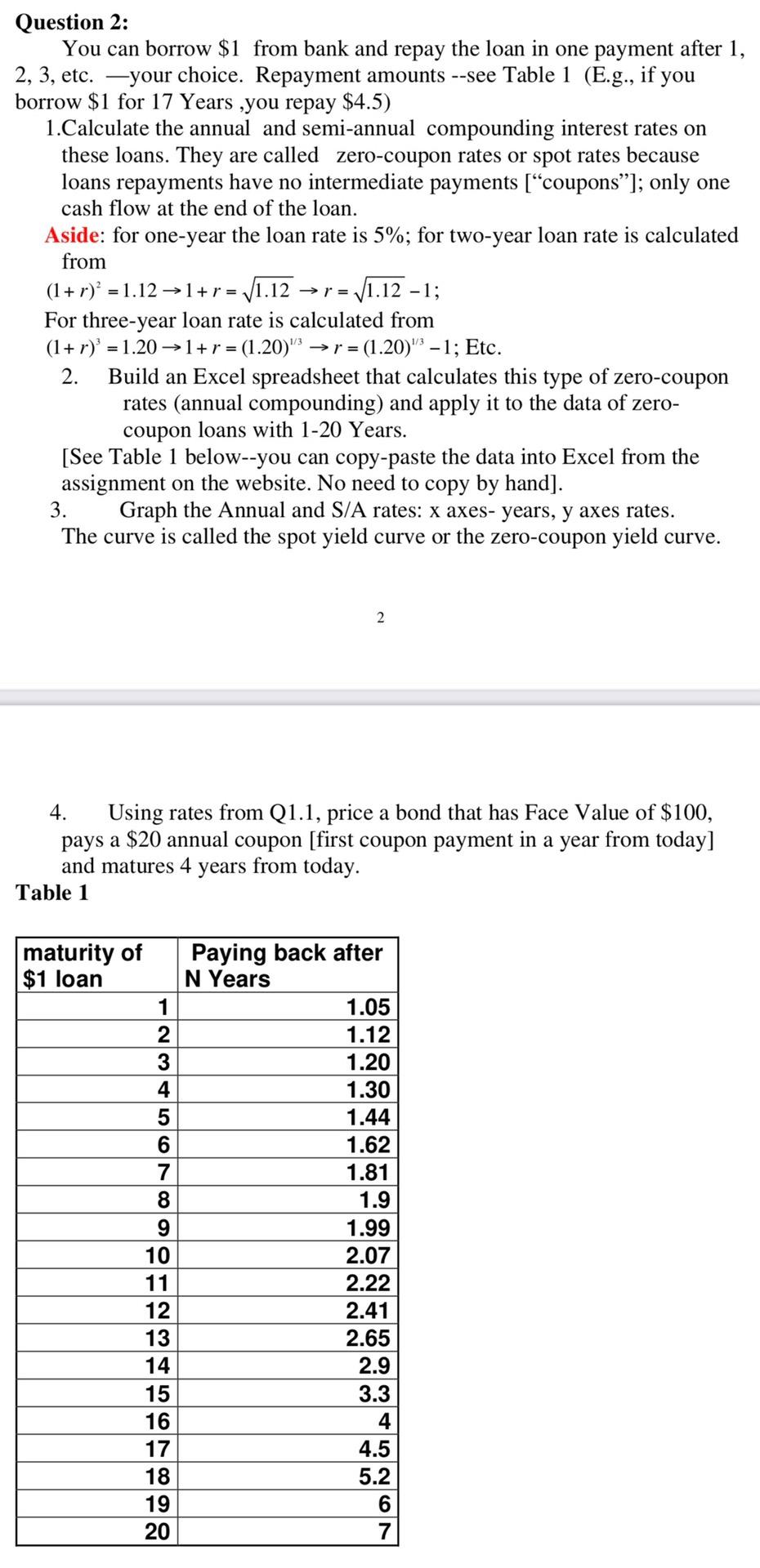

Question 2: You can borrow $1 from bank and repay the loan in one payment after 1, 2, 3, etc. your choice. Repayment amounts --see Table 1 (E.g., if you borrow $1 for 17 Years ,you repay $4.5) 1.Calculate the annual and semi-annual compounding interest rates on these loans. They are called zero-coupon rates or spot rates because loans repayments have no intermediate payments ["coupons]; only one cash flow at the end of the loan. Aside: for one-year the loan rate is 5%; for two-year loan rate is calculated from (1 + r) = 1.12 l+r = 11.12 = V1.12 -1; For three-year loan rate is calculated from (1+r) = 1.20 1+r = (1.20)" >r = (1.20)" 1; Etc. 2. Build an Excel spreadsheet that calculates this type of zero-coupon rates (annual compounding) and apply it to the data of zero- coupon loans with 1-20 Years. [See Table 1 below--you can copy-paste the data into Excel from the assignment on the website. No need to copy by hand). 3. Graph the Annual and S/A rates: x axes- years, y axes rates. The curve is called the spot yield curve or the zero-coupon yield curve. ->r = 2 4. Using rates from Q1.1, price a bond that has Face Value of $100, pays a $20 annual coupon [first coupon payment in a year from today] and matures 4 years from today. Table 1 maturity of $1 loan 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Paying back after N Years 1.05 1.12 1.20 1.30 1.44 1.62 1.81 1.9 1.99 2.07 2.22 2.41 2.65 2.9 3.3 4 4.5 5.2 Question 2: You can borrow $1 from bank and repay the loan in one payment after 1, 2, 3, etc. your choice. Repayment amounts --see Table 1 (E.g., if you borrow $1 for 17 Years ,you repay $4.5) 1.Calculate the annual and semi-annual compounding interest rates on these loans. They are called zero-coupon rates or spot rates because loans repayments have no intermediate payments ["coupons]; only one cash flow at the end of the loan. Aside: for one-year the loan rate is 5%; for two-year loan rate is calculated from (1 + r) = 1.12 l+r = 11.12 = V1.12 -1; For three-year loan rate is calculated from (1+r) = 1.20 1+r = (1.20)" >r = (1.20)" 1; Etc. 2. Build an Excel spreadsheet that calculates this type of zero-coupon rates (annual compounding) and apply it to the data of zero- coupon loans with 1-20 Years. [See Table 1 below--you can copy-paste the data into Excel from the assignment on the website. No need to copy by hand). 3. Graph the Annual and S/A rates: x axes- years, y axes rates. The curve is called the spot yield curve or the zero-coupon yield curve. ->r = 2 4. Using rates from Q1.1, price a bond that has Face Value of $100, pays a $20 annual coupon [first coupon payment in a year from today] and matures 4 years from today. Table 1 maturity of $1 loan 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Paying back after N Years 1.05 1.12 1.20 1.30 1.44 1.62 1.81 1.9 1.99 2.07 2.22 2.41 2.65 2.9 3.3 4 4.5 5.2