Answered step by step

Verified Expert Solution

Question

1 Approved Answer

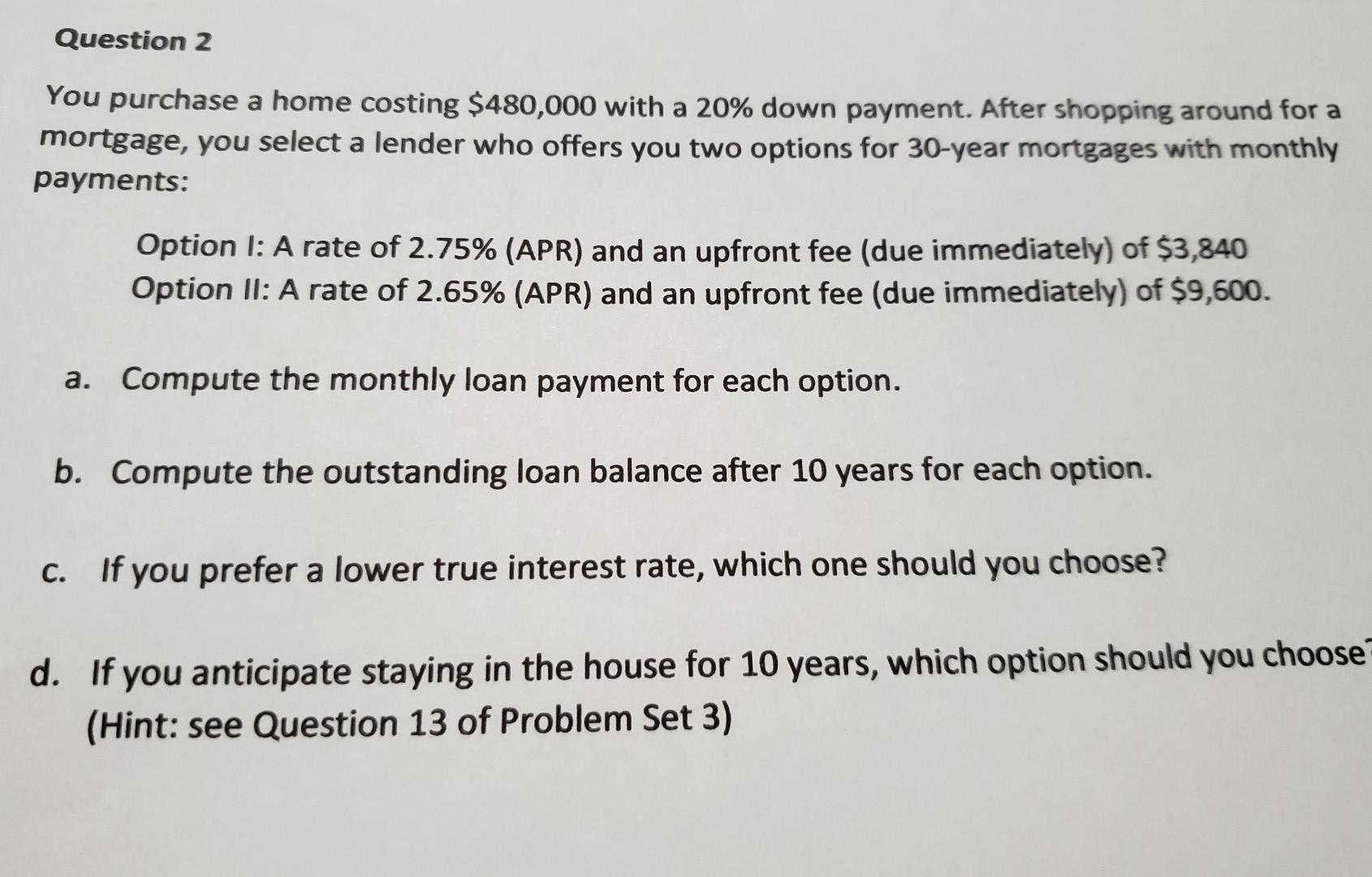

Question 2 You purchase a home costing $480,000 with a 20% down payment. After shopping around for a mortgage, you select a lender who offers

Question 2 You purchase a home costing $480,000 with a 20% down payment. After shopping around for a mortgage, you select a lender who offers you two options for 30-year mortgages with monthly payments: Option I: A rate of 2.75% (APR) and an upfront fee (due immediately) of $3,840 Option II: A rate of 2.65% (APR) and an upfront fee (due immediately) of $9,600. a. Compute the monthly loan payment for each option. b. Compute the outstanding loan balance after 10 years for each option. C. If you prefer a lower true interest rate, which one should you choose? d. If you anticipate staying in the house for 10 years, which option should you choose (Hint: see Question 13 of Problem Set 3)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptocurrency And Bitcoin 101 Beginner S Guide To Becoming A Professional Trader And Investor In Digital Currency Without The Fear Of Liquidation Or Crash

Authors: Robert J Lewis

1st Edition

979-8826353905