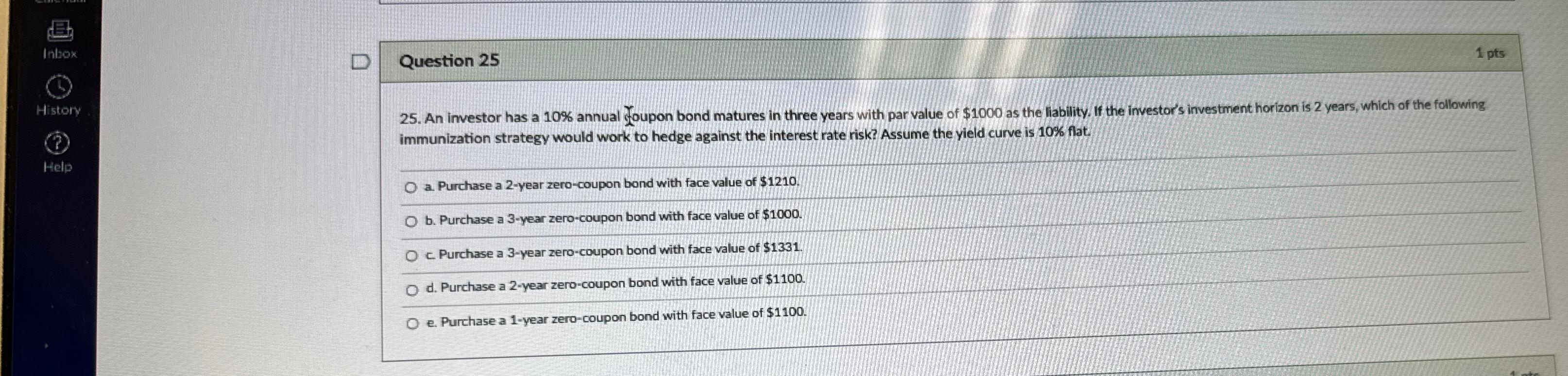

Question 25 1 pts 25. An investor has a 10% annual Ifoupon bond matures in three years with par value of $1000 as the liability.

Question 25\ 1 pts\ 25. An investor has a

10%annual Ifoupon bond matures in three years with par value of

$1000as the liability. If the investor's investment horizon is 2 years, which of the following immunization strategy would work to hedge against the interest rate risk? Assume the yield curve is

10%flat\ a. Purchase a 2-year zero-coupon bond with face value of

$1210.\ b. Purchase a 3-year zero-coupon bond with face value of

$1000.\ c. Purchase a 3-year zero-coupon bond with face value of

$1331.\ d. Purchase a 2-year zero-coupon bond with face value of

$1100.\ e. Purchase a 1-year zero-coupon bond with face value of

$1100.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Steven Berger

4th Edition

1118801687, 978-1118801680