Answered step by step

Verified Expert Solution

Question

1 Approved Answer

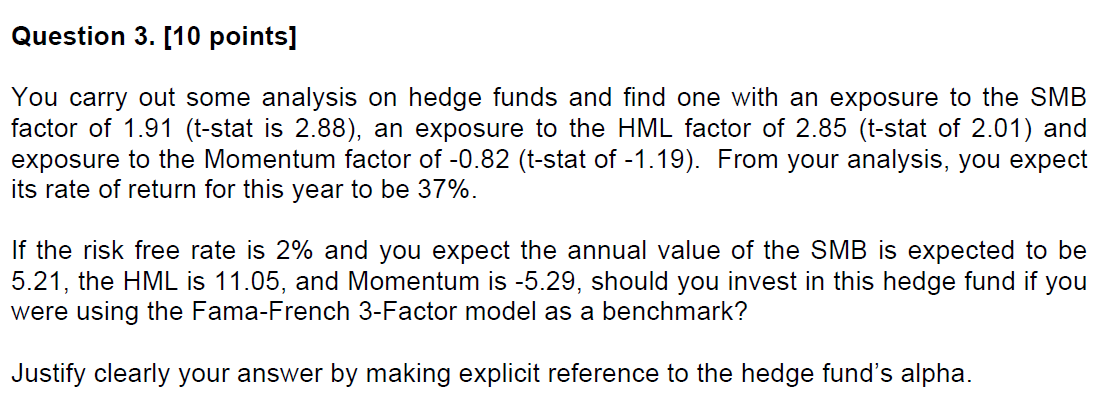

Question 3. [10 points] You carry out some analysis on hedge funds and find one with an exposure to the SMB factor of 1.91 (t-stat

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Trainer Online Purchase Managerial Accounting

Authors: Carl S. Warren, James M. Reeve, Philip E. Fess

8th Edition