Answered step by step

Verified Expert Solution

Question

1 Approved Answer

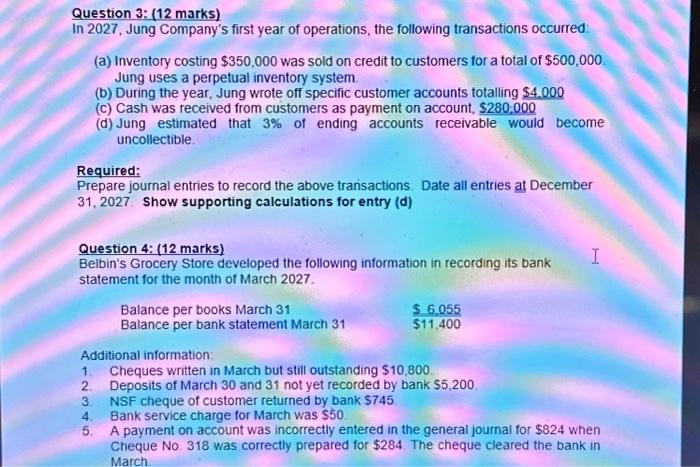

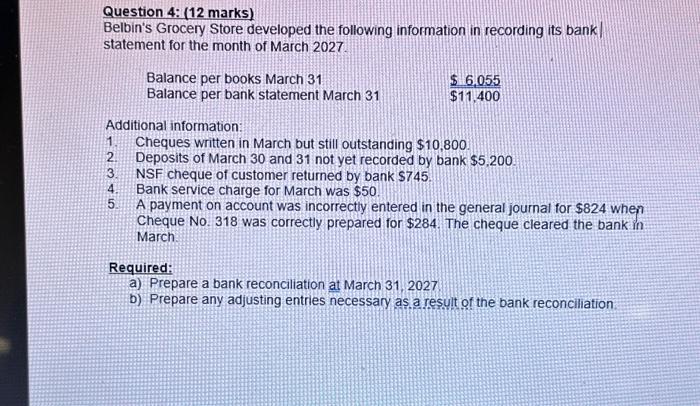

Question 3: (12 marks) In 2027, Jung Company's first year of operations, the following transactions occurred: (a) Inventory costing $350,000 was sold on credit to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing A Practical Approach

Authors: Fiona Campbell, Robyn Moroney, Jane Hamilton, Valerie Warren

2nd Canadian edition

9781118377901, 1118377907, 1119048095, 978-1118849415