Answered step by step

Verified Expert Solution

Question

1 Approved Answer

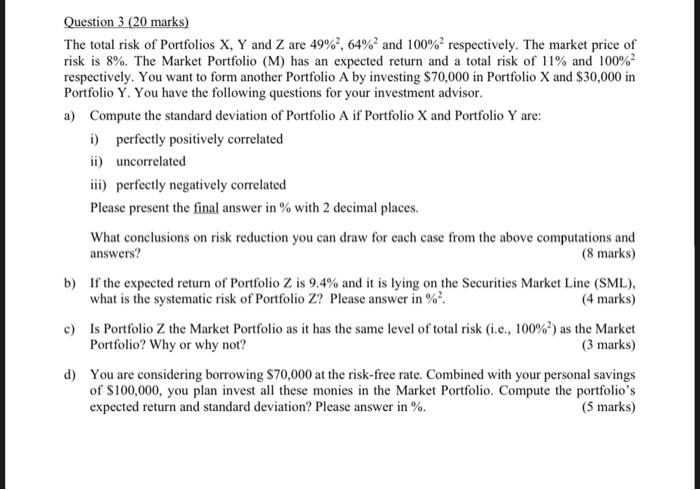

Question 3 (20 marks) The total risk of Portfolios X, Y and Z are 49%?,64% and 100% respectively. The market price of risk is 8%.

Question 3 (20 marks) The total risk of Portfolios X, Y and Z are 49%?,64% and 100% respectively. The market price of risk is 8%. The Market Portfolio (M) has an expected return and a total risk of 11% and 100% respectively. You want to form another Portfolio A by investing $70,000 in Portfolio X and $30,000 in Portfolio Y. You have the following questions for your investment advisor. a) Compute the standard deviation of Portfolio A if Portfolio X and Portfolio Y are: i) perfectly positively correlated ii) uncorrelated iii) perfectly negatively correlated Please present the final answer in % with 2 decimal places, What conclusions on risk reduction you can draw for each case from the above computations and answers? (8 marks) b) If the expected return of Portfolio Z is 9.4% and it is lying on the Securities Market Line (SML), what is the systematic risk of Portfolio Z? Please answer in %. (4 marks) c) Is Portfolio Z the Market Portfolio as it has the same level of total risk (i.c., 100%?) as the Market Portfolio? Why or why not? (3 marks) d) You are considering borrowing $70,000 at the risk-free rate. Combined with your personal savings of $100,000, you plan invest all these monies in the Market Portfolio. Compute the portfolio's expected return and standard deviation? Please answer in %. (5 marks) Question 3 (20 marks) The total risk of Portfolios X, Y and Z are 49%?,64% and 100% respectively. The market price of risk is 8%. The Market Portfolio (M) has an expected return and a total risk of 11% and 100% respectively. You want to form another Portfolio A by investing $70,000 in Portfolio X and $30,000 in Portfolio Y. You have the following questions for your investment advisor. a) Compute the standard deviation of Portfolio A if Portfolio X and Portfolio Y are: i) perfectly positively correlated ii) uncorrelated iii) perfectly negatively correlated Please present the final answer in % with 2 decimal places, What conclusions on risk reduction you can draw for each case from the above computations and answers? (8 marks) b) If the expected return of Portfolio Z is 9.4% and it is lying on the Securities Market Line (SML), what is the systematic risk of Portfolio Z? Please answer in %. (4 marks) c) Is Portfolio Z the Market Portfolio as it has the same level of total risk (i.c., 100%?) as the Market Portfolio? Why or why not? (3 marks) d) You are considering borrowing $70,000 at the risk-free rate. Combined with your personal savings of $100,000, you plan invest all these monies in the Market Portfolio. Compute the portfolio's expected return and standard deviation? Please answer in %

Question 3 (20 marks) The total risk of Portfolios X, Y and Z are 49%?,64% and 100% respectively. The market price of risk is 8%. The Market Portfolio (M) has an expected return and a total risk of 11% and 100% respectively. You want to form another Portfolio A by investing $70,000 in Portfolio X and $30,000 in Portfolio Y. You have the following questions for your investment advisor. a) Compute the standard deviation of Portfolio A if Portfolio X and Portfolio Y are: i) perfectly positively correlated ii) uncorrelated iii) perfectly negatively correlated Please present the final answer in % with 2 decimal places, What conclusions on risk reduction you can draw for each case from the above computations and answers? (8 marks) b) If the expected return of Portfolio Z is 9.4% and it is lying on the Securities Market Line (SML), what is the systematic risk of Portfolio Z? Please answer in %. (4 marks) c) Is Portfolio Z the Market Portfolio as it has the same level of total risk (i.c., 100%?) as the Market Portfolio? Why or why not? (3 marks) d) You are considering borrowing $70,000 at the risk-free rate. Combined with your personal savings of $100,000, you plan invest all these monies in the Market Portfolio. Compute the portfolio's expected return and standard deviation? Please answer in %. (5 marks) Question 3 (20 marks) The total risk of Portfolios X, Y and Z are 49%?,64% and 100% respectively. The market price of risk is 8%. The Market Portfolio (M) has an expected return and a total risk of 11% and 100% respectively. You want to form another Portfolio A by investing $70,000 in Portfolio X and $30,000 in Portfolio Y. You have the following questions for your investment advisor. a) Compute the standard deviation of Portfolio A if Portfolio X and Portfolio Y are: i) perfectly positively correlated ii) uncorrelated iii) perfectly negatively correlated Please present the final answer in % with 2 decimal places, What conclusions on risk reduction you can draw for each case from the above computations and answers? (8 marks) b) If the expected return of Portfolio Z is 9.4% and it is lying on the Securities Market Line (SML), what is the systematic risk of Portfolio Z? Please answer in %. (4 marks) c) Is Portfolio Z the Market Portfolio as it has the same level of total risk (i.c., 100%?) as the Market Portfolio? Why or why not? (3 marks) d) You are considering borrowing $70,000 at the risk-free rate. Combined with your personal savings of $100,000, you plan invest all these monies in the Market Portfolio. Compute the portfolio's expected return and standard deviation? Please answer in %

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Green And Sustainable Finance

Authors: Simon Thompson

2nd Edition

1398609242, 978-1398609242