Answered step by step

Verified Expert Solution

Question

1 Approved Answer

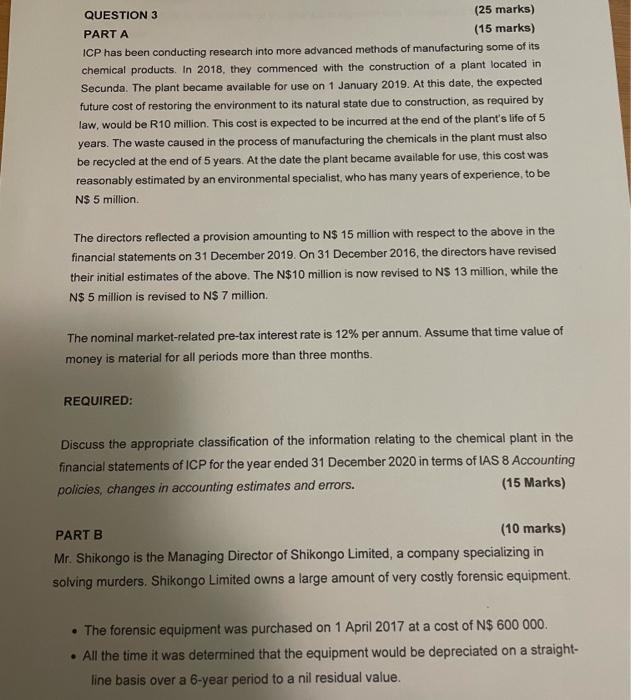

QUESTION 3 (25 marks) PART A (15 marks) ICP has been conducting research into more advanced methods of manufacturing some of its chemical products. In

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The HA HandBook Series Auditing The Legal Process Improving The Efficiency And Effectiveness Of Legal Counsel

Authors: Scott Fargason

1st Edition

0894134698, 978-0894134692