Answered step by step

Verified Expert Solution

Question

1 Approved Answer

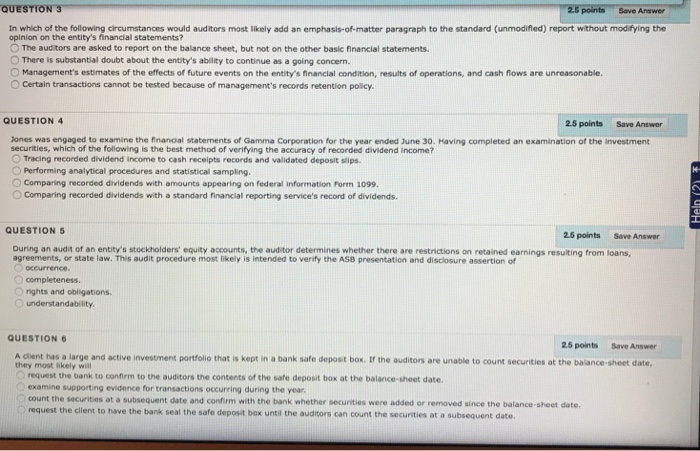

QUESTION 3 2.5 points Save Answer In which of the following circumstances would auditors most likely add an emphasis-of-matter paragraph to the standard (unmodifled) report

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Islamic Banks Positioning Study Regulatory Specificities And Audit Particularities

Authors: Hassen BEN OUHIBA

1st Edition

6206279790, 978-6206279792