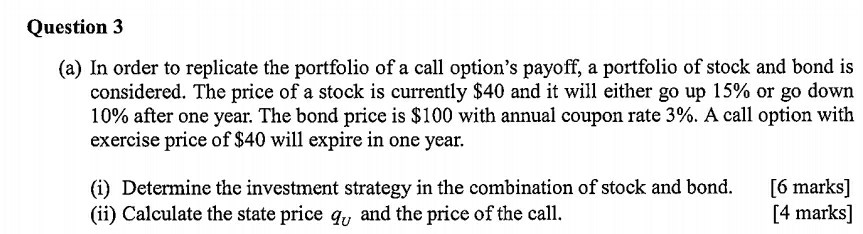

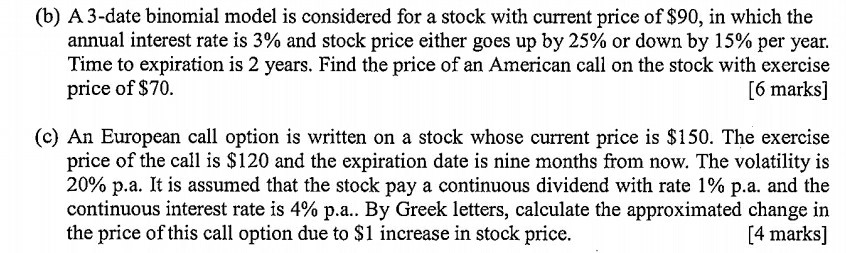

Question 3 (a) In order to replicate the portfolio of a call option's payoff, a portfolio of stock and bond is considered. The price of a stock is currently $40 and it will either go up 15% or go down 10% after one year. The bond price is $100 with annual coupon rate 3%. A call option with exercise price of $40 will expire in one year. (i) Determine the investment strategy in the combination of stock and bond. (ii) Calculate the state price qy and the price of the call. [6 marks] [4 marks] (b) A3-date binomial model is considered for a stock with current price of $90, in which the annual interest rate is 3% and stock price either goes up by 25% or down by 15% per year. Time to expiration is 2 years. Find the price of an American call on the stock with exercise [6 marks] price of $70. (c) An European call option is written on a stock whose current price is $150. The exercise price of the call is S120 and the expiration date is nine months from now. The volatility is 20% pa. It is assumed that the stock pay a continuous dividend with rate 1% pa. and the continuous interest rate is 4% p.a. By Greek letters, calculate the approximated change in [4 marks] the price of this call option due to $1 increase in stock price. Question 3 (a) In order to replicate the portfolio of a call option's payoff, a portfolio of stock and bond is considered. The price of a stock is currently $40 and it will either go up 15% or go down 10% after one year. The bond price is $100 with annual coupon rate 3%. A call option with exercise price of $40 will expire in one year. (i) Determine the investment strategy in the combination of stock and bond. (ii) Calculate the state price qy and the price of the call. [6 marks] [4 marks] (b) A3-date binomial model is considered for a stock with current price of $90, in which the annual interest rate is 3% and stock price either goes up by 25% or down by 15% per year. Time to expiration is 2 years. Find the price of an American call on the stock with exercise [6 marks] price of $70. (c) An European call option is written on a stock whose current price is $150. The exercise price of the call is S120 and the expiration date is nine months from now. The volatility is 20% pa. It is assumed that the stock pay a continuous dividend with rate 1% pa. and the continuous interest rate is 4% p.a. By Greek letters, calculate the approximated change in [4 marks] the price of this call option due to $1 increase in stock price