Answered step by step

Verified Expert Solution

Question

1 Approved Answer

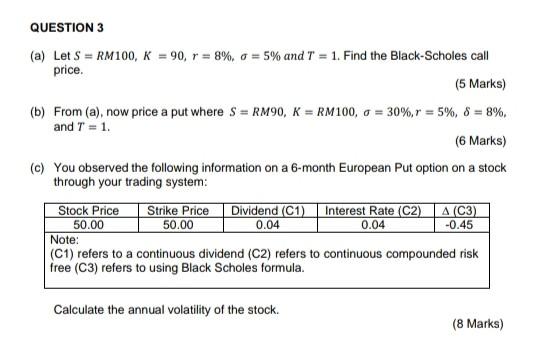

QUESTION 3 (a) Let S = RM100, K = 90, r = 8%, o = 5% and T = 1. Find the Black-Scholes call price.

QUESTION 3 (a) Let S = RM100, K = 90, r = 8%, o = 5% and T = 1. Find the Black-Scholes call price. (5 Marks) (b) From (a), now price a put where S = RM90, K = RM100, 0 = 30%,r = 5%, 8 = 8%. and T = 1. (6 Marks) (c) You observed the following information on a 6-month European Put option on a stock through your trading system: Stock Price Strike Price Dividend (C1) Interest Rate (C2) A (C3) 50.00 50.00 0.04 0.04 (C1) refers to a continuous dividend (C2) refers to continuous compounded risk free (C3) refers to using Black Scholes formula. -0.45 Note: Calculate the annual volatility of the stock. (8 Marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How To Start An Online Business In 7 Steps

Authors: Mr Tolga Cakir

1st Edition

0993303803, 978-0993303807