Answered step by step

Verified Expert Solution

Question

1 Approved Answer

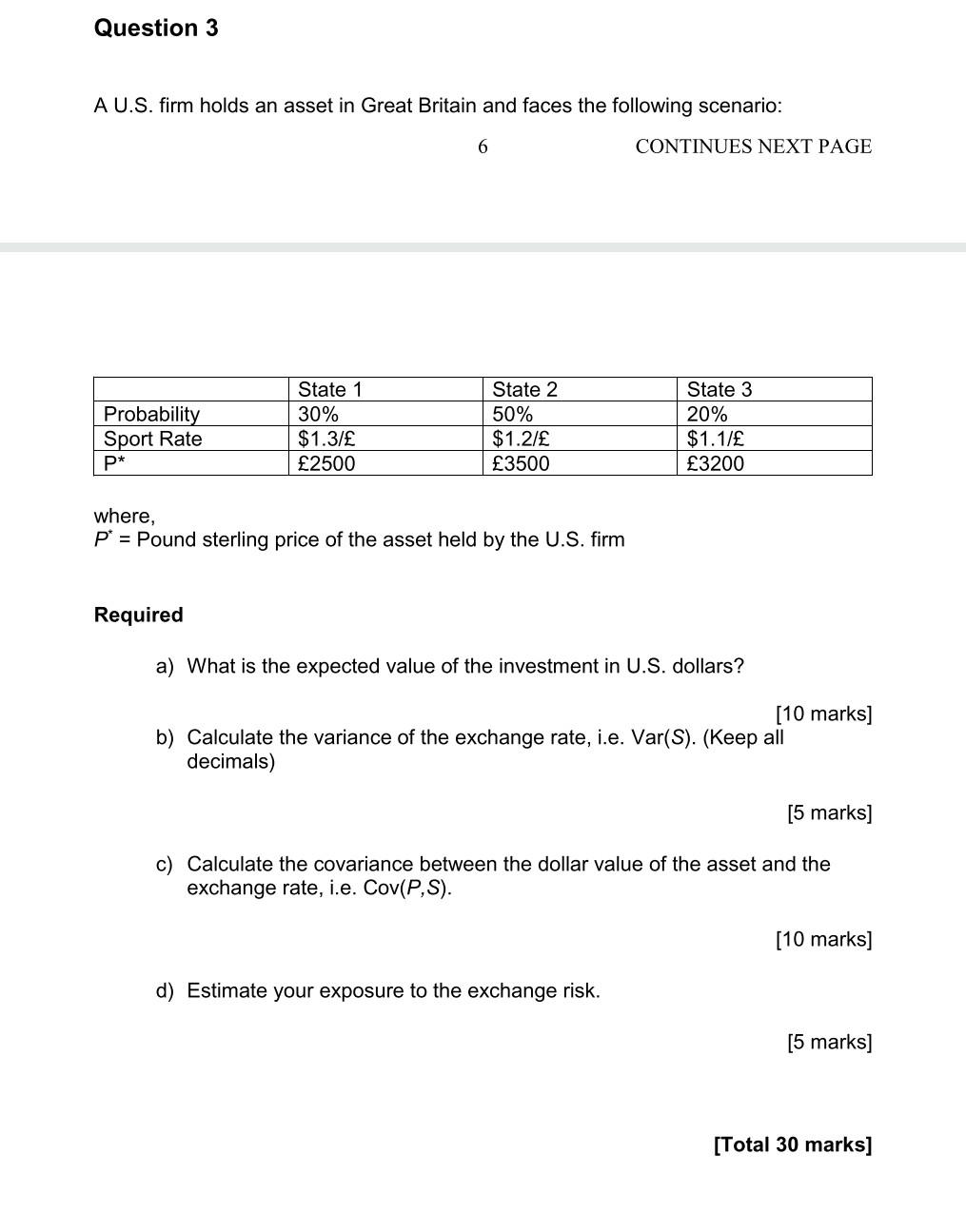

Question 3 A U.S. firm holds an asset in Great Britain and faces the following scenario: 6 Probability Sport Rate P* State 1 30% $1.3/

Question 3 A U.S. firm holds an asset in Great Britain and faces the following scenario: 6 Probability Sport Rate P* State 1 30% $1.3/ 2500 Required State 2 50% $1.2/ 3500 where, P* = Pound sterling price of the asset held by the U.S. firm CONTINUES NEXT PAGE State 3 20% $1.1/ 3200 a) What is the expected value of the investment in U.S. dollars? d) Estimate your exposure to the exchange risk. [10 marks] b) Calculate the variance of the exchange rate, i.e. Var(S). (Keep all decimals) [5 marks] c) Calculate the covariance between the dollar value of the asset and the exchange rate, i.e. Cov(P,S). [10 marks] [5 marks] [Total 30 marks]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Changing Geography Of Banking And Finance

Authors: Pietro Alessandrini ,Michele Fratianni ,Alberto Zazzaro

1st Edition

1441947205, 978-1441947208