Answered step by step

Verified Expert Solution

Question

1 Approved Answer

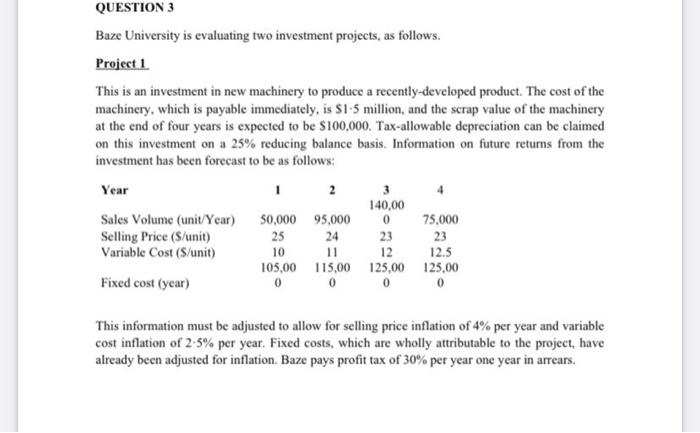

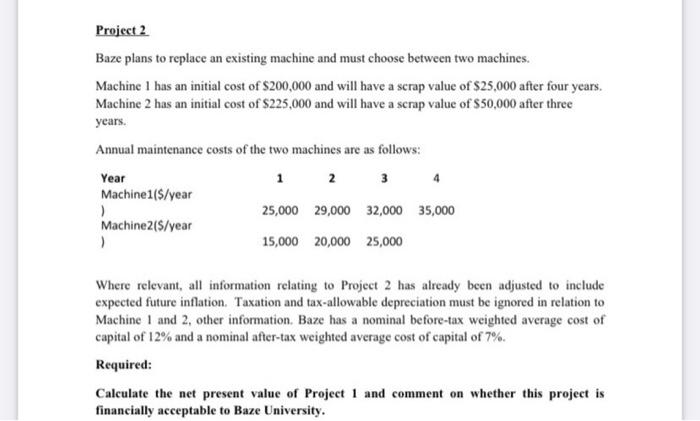

QUESTION 3 Baze University is evaluating two investment projects, as follows. Project 1 This is an investment in new machinery to produce a recently-developed product.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Economics Discussion Series Tax Exhaustion Firm Investment And Leasing A Test Of The Q Model Of Investment

Authors: United States Federal Reserve Board, Michael P. O'Malley

1st Edition

1288722370, 9781288722372