Question

Question 3 Bond X is a 4% coupon bond and Bond Y is an 8% coupon bond. Both bonds require ten years to maturity. Bond

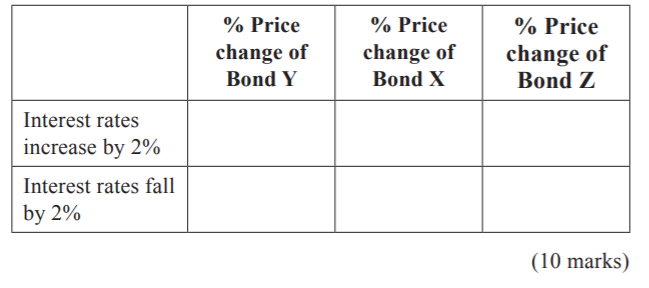

Question 3

Bond X is a 4% coupon bond and Bond Y is an 8% coupon bond. Both bonds require ten years to maturity. Bond Z, similar to Bond X, has the same 4% coupon payment. However, bond Z is a longer-dated bond, with 15 years to maturity. The three issues have a par value of $1,000 and make semi-annual payments. At the moment, the yield-to-maturity (YTM) of the three bonds is 6% p.a. Assume the market is efficient. Answer the following questions:

a) Find out the current price of the three bonds. (6 marks)

b) If interest rates were to suddenly rise by 2%, what would be the respective new price? What if the interest rate were to suddenlyfall by 2% instead? (9 marks)

c) From your answers in parts (a) and (b), what relationship have you observed about the interest rate risk of lower coupon bonds and longer-dated bonds? Complete the following table to assist your explanation.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Selected Works Of George J. Benston Banking And Financial Services Volume 1

Authors: James D. Rosenfeld

1st Edition

0195389018, 0199745471, 9780199745470