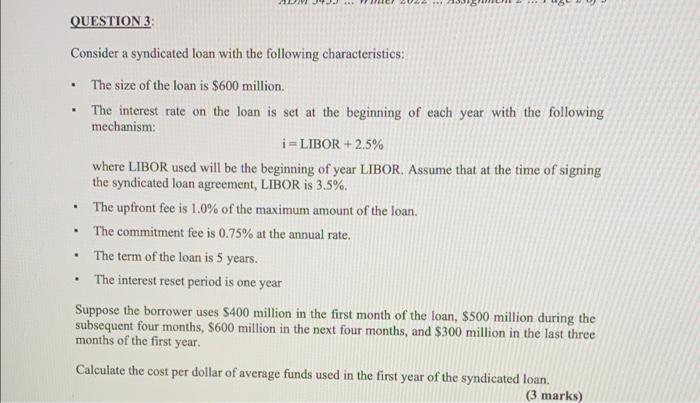

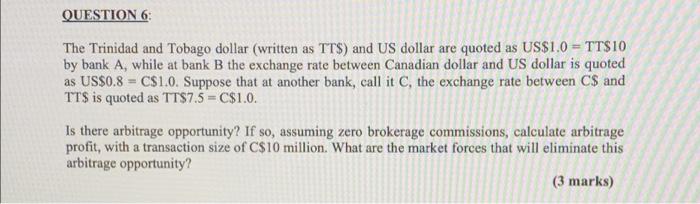

QUESTION 3 Consider a syndicated loan with the following characteristics: . The size of the loan is $600 million. The interest rate on the loan is set at the beginning of each year with the following mechanism: i = LIBOR +2.5% where LIBOR used will be the beginning of year LIBOR. Assume that at the time of signing the syndicated loan agreement, LIBOR is 3.5%. The upfront fee is 1.0% of the maximum amount of the loan. The commitment fee is 0.75% at the annual rate. The term of the loan is 5 years. The interest reset period is one year Suppose the borrower uses $400 million in the first month of the loan, $500 million during the subsequent four months, $600 million in the next four months, and $300 million in the last three months of the first year. Calculate the cost per dollar of average funds used in the first year of the syndicated loan. (3 marks) QUESTION 6 The Trinidad and Tobago dollar (written as TTS) and US dollar are quoted as US$1.0 = TT$10 by bank A, while at bank B the exchange rate between Canadian dollar and US dollar is quoted as US$0.8 = CS10. Suppose that at another bank, call it C, the exchange rate between C$ and TT$ is quoted as TTS7.5 = C$1.0. Is there arbitrage opportunity? If so, assuming zero brokerage commissions, calculate arbitrage profit, with a transaction size of C$10 million. What are the market forces that will eliminate this arbitrage opportunity? (3 marks) QUESTION 3 Consider a syndicated loan with the following characteristics: . The size of the loan is $600 million. The interest rate on the loan is set at the beginning of each year with the following mechanism: i = LIBOR +2.5% where LIBOR used will be the beginning of year LIBOR. Assume that at the time of signing the syndicated loan agreement, LIBOR is 3.5%. The upfront fee is 1.0% of the maximum amount of the loan. The commitment fee is 0.75% at the annual rate. The term of the loan is 5 years. The interest reset period is one year Suppose the borrower uses $400 million in the first month of the loan, $500 million during the subsequent four months, $600 million in the next four months, and $300 million in the last three months of the first year. Calculate the cost per dollar of average funds used in the first year of the syndicated loan. (3 marks) QUESTION 6 The Trinidad and Tobago dollar (written as TTS) and US dollar are quoted as US$1.0 = TT$10 by bank A, while at bank B the exchange rate between Canadian dollar and US dollar is quoted as US$0.8 = CS10. Suppose that at another bank, call it C, the exchange rate between C$ and TT$ is quoted as TTS7.5 = C$1.0. Is there arbitrage opportunity? If so, assuming zero brokerage commissions, calculate arbitrage profit, with a transaction size of C$10 million. What are the market forces that will eliminate this arbitrage opportunity