Answered step by step

Verified Expert Solution

Question

1 Approved Answer

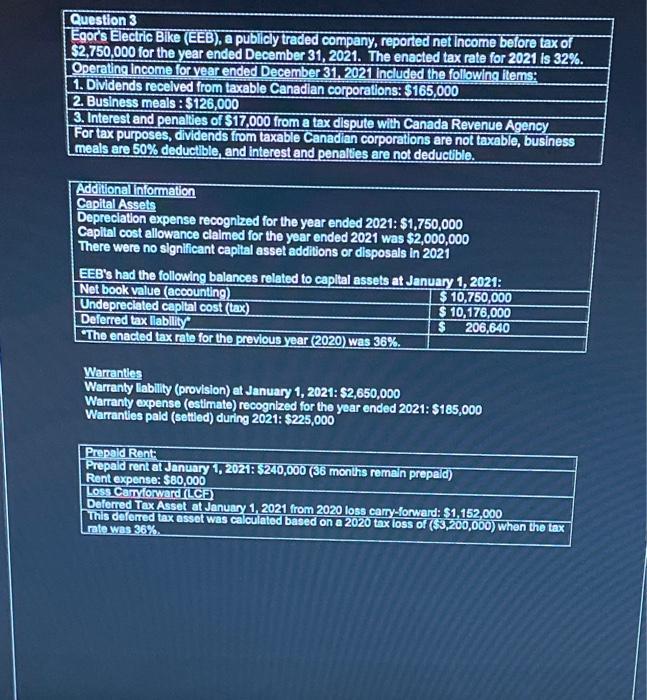

Question 3 Egor's Electric Bike (EEB), a publicly traded company, reported net income before tax of $2,750,000 for the year ended December 31, 2021.

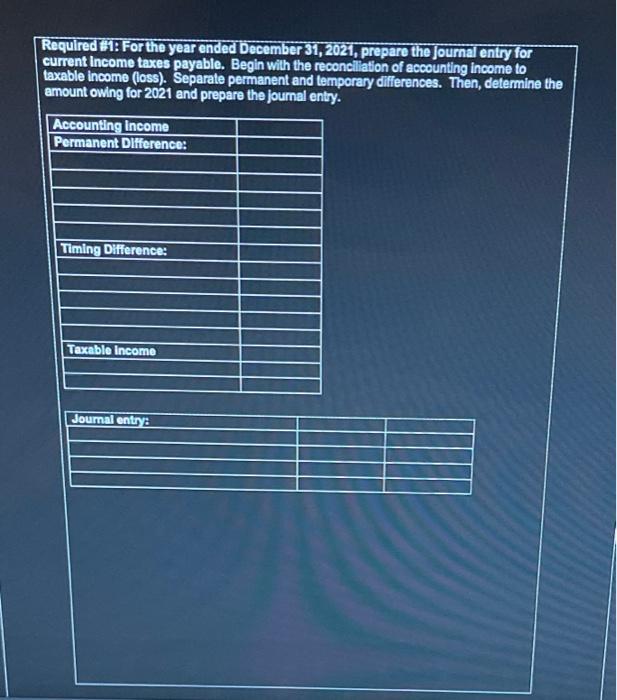

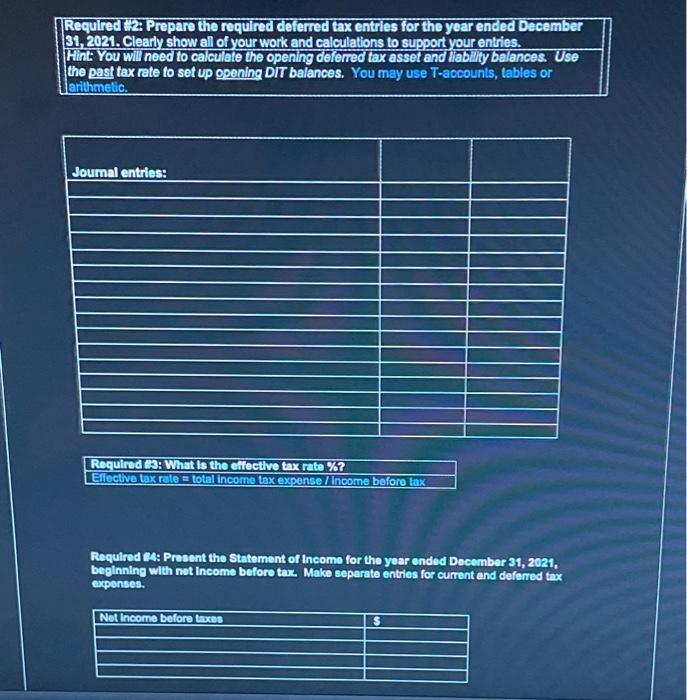

Question 3 Egor's Electric Bike (EEB), a publicly traded company, reported net income before tax of $2,750,000 for the year ended December 31, 2021. The enacted tax rate for 2021 is 32%. Operating income for year ended December 31, 2021 included the following items: 1. Dividends received from taxable Canadian corporations: $165,000 2. Business meals: $126,000 3. Interest and penalties of $17,000 from a tax dispute with Canada Revenue Agency For tax purposes, dividends from taxable Canadian corporations are not taxable, business meals are 50% deductible, and interest and penalties are not deductible. Additional Information Capital Assets Depreciation expense recognized for the year ended 2021: $1,750,000 Capital cost allowance claimed for the year ended 2021 was $2,000,000 There were no significant capital asset additions or disposals in 2021 EEB's had the following balances related to capital assets at January 1, 2021: Net book value (accounting) $ 10,750,000 $10,176,000 Undepreciated capital cost (tax) $ 206,640 Deferred tax liability The enacted tax rate for the previous year (2020) was 36%. Warranties Warranty liability (provision) at January 1, 2021: $2,650,000 Warranty expense (estimate) recognized for the year ended 2021: $185,000 Warranties paid (settled) during 2021: $225,000 Prepaid Rent: Prepaid rent at January 1, 2021: $240,000 (36 months remain prepaid) Rent expense: $80,000 Loss Carryforward (LCF) Deferred Tax Asset at January 1, 2021 from 2020 loss carry-forward: $1,152,000 This deferred tax asset was calculated based on a 2020 tax loss of ($3,200,000) when the tax rate was 36% Required #1: For the year ended December 31, 2021, prepare the journal entry for current income taxes payable. Begin with the reconciliation of accounting income to taxable income (loss). Separate permanent and temporary differences. Then, determine the amount owing for 2021 and prepare the journal entry. Accounting income Permanent Difference: Timing Difference: Taxable income Journal entry: Required #2: Prepare the required deferred tax entries for the year ended December 31, 2021. Clearly show all of your work and calculations to support your entries. Hint: You will need to calculate the opening deferred tax asset and liability balances. Use the past tax rate to set up opening DIT balances. You may use T-accounts, tables or arithmetic. Journal entries: Required #3: What is the effective tax rate %? Effective tax rate= total income tax expense / Income before tax Required #4: Present the Statement of Income for the year ended December 31, 2021, beginning with net Income before tax. Make separate entries for current and deferred tax expenses. Net Income before taxes

Step by Step Solution

★★★★★

3.51 Rating (158 Votes )

There are 3 Steps involved in it

Step: 1

Income before tax Accounting income Permanent difference Timing difference Total in...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: J. David Spiceland, James Sepe, Mark Nelson

6th edition

978-0077328894, 71313974, 9780077395810, 77328892, 9780071313971, 77395816, 978-0077400163