Answered step by step

Verified Expert Solution

Question

1 Approved Answer

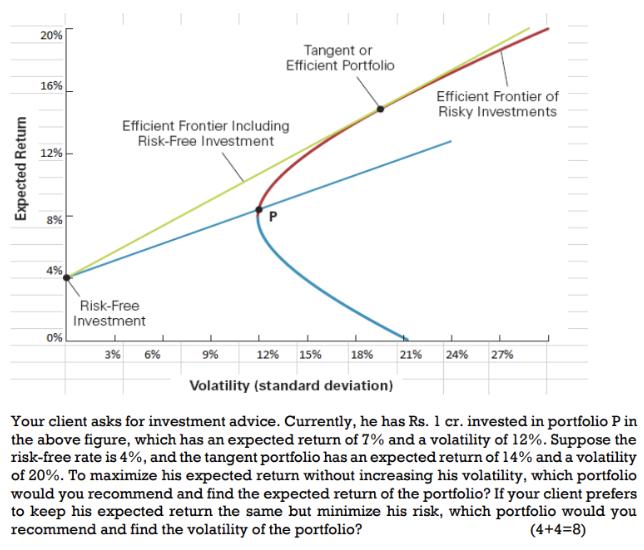

Expected Return 20% 16% 12% 8% 0% Efficient Frontier Including Risk-Free Investment Risk-Free Investment 3% 6% 9% Tangent or Efficient Portfolio P 12% 15%

Expected Return 20% 16% 12% 8% 0% Efficient Frontier Including Risk-Free Investment Risk-Free Investment 3% 6% 9% Tangent or Efficient Portfolio P 12% 15% 18% 21% Volatility (standard deviation) Efficient Frontier of Risky Investments 24% 27% Your client asks for investment advice. Currently, he has Rs. 1 cr. invested in portfolio P in the above figure, which has an expected return of 7% and a volatility of 12%. Suppose the risk-free rate is 4%, and the tangent portfolio has an expected return of 14% and a volatility of 20%. To maximize his expected return without increasing his volatility, which portfolio would you recommend and find the expected return of the portfolio? If your client prefers to keep his expected return the same but minimize his risk, which portfolio would you recommend and find the volatility of the portfolio? (4+4=8)

Step by Step Solution

★★★★★

3.45 Rating (165 Votes )

There are 3 Steps involved in it

Step: 1

Step 11 SOLUTION Calculation of portfolio to maximize expected return at current volatility Maintain...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: Donald E. Kieso, Jerry J. Weygandt, And Terry D. Warfield

13th Edition

9780470374948, 470423684, 470374942, 978-0470423684