Answered step by step

Verified Expert Solution

Question

1 Approved Answer

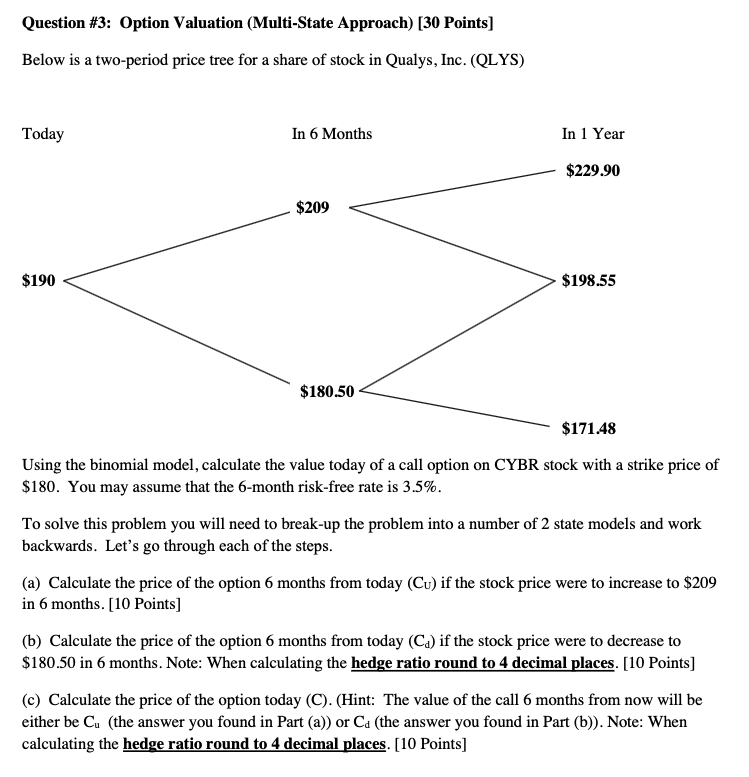

Question # 3 : Option Valuation ( Multi - State Approach ) [ 3 0 Points ] Below is a two - period price tree

Question #: Option Valuation MultiState Approach Points

Below is a twoperiod price tree for a share of stock in Qualys, Inc. QLYS

$

Using the binomial model, calculate the value today of a call option on CYBR stock with a strike price of $ You may assume that the month riskfree rate is

To solve this problem you will need to breakup the problem into a number of state models and work backwards. Let's go through each of the steps.

a Calculate the price of the option months from today if the stock price were to increase to $ in months. Points

b Calculate the price of the option months from today if the stock price were to decrease to $ in months. Note: When calculating the hedge ratio round to decimal places. Points

c Calculate the price of the option today CHint: The value of the call months from now will be either be the answer you found in Part a or the answer you found in Part b Note: When calculating the hedge ratio round to decimal places. Points

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Jeff Madura

3rd Edition

0321357973, 978-0321357977