Answered step by step

Verified Expert Solution

Question

1 Approved Answer

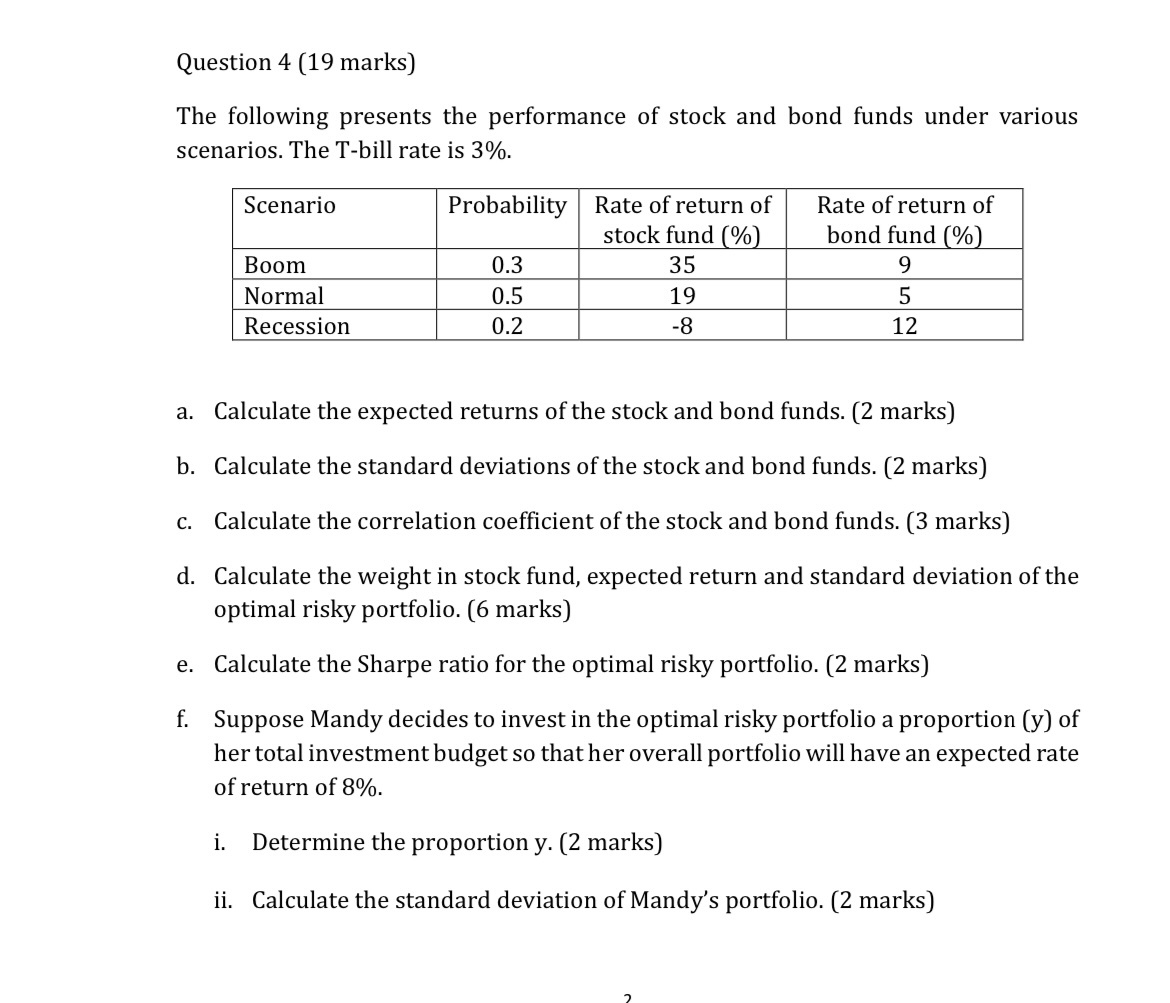

Question 4 ( 1 9 marks ) The following presents the performance of stock and bond funds under various scenarios. The T - bill rate

Question marks

The following presents the performance of stock and bond funds under various

scenarios. The Tbill rate is

a Calculate the expected returns of the stock and bond funds. marks

b Calculate the standard deviations of the stock and bond funds. marks

c Calculate the correlation coefficient of the stock and bond funds. marks

d Calculate the weight in stock fund, expected return and standard deviation of the

optimal risky portfolio. marks

e Calculate the Sharpe ratio for the optimal risky portfolio. marks

f Suppose Mandy decides to invest in the optimal risky portfolio a proportion y of

her total investment budget so that her overall portfolio will have an expected rate

of return of

i Determine the proportion y marks

ii Calculate the standard deviation of Mandy's portfolio. marks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Short Term Financial Management

Authors: John Zietlow, Matthew Hill, Terry Maness

5th Edition

1516512405, 9781516512409