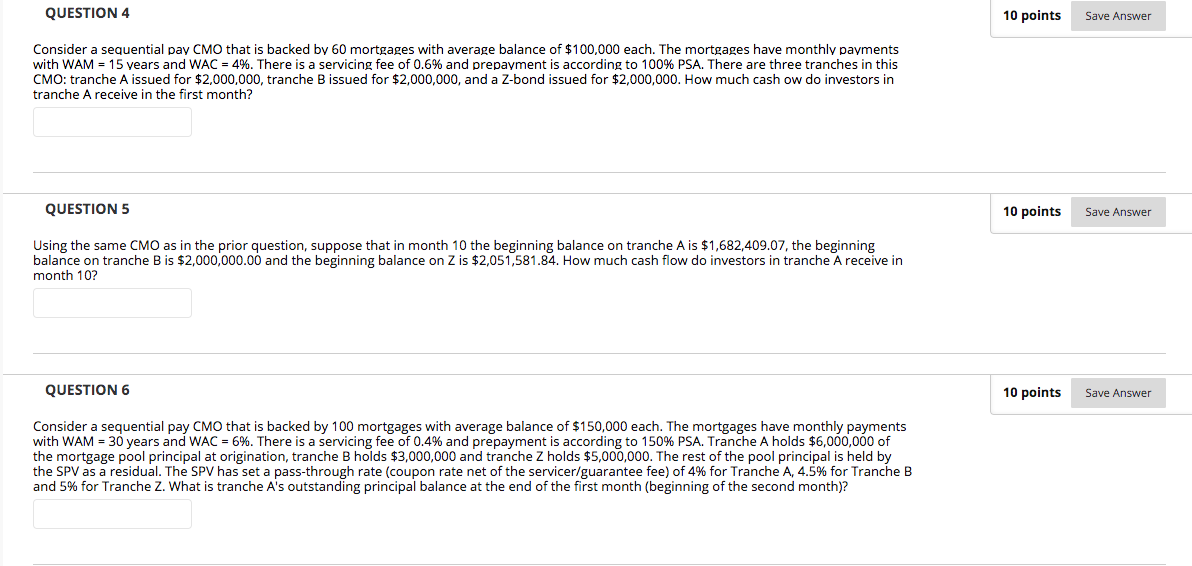

QUESTION 4 10 points Save Answer Consider a sequential pay CMO that is backed by 60 mortgages with average balance of $100,000 each. The mortgages have monthly payments with WAM = 15 years and WAC = 4%. There is a servicing fee of 0.6% and prepayment is according to 100% PSA. There are three tranches in this CMO: tranche A issued for $2,000,000, tranche B issued for $2,000,000, and a Z-bond issued for $2,000,000. How much cash ow do investors in tranche A receive in the first month? QUESTION 5 10 points Save Answer Using the same CMO as in the prior question, suppose that in month 10 the beginning balance on tranche A is $1,682,409.07, the beginning balance on tranche B is $2,000,000.00 and the beginning balance on Z is $2,051,581.84. How much cash flow do investors in tranche A receive in month 10? QUESTION 6 10 points Save Answer Consider a sequential pay CMO that is backed by 100 mortgages with average balance of $150,000 each. The mortgages have monthly payments with WAM = 30 years and WAC = 6%. There is a servicing fee of 0.4% and prepayment is according to 150% PSA. Tranche A holds $6,000,000 of the mortgage pool principal at origination, tranche B holds $3,000,000 and tranche Z holds $5,000,000. The rest of the pool principal is held by the SPV as a residual. The SPV has set a pass-through rate (coupon rate net of the servicer/guarantee fee) of 4% for Tranche A, 4.5% for Tranche B and 5% for Tranche Z. What is tranche A's outstanding principal balance at the end of the first month (beginning of the second month)? QUESTION 4 10 points Save Answer Consider a sequential pay CMO that is backed by 60 mortgages with average balance of $100,000 each. The mortgages have monthly payments with WAM = 15 years and WAC = 4%. There is a servicing fee of 0.6% and prepayment is according to 100% PSA. There are three tranches in this CMO: tranche A issued for $2,000,000, tranche B issued for $2,000,000, and a Z-bond issued for $2,000,000. How much cash ow do investors in tranche A receive in the first month? QUESTION 5 10 points Save Answer Using the same CMO as in the prior question, suppose that in month 10 the beginning balance on tranche A is $1,682,409.07, the beginning balance on tranche B is $2,000,000.00 and the beginning balance on Z is $2,051,581.84. How much cash flow do investors in tranche A receive in month 10? QUESTION 6 10 points Save Answer Consider a sequential pay CMO that is backed by 100 mortgages with average balance of $150,000 each. The mortgages have monthly payments with WAM = 30 years and WAC = 6%. There is a servicing fee of 0.4% and prepayment is according to 150% PSA. Tranche A holds $6,000,000 of the mortgage pool principal at origination, tranche B holds $3,000,000 and tranche Z holds $5,000,000. The rest of the pool principal is held by the SPV as a residual. The SPV has set a pass-through rate (coupon rate net of the servicer/guarantee fee) of 4% for Tranche A, 4.5% for Tranche B and 5% for Tranche Z. What is tranche A's outstanding principal balance at the end of the first month (beginning of the second month)