Answered step by step

Verified Expert Solution

Question

1 Approved Answer

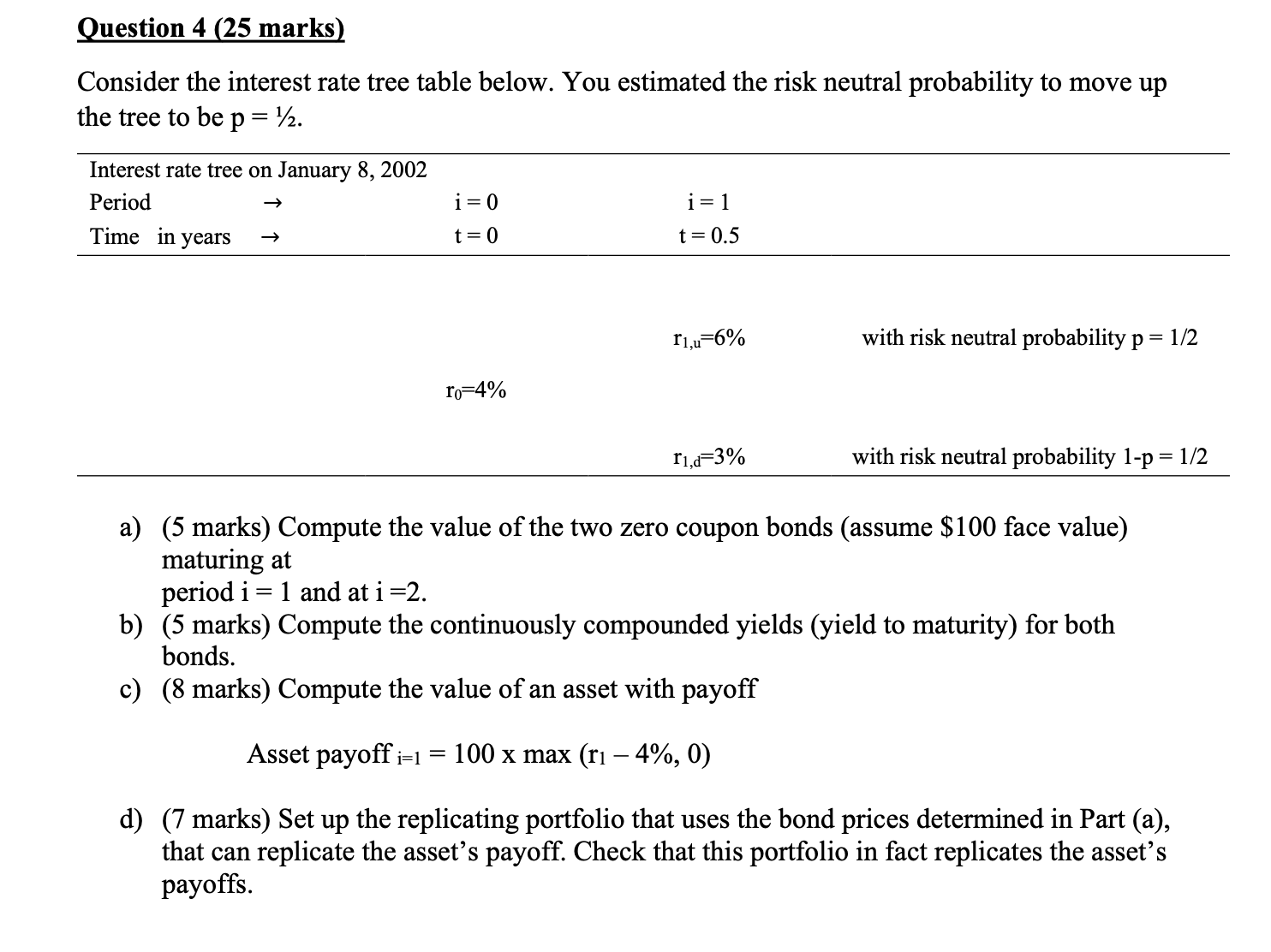

Question 4 ( 2 5 marks ) Consider the interest rate tree table below. You estimated the risk neutral probability to move up the tree

Question marks

Consider the interest rate tree table below. You estimated the risk neutral probability to move up

the tree to be

a marks Compute the value of the two zero coupon bonds assume $ face value

maturing at

period and at

b marks Compute the continuously compounded yields yield to maturity for both

bonds.

c marks Compute the value of an asset with payoff

Asset payoff max

d marks Set up the replicating portfolio that uses the bond prices determined in Part a

that can replicate the asset's payoff. Check that this portfolio in fact replicates the asset's

payoffs. Consider the interest rate tree table below. You estimated the risk neutral probability to move up

the tree to be p

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cases In Financial Reporting

Authors: Ellen Engel, D. Eric Hirst, Mary Lea McAnally

7th Edition

1934319791, 9781934319796