Answered step by step

Verified Expert Solution

Question

1 Approved Answer

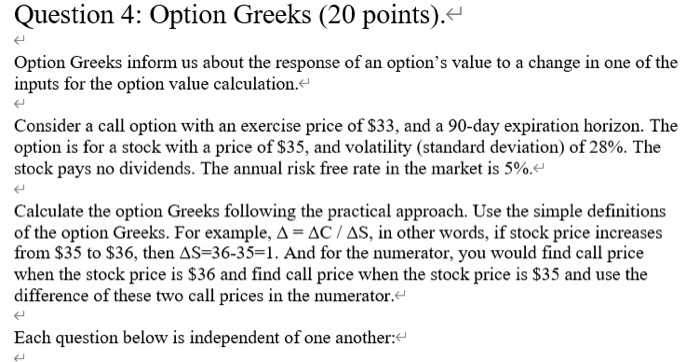

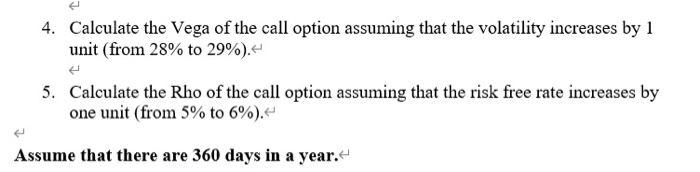

Question 4: Option Greeks (20 points). Option Greeks inform us about the response of an option's value to a change in one of the inputs

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Relief For Single Parents A Proven Plan For Achieving The Seemingly Impossible

Authors: Brenda Armstrong , Dave Ramsey

1st Edition

0802444091,1575674270