Answered step by step

Verified Expert Solution

Question

1 Approved Answer

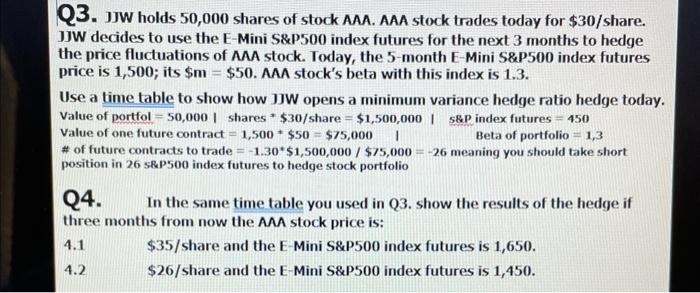

question 4 pleaze Q3. JJW holds 50,000 shares of stock AAA. AAA stock trades today for $30/ share. JJW decides to use the E-Mini S&P500

question 4 pleaze

Q3. JJW holds 50,000 shares of stock AAA. AAA stock trades today for $30/ share. JJW decides to use the E-Mini S\&P500 index futures for the next 3 months to hedge the price fluctuations of AAA stock. Today, the 5-month E-Mini S\&P500 index futures price is 1,500 ; its $m=$50. AAA stock's beta with this index is 1.3. Use a time table to show how JJW opens a minimum variance hedge ratio hedge today. Value of portfol =50,0001 shares $30/ share =$1,500,000 I 5&P index futures =450 Value of one future contract =1,500$50=$75,000 I Beta of portfolio =1,3 # of future contracts to trade =1.30$1,500,000/$75,000=26 meaning you should take short position in 26 skp500 index futures to hedge stock portfolio Q4. In the same time table you used in Q3. show the results of the hedge if three months from now the AAA stock price is: 4.1 $35/ share and the E-Mini S\&P500 index futures is 1,650. 4.2 $26 /share and the E-Mini S\&P500 index futures is 1,450 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Stochastic Filtering With Applications In Finance

Authors: Bhar Ramaprasad

1st Edition

9814304859, 9789814304856