Question 4: Substantive Procedures and Audit Documentation

After the end of the financial year, Jane Owen performed transaction tests of the inventory purchases and cash disbursement. She summarised the audit procedures she performed in the following workpaper (reference N-2). To ensure audit quality, BDC has a review policy which helps to ensure that each audit document provides a clear and complete indication of the procedures that were performed and that adequate evidence has been collected. For this audit, you must review and approve all audit workpapers. If you find any unclarity or issues in a workpaper, the workpaper is returned to the appropriate staff auditor for necessary and appropriate revision.

REQUIRED:

Review the audit work papers below. Prepare Jane a list of the concerns that are present in her work papers. For each point raised, give explanations why the documentation is not appropriate.

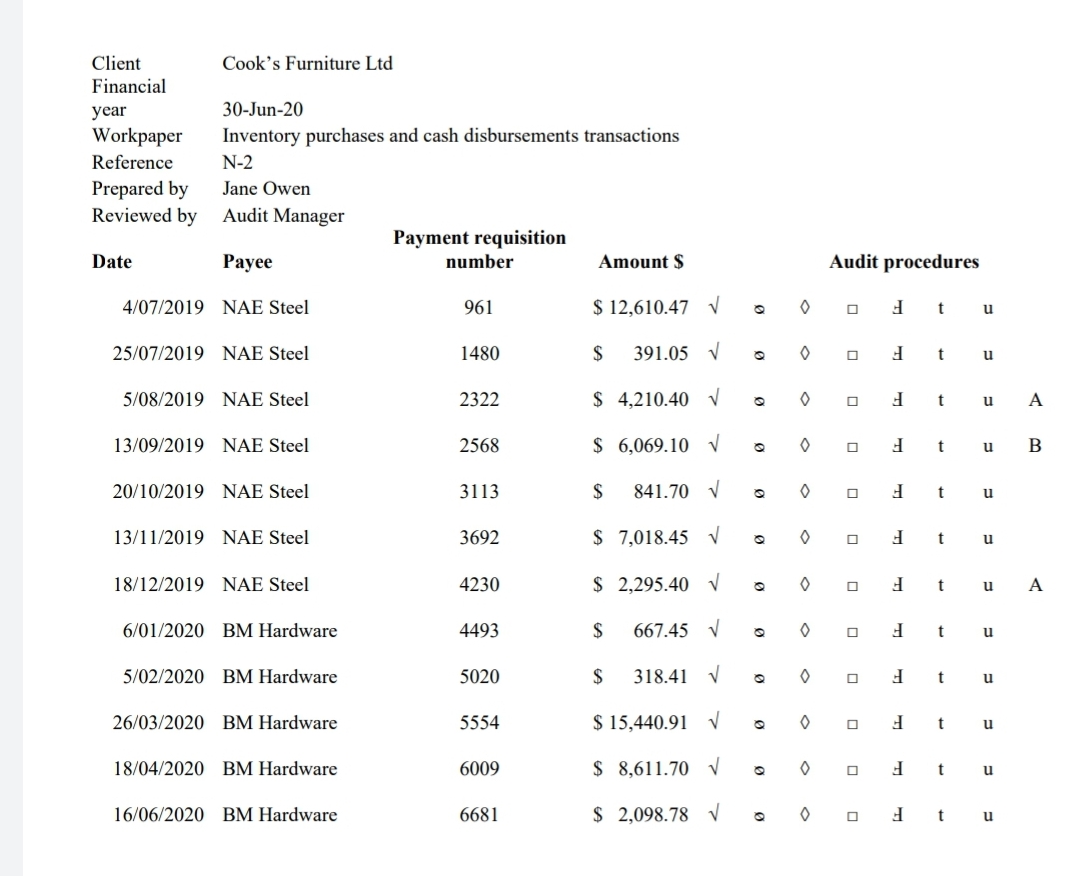

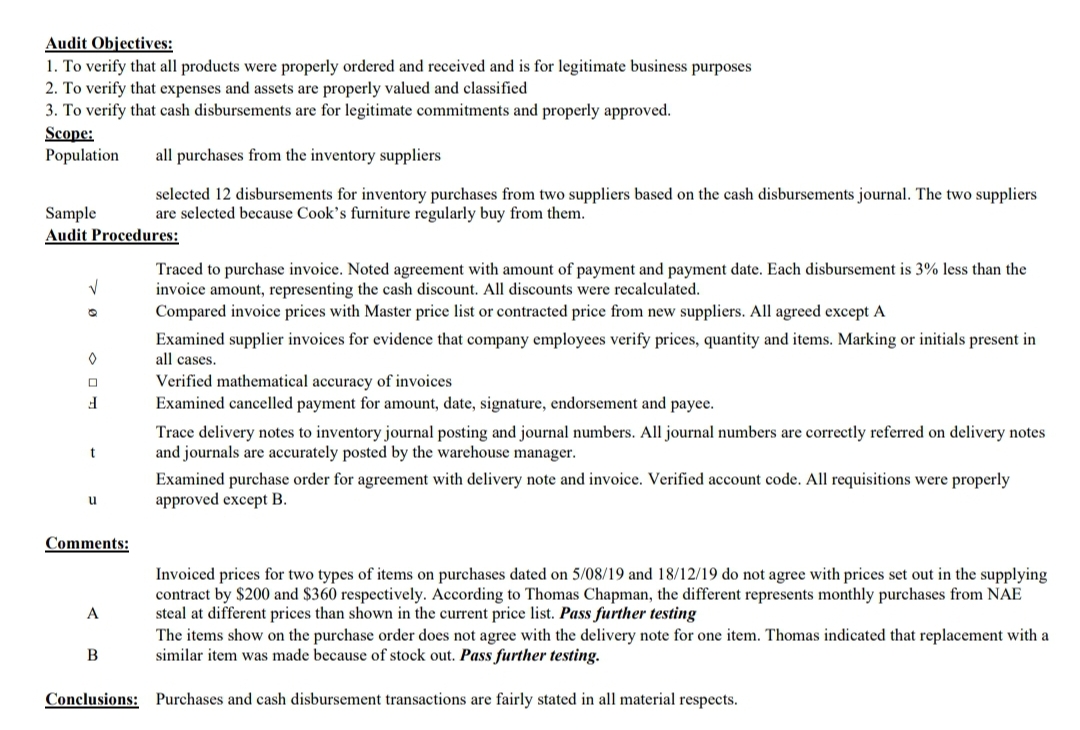

Client Cook's Furniture Ltd Financial year 30-Jun-20 Workpaper Inventory purchases and cash disbursements transactions Reference N-2 Prepared by Jane Owen Reviewed by Audit Manager Payment requisition Date Payee number Amount $ Audit procedures 4/07/2019 NAE Steel 961 $ 12,610.47 V O t 25/07/2019 NAE Steel 1480 $ 391.05 V O C U 5/08/2019 NAE Steel 2322 $ 4,210.40 V O F t u A 13/09/2019 NAE Steel 2568 $ 6,069.10 V O L B 20/10/2019 NAE Steel 3113 $ 841.70 V t U 13/11/2019 NAE Steel 3692 $ 7,018.45 V O U 18/12/2019 NAE Steel 4230 $ 2,295.40 V 0 t 11 A 6/01/2020 BM Hardware 4493 $ 667.45 V 0 T 5/02/2020 BM Hardware 5020 $ 318.41 V 0 t 26/03/2020 BM Hardware 5554 $ 15,440.91 V 0 T 18/04/2020 BM Hardware 6009 $ 8,611.70 O t 16/06/2020 BM Hardware 6681 $ 2,098.78 V O t UAudit Objectives: 1. To verify that all products were properly ordered and received and is for legitimate business purposes 2. To verify that expenses and assets are properly valued and classified 3. To verify that cash disbursements are for legitimate commitments and properly approved. Scope: Population all purchases from the inventory suppliers Sample selected 12 disbursements for inventory purchases from two suppliers based on the cash disbursements journal. The two suppliers are selected because Cook's furniture regularly buy from them. Audit Procedures: Traced to purchase invoice. Noted agreement with amount of payment and payment date. Each disbursement is 3% less than the invoice amount, representing the cash discount. All discounts were recalculated. Compared invoice prices with Master price list or contracted price from new suppliers. All agreed except A Examined supplier invoices for evidence that company employees verify prices, quantity and items. Marking or initials present in all cases. Verified mathematical accuracy of invoices Examined cancelled payment for amount, date, signature, endorsement and payee. Trace delivery notes to inventory journal posting and journal numbers. All journal numbers are correctly referred on delivery notes and journals are accurately posted by the warehouse manager. Examined purchase order for agreement with delivery note and invoice. Verified account code. All requisitions were properly u approved except B. Comments: Invoiced prices for two types of items on purchases dated on 5/08/19 and 18/12/19 do not agree with prices set out in the supplying contract by $200 and $360 respectively. According to Thomas Chapman, the different represents monthly purchases from NAE A steal at different prices than shown in the current price list. Pass further testing The items show on the purchase order does not agree with the delivery note for one item. Thomas indicated that replacement with a B similar item was made because of stock out. Pass further testing. Conclusions: Purchases and cash disbursement transactions are fairly stated in all material respects