Answered step by step

Verified Expert Solution

Question

1 Approved Answer

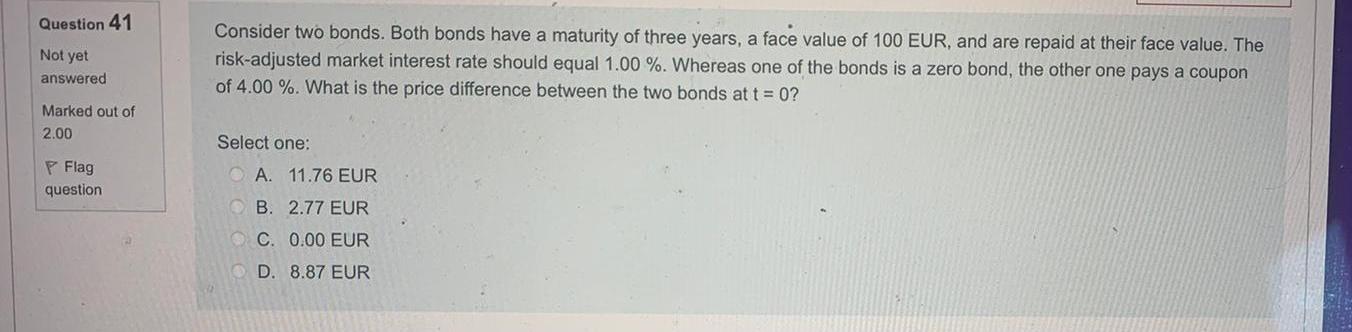

Question 41 Not yet Consider two bonds. Both bonds have a maturity of three years, a face value of 100 EUR, and are repaid at

Question 41 Not yet Consider two bonds. Both bonds have a maturity of three years, a face value of 100 EUR, and are repaid at their face value. The risk-adjusted market interest rate should equal 1.00 %. Whereas one of the bonds is a zero bond, the other one pays a coupon of 4.00 %. What is the price difference between the two bonds at t = 0? answered Marked out of 2.00 Select one: P Flag question A. 11.76 EUR B. 2.77 EUR C. 0.00 EUR D. 8.87 EUR

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Charles E. Davis, Elizabeth Davis

2nd edition

ISBN: 1118548639, 9781118800713, 1118338448, 9781118548639, 1118800710, 978-1118338445