Answered step by step

Verified Expert Solution

Question

1 Approved Answer

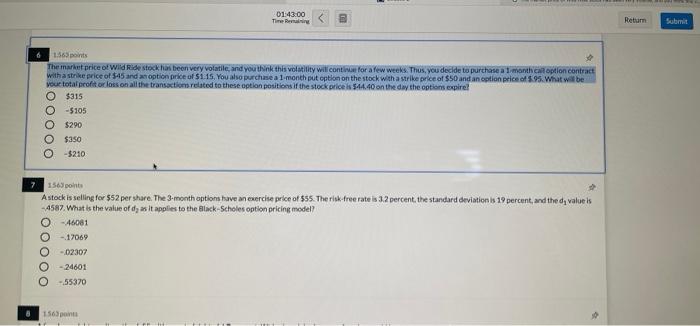

question 6 01:43:00 Time Return Submit 6 1.563 points The market price of Wild Ride stock has been very volatile, and you think this volatility

question 6

01:43:00 Time Return Submit 6 1.563 points The market price of Wild Ride stock has been very volatile, and you think this volatility will contine for a few weeks. Thus, you decide to purchase a month an option contract with a strike price of $45 and an option price of $115. You also purchase a 1-month put option on the stock with a strike price of $50 and an option price of $95. What will be You total profit or lots on all the transaction related to these option positions if the stock prices $14.40 on the day the options expire! $315 -5105 $290 $350 -$210 7 1565 points Astock is selling for $52 per share. The 3-month options save an exercise price of $55. The risk free rate is 3.2 percent. the standard deviation is 19 percent, and the dy value is -4587. What is the value of d, as it applies to the Black-Scholes option pricing model? -46061 -17069 -02307 -24601 -55370 1563 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Principals Guide To School Budgeting

Authors: Richard D. Sorenson, Lloyd M. Goldsmith

3rd Edition

1506389457, 978-1506389455